Algae Products Market Summary

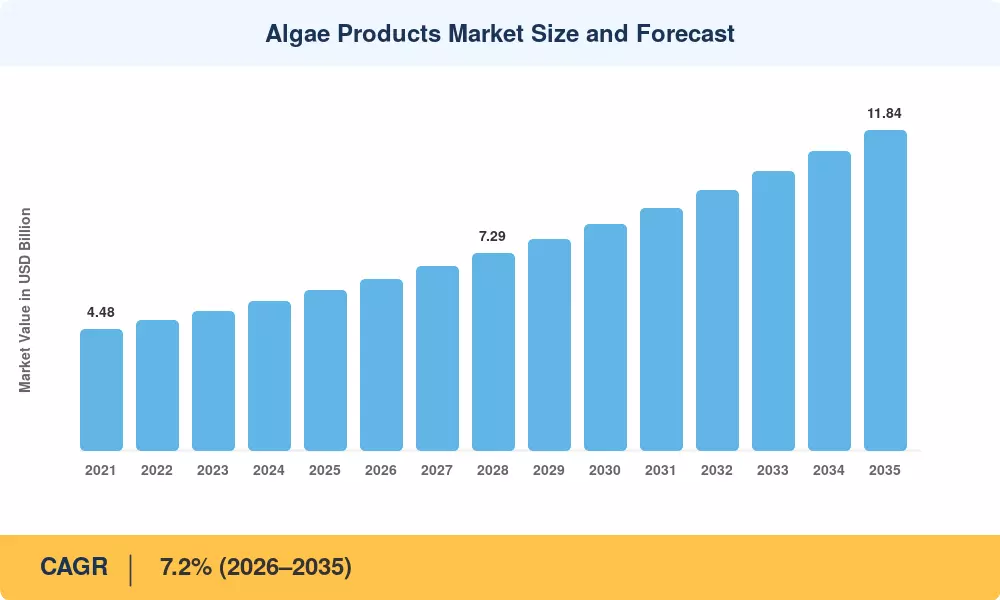

The Algae Products Market reached an estimated USD 5.92 billion in 2025 and is projected to grow from USD 6.35 billion in 2026 to USD 11.84 billion by 2035, registering a CAGR of 7.2% during the forecast period (2026–2035). This expansion is anchored by two converging forces: rising global demand for plant-based and sustainable nutrition, and aggressive government mandates targeting carbon-neutral fuels. The U.S. Department of Energy's USD 1.8 billion Bioenergy Technologies Office allocation and the EU's Farm to Fork Strategy have both placed algae-derived ingredients at the center of policy roadmaps [2][3].

The Algae Products Market is undergoing a massive change with the substitution of conventional petroleum-derived omega-3 supplements, synthetic food colorants, and soy-based protein isolates by spirulina chlorella superfood formulations, algae omega-3 DHA EPA oils, and microalgae protein supplement powders. Capital investment in closed-loop algae biorefineries is above USD 2.4 billion globally between 2022 and 2024 . These fermentation-based photobioreactor systems are replacing open pond culture at scale. The trend towards acquiring seaweed carrageenan ingredients for clean-label food processing has gained significant momentum, with more than 320 new product launches referring to algae-based thickeners in 2024 alone [5].

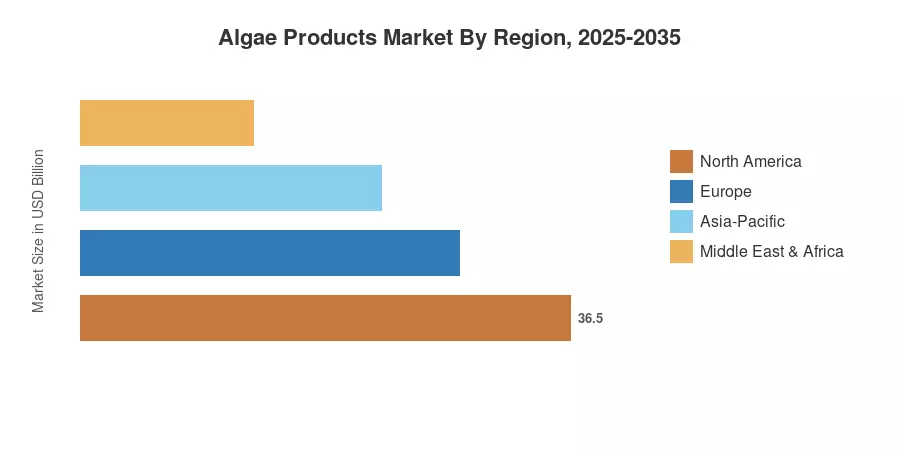

North America has a share of over 34% in the Algae Products Market. The United States is leading the demand for nutraceuticals and algae biofuel production research. Asia-Pacific is the fastest-growing area with a projected CAGR of 8.9%, driven by China’s spirulina chlorella superfood exports and India’s developing seaweed farming corridor. Europe is second with roughly 27%, with regulatory tailwinds for algal omega-3 DHA EPA in infant formula and functional beverages bolstering the pipeline through 2035

Key Report Takeaways

• By Product Type

- Dietary supplements — including spirulina, chlorella superfood tablets and microalgae protein supplement powders — account for approximately 38% of the Algae Products Market by revenue

- Algae biofuel production is the fastest-growing product segment, expanding at a CAGR of 9.4% through 2035

- Hydrocolloids, led by seaweed carrageenan ingredient applications, generate an estimated USD 1.28 billion in 2025

• By Source

- Microalgae (Spirulina, Chlorella, Haematococcus, Schizochytrium) dominate the Algae Products Market with roughly 55% share

- Macroalgae (brown, red, green seaweed) grow at a CAGR of 6.8%, driven by food and agriculture applications

• By Region

- North America leads with an estimated USD 2.01 billion in 2025 revenue

- Asia-Pacific registers the highest forecast CAGR of 8.9% in the Algae Products Market

- Europe captures approximately 27% of the global market share

Algae Products Market Size and Forecast (2021–2035)

MRFR's sizing methodology integrates bottom-up revenue modeling from 140+ algae producers, cross-validated against trade-flow databases (UN Comtrade, FAO FishStatJ), regulatory filings, and proprietary buyer surveys conducted across 28 countries. Historical figures (2021–2024) reflect actual trade data, while 2025 is estimated and 2026–2035 values are projected at a constant-currency CAGR of 7.2%.