Animal Stem Cell Therapy Market Summary

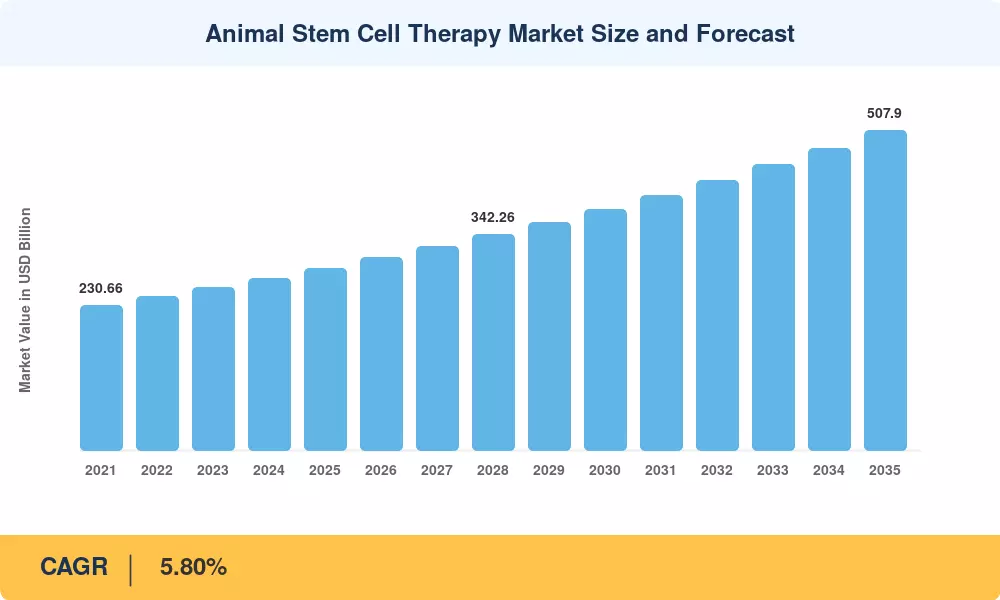

The Global Animal Stem Cell Therapy Market size was valued at USD 289.00 Million in 2025, and the market is projected to grow from USD 305.76 Million in 2026 to USD 507.90 Million by 2035, registering a CAGR of 5.80% during the forecast period 2026–2035. This expansion is anchored in the rising prevalence of chronic musculoskeletal conditions in companion animals — osteoarthritis alone accounts for roughly 80% of lameness cases in dogs and cats [2] — and a regulatory environment that has grown increasingly favorable toward veterinary regenerative medicine approvals in the United States, Europe, and parts of Asia-Pacific.

A visible shift is underway in how veterinary practitioners manage degenerative and inflammatory conditions. Traditional pharmacologic approaches — NSAIDs, corticosteroids, and surgical intervention — are gradually being supplemented, and in some clinical settings replaced, by pet stem cell treatment protocols that leverage mesenchymal stem cells (MSCs) harvested from adipose tissue or bone marrow. The USDA's Center for Veterinary Biologics has fast-tracked several autologous cell therapy licensing pathways since 2023, while the European Medicines Agency issued updated guidance on advanced therapy veterinary medicinal products (ATVMPs) valued at over EUR 12 million in compliance investment across the EU [3]. These catalysts are reshaping how capital flows into companion animal cell therapy research pipelines.

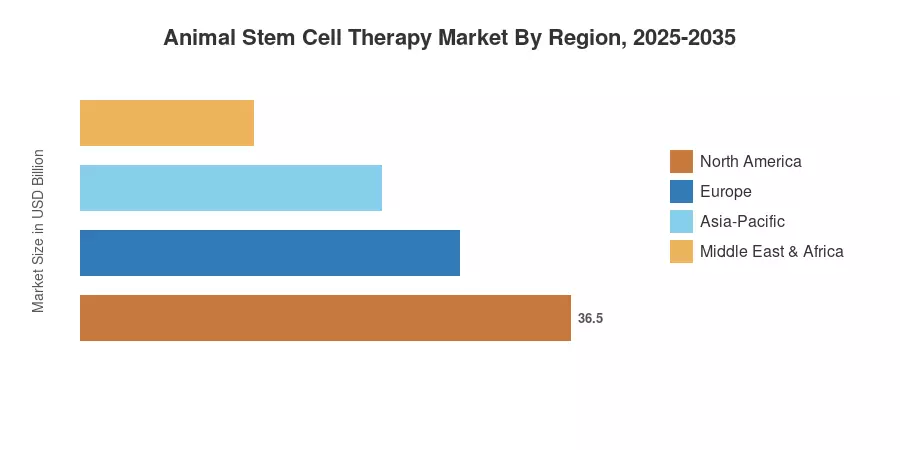

North America commands approximately 38% of the global animal stem cell therapy market, driven by high pet insurance penetration and a dense network of specialty veterinary hospitals. Asia-Pacific stands as the fastest-growing region with a projected CAGR of 7.2%, fueled by rapid urbanization and rising pet ownership across China, India, and South Korea. Europe holds the second-largest share at roughly 27%, led by Germany and the United Kingdom, where equine stem cell therapy adoption in sport-horse medicine has been particularly robust The decade ahead will reward early movers who can scale manufacturing, secure regulatory clearance across multiple geographies, and build clinical evidence that persuades both veterinarians and pet owners.

Key Report Takeaways

• By Type

- Autologous stem cell therapies captured the leading share of the animal stem cell therapy market at approximately 58% in 2025, driven by lower immunological rejection risk and established clinical protocols in veterinary regenerative medicine

- Allogeneic therapies are projected to register a CAGR of 6.90% through 2035, as off-the-shelf convenience appeals to high-volume veterinary clinics seeking scalable pet stem cell treatment options

• By Application

- Osteoarthritis dominated application-level revenue within the animal stem cell therapy market, reflecting the condition's outsized prevalence in aging companion animal populations

- Tendonitis applications are expanding rapidly in the equine stem cell therapy segment, particularly in North America and Western Europe, where sport-horse expenditure remains high

• By Region

- North America accounted for the largest regional share at 38%, anchored by the United States' advanced veterinary infrastructure and favorable reimbursement dynamics

- Asia-Pacific is forecast to grow at a CAGR of 7.2%, making it the fastest-growing region in the animal stem cell therapy market through 2035

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates top-down revenue estimates from company filings and veterinary industry databases with bottom-up demand modeling based on addressable patient populations, treatment penetration rates, and average procedure pricing across geographies. Historical data (2021–2024) reflects actual reported revenues; the 2025 base year blends preliminary actuals with model-derived estimates; forecast years (2026–2035) apply a calibrated CAGR adjusted for macroeconomic, regulatory, and technology adoption assumptions.

.webp?v=1782976095)