Airport Security Market Summary

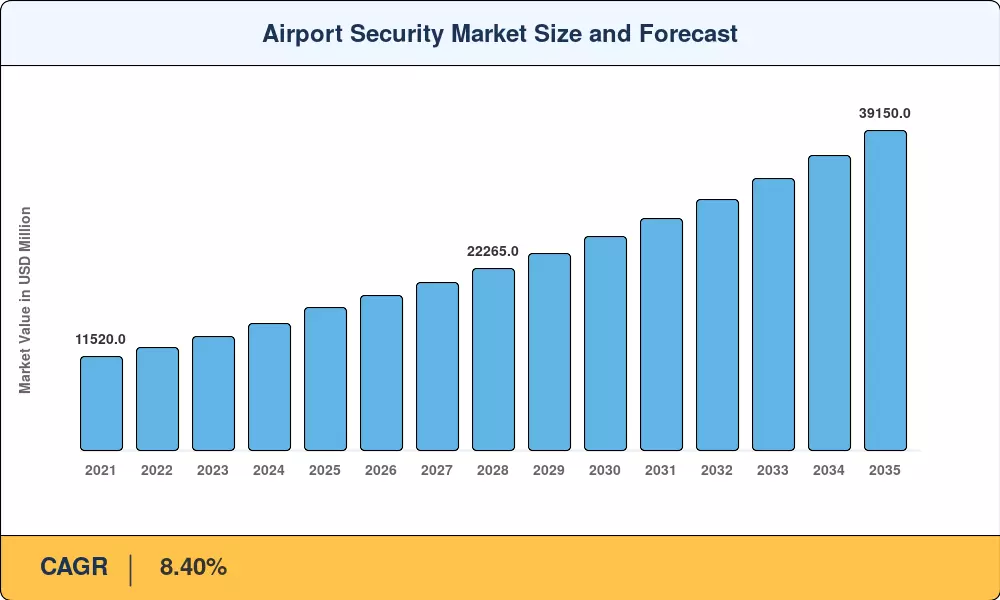

The Airport Security Market reached an estimated USD 17,480 million in 2025 and is projected to climb from USD 18,950 million in 2026 to USD 39,150 million by 2035, reflecting an 8.40% CAGR across the forecast window. A convergence of record passenger throughput — IATA forecasts global air traffic surpassing 9.4 billion trips annually by the early 2030s [1] — and tightened regulatory mandates from ICAO Annex 17 revisions [2] is channeling sustained capital into airport security infrastructure worldwide. Government appropriations in the United States alone exceeded USD 9.2 billion for the Transportation Security Administration in fiscal year 2024, underscoring the non-discretionary nature of this spending [3].

Computed-tomography cabin-baggage scanners, AI-based video analytics, and credential-authentication kiosks that match a traveler’s face against a photo ID in under two seconds [4] are replacing legacy metal-detector lanes and analog CCTV networks. The European Union’s revision of Regulation (EC) 300/2008 will require all EU airports to install Standard 3 screening technology by the year 2026, which is expected to cost an additional EUR 1.4 billion for new hardware acquisition [5]. These technology refreshes minimize curb-to-gate dwell times, lower staffing intensity per lane and move the Airport Security Market from a pure cost center into a revenue-protecting function that enables higher retail throughput in terminals.

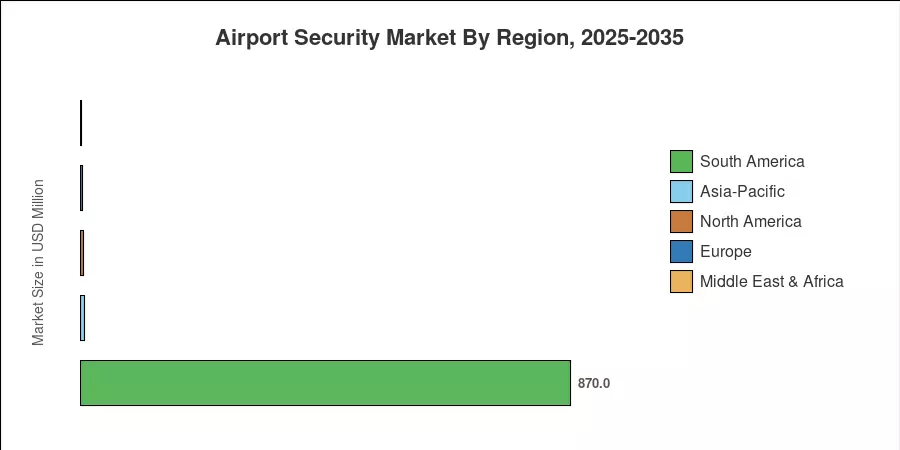

The Asia-Pacific region is estimated to contribute about 39.2% of the Airport Security Market revenue owing to the greenfield mega-hub construction in China and India. The Middle East & Africa region is the fastest-growing region, driven by projects such as the King Salman International Airport in Riyadh. At the same time, North America is the second largest regional contributor with around 28.5% of the market, driven by continuous TSA modernization cycles. Over the next 10 years, the adoption of subscription-based security technologies and cloud-native command centers will revolutionize procurement methods across all levels of airports.

Key Report Takeaways

• By Security System

- Screening and Scanning Systems held approximately 42.0% of the Airport Security Market share in 2025, driven by mandated CT scanner roll-outs across Tier-1 hubs.

- Access Control and Biometrics is forecast to expand at an 11.6% CAGR through 2035, the fastest among security-system segments.

• By Technology

- Hardware accounted for a dominant share of Airport Security Market spending in 2025, reflecting the capital intensity of scanner and sensor deployments.

- Software is poised to grow at a 12.5% CAGR through 2035 as AI analytics and cloud command platforms gain traction.

• By Geography

- Asia-Pacific held the largest revenue share of the Airport Security Market in 2025, led by China, India, and Japan.

- The Middle East & Africa region recorded the fastest projected CAGR, fueled by mega-airport construction pipelines.

Market Size and Forecast (2021–2035)

The market sizing uses a triangulated technique comprising top-down government procurement budgets, bottom-up airport capital expenditure declarations, and vendor revenue cross-checks spanning more than 350 airports globally. *Historical statistics (2021-2024) based on certified industry revenues; the base year 2025 was approximated from trailing twelve months data. Forecasts are based on the calibrated CAGR of 8.40% with modifications for regulatory catalysts and regional infrastructure timeframes.