Aircraft Electrical Systems Market Summary

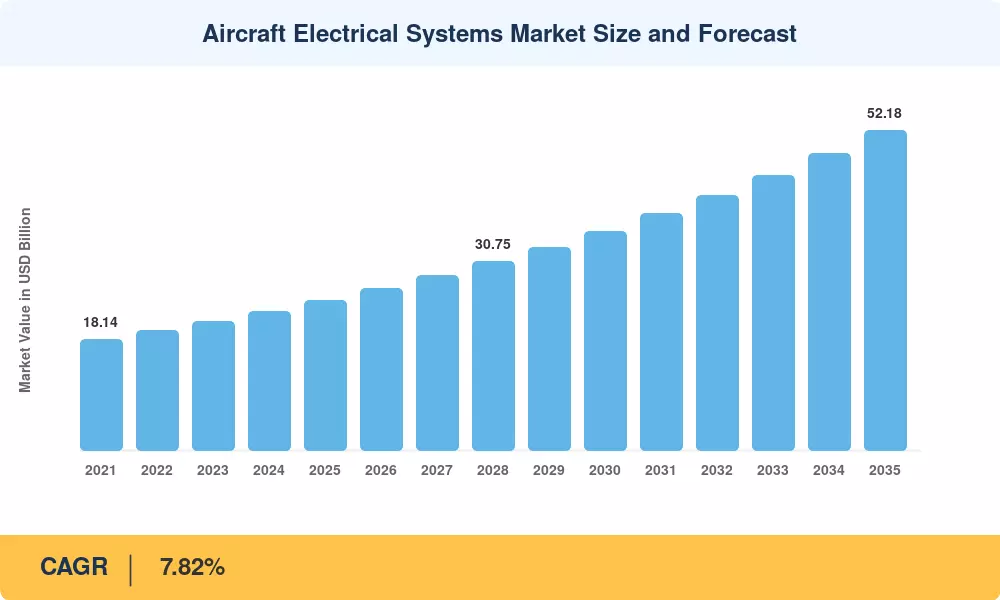

The Aircraft Electrical Systems Market stood at USD 24.52 billion in 2025 and is projected to reach USD 27.68 billion by 2026 before climbing to USD 52.18 billion by 2035, registering a CAGR of 7.82% during the 2026–2035 forecast window. Two catalysts anchor this trajectory: commercial OEM backlogs exceeding 14,000 aircraft at Airbus and Boeing, and the accelerating shift toward more electric aircraft MEA architectures that swap legacy pneumatic and hydraulic subsystems for lighter, electrically driven alternatives[2]. Government-backed clean-aviation mandates — including the EU's Clean Aviation Joint Undertaking and NASA's Electrified Powertrain Flight Demonstration — are channeling billions into aircraft power distribution systems and high-voltage conversion hardware.

A fundamental technology transformation is reshaping how aircraft generate, route, and consume electrical power. Legacy 115 V AC bus architectures are giving way to 270 V-plus DC distribution networks, cutting copper harness weight by roughly 35–40% and enabling silicon-carbide (SiC) semiconductor-based converters rated above 200 °C junction temperatures [3]. Aircraft electrical load management complexity has increased in parallel: next-generation widebodies now support cabin power budgets exceeding 1 MW, driving demand for intelligent load-shedding controllers and solid-state power-distribution units. Hybrid-electric propulsion demonstrators — such as Airbus's E-Fan X successor programs — validate high-power starter-generators and advanced avionics wiring harness architectures capable of handling megawatt-class loads safely.

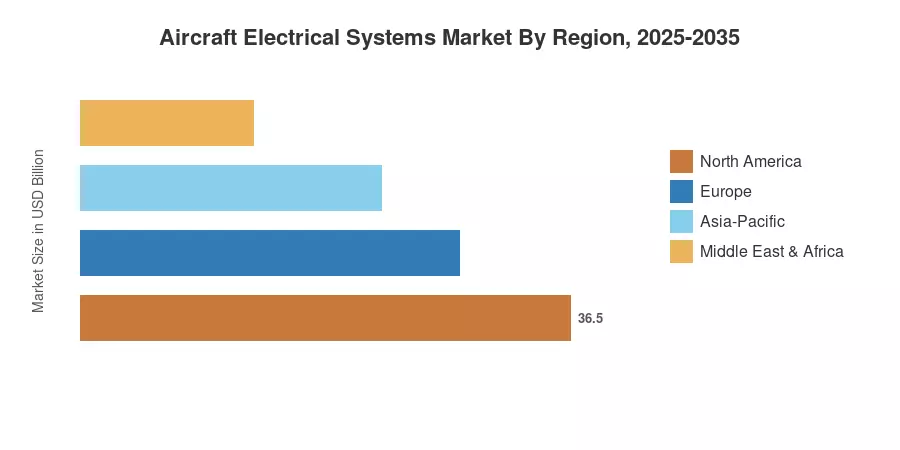

North America commands a 44.76% revenue share in the Aircraft Electrical Systems Market, anchored by U.S. defense electrification programs and Boeing's commercial production ramp Asia-Pacific is the fastest-growing region at an 8.53% CAGR, propelled by COMAC's C919 production scale-up and India's expanding MRO infrastructure. Europe holds the second-largest share at approximately 27%, driven by Airbus linefit demand and Safran's converter and generator programs. These regional dynamics position the Aircraft Electrical Systems Market for sustained double-digit growth pockets through the mid-2030s.

Key Report Takeaways

• By System

- Power distribution led with a 36.48% revenue share in 2025, reflecting growing adoption of solid-state aircraft power distribution systems across narrowbody platforms

- Energy storage is forecasted to post a 10.15% CAGR through 2035, driven by lithium-ion and next-generation battery demand for more electric aircraft MEA designs

• By Component

- Generators and starter-generators held a USD 5.46 billion share in 2025 as aircraft AC DC power systems transitioned to high-power integrated drive generators

- Battery packs and battery management systems are projected to expand at an 8.87% CAGR through 2035, fueled by eVTOL prototyping and cabin backup-power requirements

• By Platform

- Commercial aviation accounted for 67.71% of the Aircraft Electrical Systems Market in 2025

- General aviation is expected to grow at a 9.78% CAGR through 2035, supported by Part 23 aircraft electrification and personal air-mobility vehicle certification

• By Region

- North America commanded a 44.76% share in 2025

- Asia-Pacific is projected to register the fastest CAGR of 8.53% from 2026 to 2035

Market Size and Forecast (2021–2035)

MRFR's market-sizing methodology combines bottom-up revenue modeling from OEM and tier-1 supplier filings with top-down cross-validation against IATA fleet delivery forecasts, MRO spend databases, and trade-association production data. Historical figures (2021–2024) are derived from audited financial disclosures; the base-year 2025 estimate blends preliminary shipment data with channel-check interviews. Forecast values (2026–2035) apply segment-level CAGR assumptions stress-tested against fleet growth scenarios.

.webp?v=1782888034)