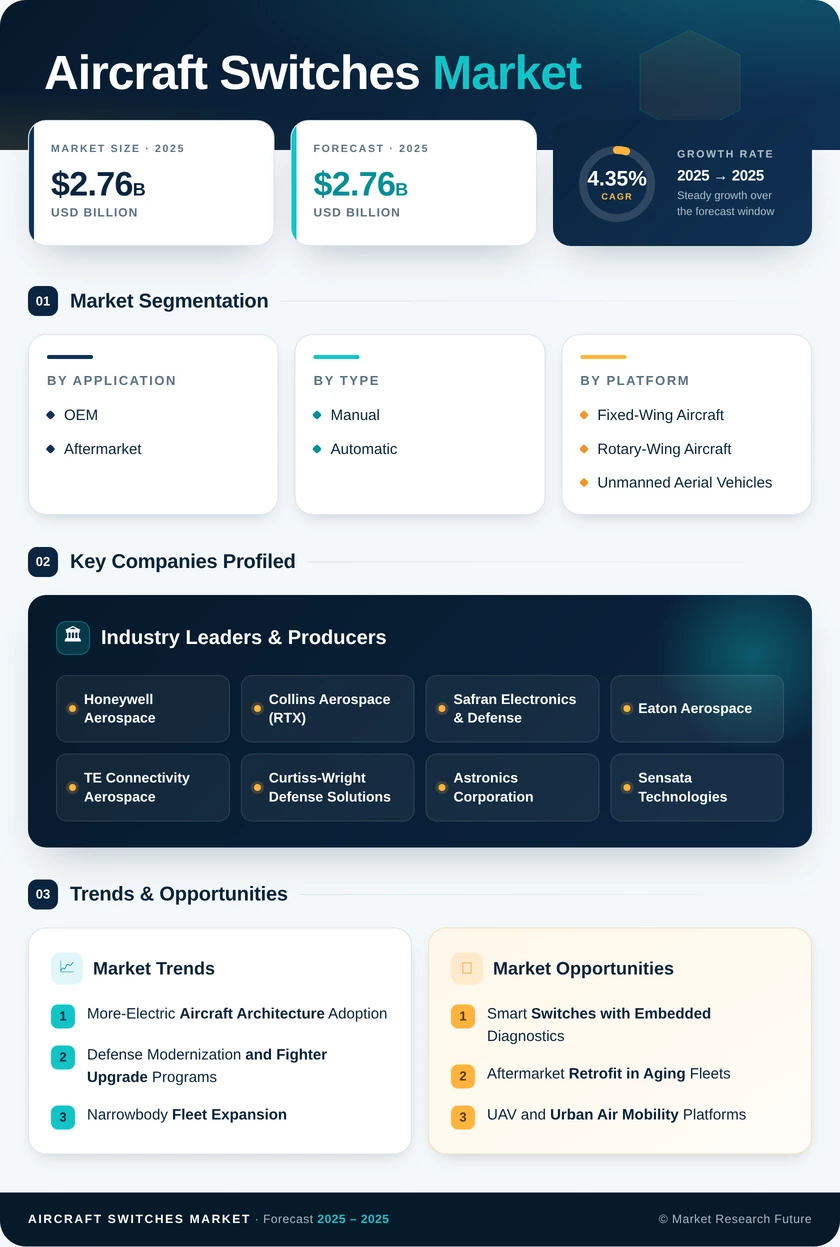

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Application | Cockpit, Cabin, Engine & APU, Avionics, Others | Cockpit (37.8% share, 2025) | Avionics (5.28% CAGR) |

| By Switch Type | Manual, Automatic | Manual (69.5% share, 2025) | Automatic (6.15% CAGR) |

| By Platform | Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles | Fixed-Wing Aircraft (73.1% share, 2025) | Unmanned Aerial Vehicles (6.72% CAGR) |

| By End User | OEM, Aftermarket | OEM (64.3% share, 2025) | Aftermarket (4.78% CAGR) |

| By Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (40.2% share, 2025) | Asia-Pacific (5.85% CAGR) |

Market Segmentation Overview

By Application

| Sub-Segment | Key Trend |

| Cockpit | Highest switch density per aircraft; pilot-interface concentration drives volume |

| Cabin | Growing demand for passenger-facing illuminated control panels and IFE switches |

| Engine & APU | Thermal-rated switching for FADEC integration and APU start sequences |

| Avionics | Glass-cockpit retrofits expanding cockpit avionics switches replacement cycles |

| Others | Landing gear, cargo door, and utility switching — stable, lower-growth niche |

Cockpit applications remain the revenue anchor as each widebody flight deck integrates 350–500 discrete switching units. Avionics switches are gaining share as airlines retrofit mid-life regional jets with integrated display systems requiring dedicated reversionary-mode controls.

By Switch Type

| Sub-Segment | Key Trend |

| Manual | Regulatory requirement for tactile pilot inputs on safety-critical functions |

| Automatic | Solid-state and software-actuated designs expanding with fly-by-wire adoption |

Manual switches dominate on installed base, but automatic switches deliver higher per-unit value and tighter integration with digital aircraft health-management platforms, positioning them for accelerating share gains through 2035.

By Platform

| Sub-Segment | Key Trend |

| Fixed-Wing Aircraft | Commercial narrowbody/widebody production lines drive bulk volume |

| Rotary-Wing Aircraft | Military helicopter upgrades sustain stable mid-tier demand |

| Unmanned Aerial Vehicles | Defense ISR and commercial cargo drones create fastest-growing demand pool |

Fixed-wing platforms account for the vast majority of switch consumption, but UAVs are growing at nearly double the overall market CAGR as military and commercial drone programs scale globally.

By End User

| Sub-Segment | Key Trend |

| OEM | New-build aircraft deliveries set switch quantities at point of manufacture |

| Aftermarket | Fleet aging drives replacement demand with higher-margin distribution channels |

OEM channels set the baseline for per-aircraft switch content, while the aftermarket provides a growing, margin-rich complement as global fleets age and undergo mandated avionics refreshes.

By Geography

| Sub-Segment | Key Trend |

| North America | Defense spending leadership and deep Aircraft Switches Market infrastructure sustain dominant share |

| Europe | Airbus supply chain and multi-nation fighter programs anchor second position |

| Asia-Pacific | Indigenous aircraft programs and Aircraft Switches Market build-out fuel fastest regional growth |

| South America | Embraer-centric demand with emerging regional airline fleet expansion |

| Middle East & Africa | Defense industrialization and Aircraft Switches Market hub competition drive incremental growth |

North America and Europe together represent roughly two-thirds of global revenue, while Asia-Pacific is closing the gap through aggressive fleet expansion and defense localization mandates across China, India, and South Korea.