AI in Insurance Market Summary

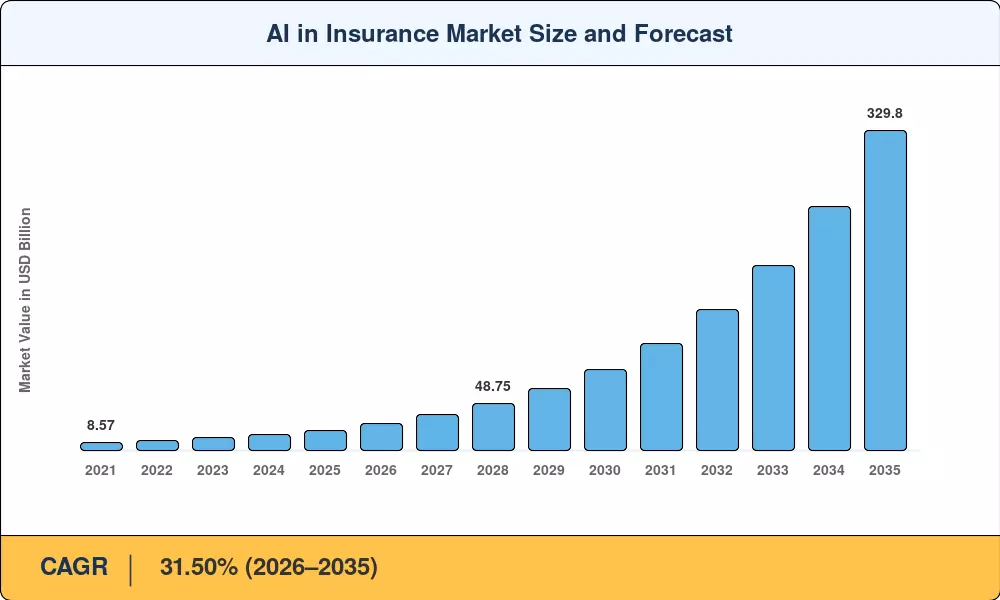

The AI in Insurance Market reached an estimated USD 20.90 billion in 2025 and is projected to expand from USD 28.05 Billion in 2026 to USD 329.80 billion by 2035, registering a CAGR of 31.50% across the forecast period. This aggressive trajectory reflects a structural shift rather than incremental adoption — insurers globally face regulatory mandates for faster claims adjudication and transparent pricing, and AI delivers both. The European Insurance and Occupational Pensions Authority's 2024 guidelines on algorithmic transparency, combined with state-level rate-filing automation requirements in the U.S., have created compliance-driven demand that accelerates capital allocation toward intelligent processing platforms [1].

Technology transformation sits at the center of this expansion. Legacy rule-based underwriting engines and manual claims workflows — systems that have anchored carrier operations for decades — are giving way to cloud-native AI stacks capable of real-time risk scoring and instant settlement decisions. Carriers invested an estimated USD 6.8 billion in AI infrastructure upgrades during 2024 alone, according to industry estimates from Celent [2]. Generative AI models now parse unstructured medical records and property inspection reports in seconds, compressing underwriting cycles that once took weeks into hours.

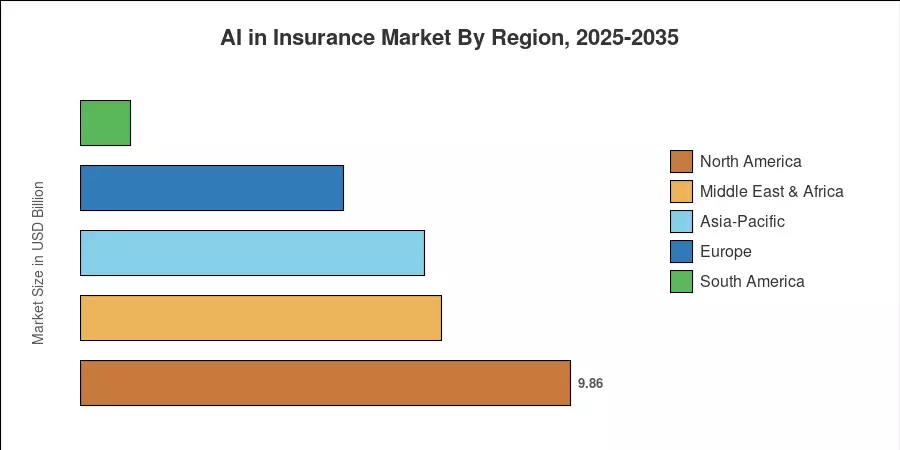

North America commands roughly 47.2% of the AI in Insurance Market, anchored by the density of insurtech investment in the U.S. and Canada. Asia-Pacific stands as the fastest-growing region at a projected 33.10% CAGR, propelled by digital-first insurance ecosystems in China and India. Europe holds the second-largest share at approximately 25.3%, driven by Solvency II modernization and open-insurance API frameworks. As embedded distribution models and parametric products gain traction, the AI in Insurance Market is poised to reshape how risk is priced, transferred, and settled through 2035.

Key Report Takeaways

• By Offering

- Software solutions accounted for 52.0% of the AI in the Insurance Market in 2025, reflecting carrier preference for modular platforms over custom-built tooling.

- Services are projected to grow at a 38.50% CAGR through 2035 as implementation and managed-AI support demand intensifies.

• By Technology

- Software solutions accounted for 52.0% of the AI in Insurance Market in 2025, reflecting carrier preference for modular platforms over custom-built tooling.

- Services are projected to grow at a 38.50% CAGR through 2035 as implementation and managed-AI support demand intensifies.

- Machine learning technology held 65.4% of revenue in 2025, underpinning claims triage, pricing, and fraud detection workloads.

• By End-User

- Property and casualty lines represented 62.4% of revenue, driven by computer-vision-enabled property assessment and telematics-based auto coverage.

• By Deployment

- Cloud-based deployments captured 65.6% of the AI in Insurance Market share in 2025, accelerated by API-first architectures.

- Property and casualty lines represented 62.4% of revenue, driven by computer-vision-enabled property assessment and telematics-based auto coverage.

• By Enterprise Size

- Small and medium insurers are expanding AI adoption at a 42.0% CAGR, the fastest pace across enterprise segments.

• By Region

- North America led the AI in Insurance Market with 47.2% share in 2025.

- Asia-Pacific is forecast to register a 33.10% CAGR, fueled by digital insurance mandates in China and India's regulatory sandbox programs.

AI in Insurance Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from audited carrier technology budgets, disclosed AI vendor revenue, and triangulated channel-partner intelligence. Forecast projections apply a bottom-up segment build calibrated against macroeconomic indicators, regulatory timelines, and disclosed investment pipelines. All figures are expressed in USD Billion at constant 2025 exchange rates.