Ammonium Nitrate Market Summary

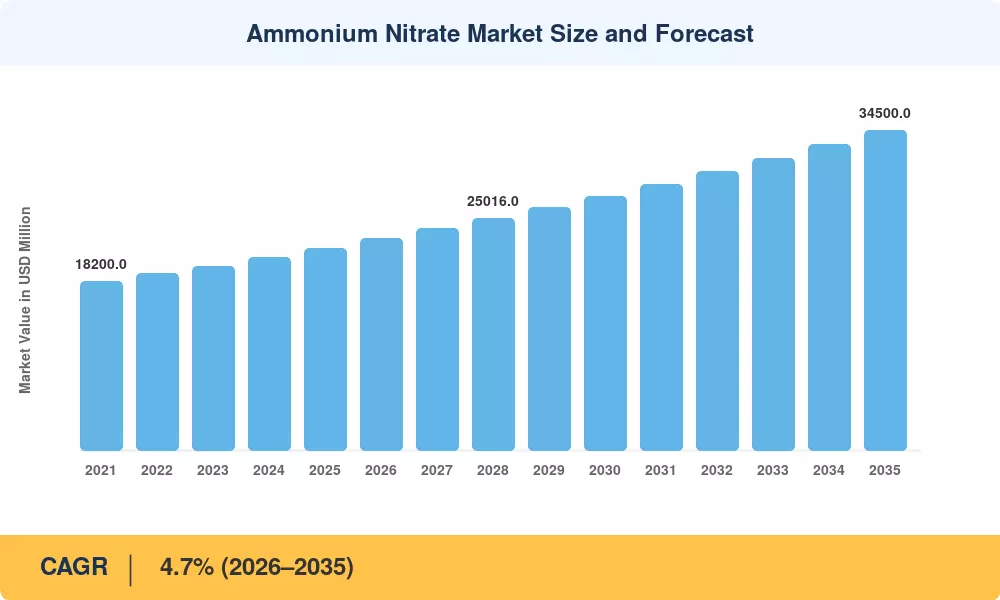

The global Ammonium Nitrate Market stood at an estimated USD 21,800 Million in 2025 and is projected to reach USD 22,820 Million by 2026, climbing to USD 34,500 Million by 2035 at a compound annual growth rate (CAGR) of 4.7% during the forecast period (2026–2035). Two forces are pulling this trajectory upward: tightening carbon-border adjustment mechanisms across the EU and North America that reward low-emission feedstock producers, and a sustained cycle of copper, lithium, and nickel mine development in South America and sub-Saharan Africa that is driving bulk explosive demand [1][2]. These catalysts are supported by national food-security mandates in India and Southeast Asia that continue to underpin fertilizer consumption volumes.

Precision-agriculture platforms are reshaping how ammonium nitrate reaches the field. Variable-rate application systems now guide coated-granule placement within centimeters, reducing per-hectare nitrogen waste by up to 18% while sustaining yield targets [3]. Blue and green ammonia facilities — with an estimated USD 14 billion in committed capital globally through 2030 — are beginning to alter the upstream cost curve for nitrate production, giving producers who invest early a carbon-intensity advantage under emerging embedded-carbon reporting frameworks [4].

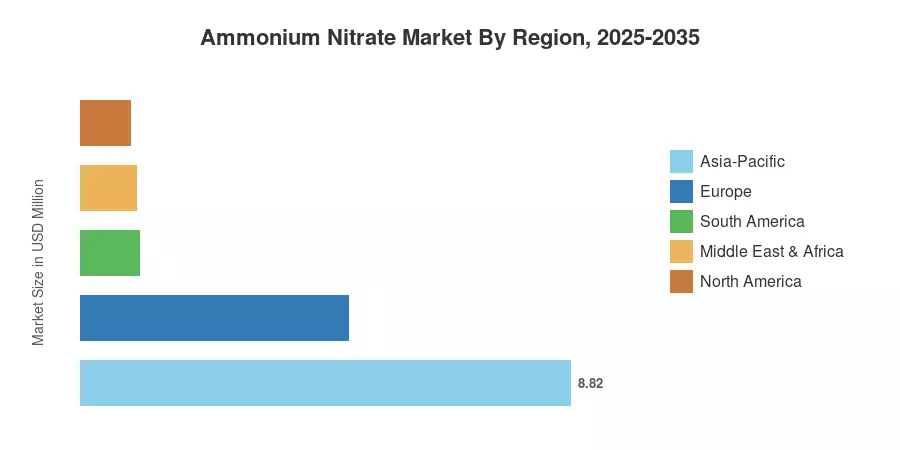

Asia-Pacific commands approximately 42% of the Ammonium Nitrate Market, anchored by China's and India's combined agricultural demand and a growing mining sector in Indonesia and Australia. The region also posts the fastest projected CAGR at 5.4%. Europe holds the second-largest share at roughly 23%, driven by established agrochemical supply chains in France, Germany, and Russia, though tighter EU REACH amendments are adding compliance costs. Africa and South America are the dark-horse regions to watch — new mine openings and fertilizer subsidy programs should accelerate volume growth beyond 2028.

Key Report Takeaways

• By Application

- Fertilizers accounted for the dominant application share of the Ammonium Nitrate Market in 2025, reflecting entrenched use in row-crop and cereal programs worldwide.

- The explosives segment is forecast to expand at a CAGR of 5.3% through 2035, fueled by deeper ore-body mining in copper and rare-earth projects.

• By Grade

- Fertilizers accounted for the dominant application share of the Ammonium Nitrate Market in 2025, reflecting entrenched use in row-crop and cereal programs worldwide.

- The explosives segment is forecast to expand at a CAGR of 5.3% through 2035, fueled by deeper ore-body mining in copper and rare-earth project

- Agricultural grade captured the leading share of the Ammonium Nitrate Market by grade in 2025, while industrial grade is tracking the fastest growth trajectory.

• By Form

- Porous prills held roughly 55% of total volume in 2025, driven by cost-effective production and broad compatibility with bulk blending systems.

- The granular segment is set to register a CAGR of 6.1% as precision-agriculture coatings gain traction.

• By End-User

- Porous prills held roughly 55% of total volume in 2025, driven by cost-effective production and broad compatibility with bulk blending systems.

- The granular segment is set to register a CAGR of 6.1% as precision-agriculture coatings gain traction.

- Agriculture represented the largest end-user segment of the Ammonium Nitrate Market, whereas mining is advancing at the highest end-user CAGR through 2035.

• By Region

- Asia-Pacific held the dominant Ammonium Nitrate Market share in 2025, supported by high-volume fertilizer consumption in China and India.

- South America is emerging as a high-growth corridor, driven by Brazilian soybean expansion and Chilean copper mine development.

Market Size and Forecast (2021–2035)

Market Research Future compiled historical revenue data from customs-trade databases, company annual reports, and industry associations for 2021–2024. Forecast values (2026–2035) apply a calibrated 4.7% CAGR, cross-referenced against IFA nitrogen-demand models and World Bank commodity price projections [1][5].