Automatic Identification System Market Summary

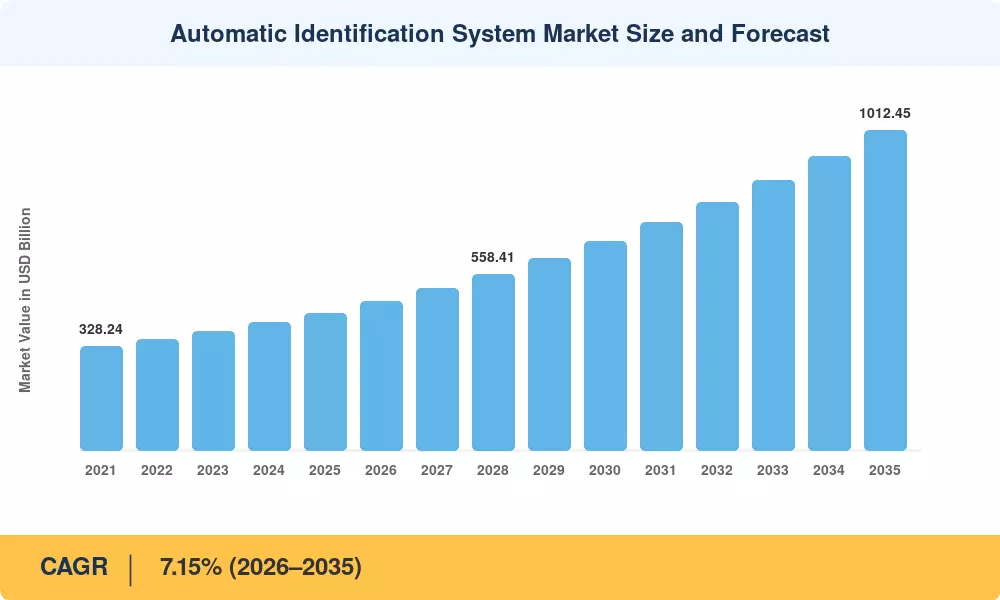

The Automatic Identification System Market reached an estimated USD 432.71 million in 2025 and is projected to climb to USD 461.36 million in 2026 before expanding to USD 1,012.45 million by 2035, registering a CAGR of 7.15% across the 2026–2035 forecast window. Two catalysts anchor this trajectory: the International Maritime Organization's (IMO) progressive widening of AIS carriage requirements beyond SOLAS-class vessels and the rapid build-out of satellite AIS constellations that are closing persistent coverage gaps across open-ocean corridors[2]. Governments worldwide allocated over USD 1.8 billion to port modernization and vessel traffic management AIS upgrades between 2022 and 2024, reflecting a decisive policy pivot toward digitalized maritime surveillance [3].

Legacy radar-only coastal monitoring is giving way to hybrid architectures that fuse terrestrial AIS base stations with satellite AIS feeds and AI-driven anomaly detection. The European Maritime Safety Agency's (EMSA) CleanSeaNet program, for example, now ingests AIS data analytics platform outputs to cross-reference vessel positions with synthetic-aperture-radar imagery, a model being replicated across Southeast Asian and Latin American coastguards [4]. Ship transponder AIS receiver technology has simultaneously evolved from single-channel VHF units to multi-channel, software-defined transceivers capable of handling AIS messages alongside VDES digital exchanges.

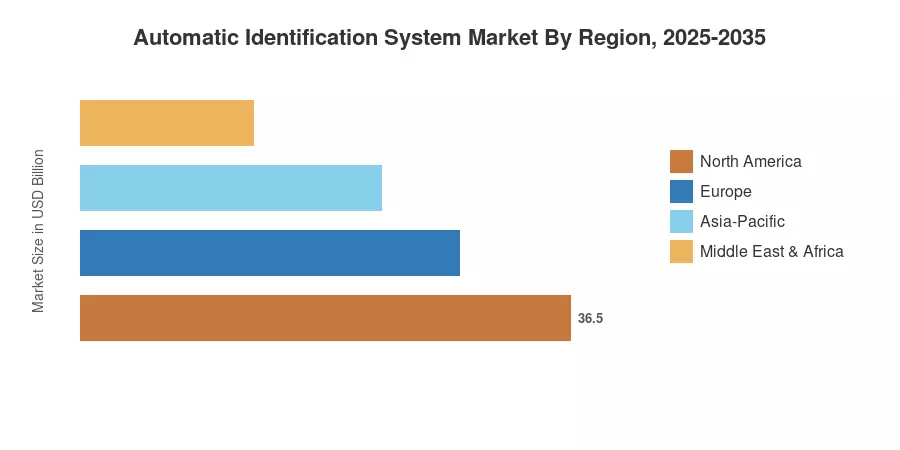

Asia-Pacific commands roughly 44.28% of global revenue, driven by China's smart-port initiative and India's Sagarmala port-led development program. South America is the fastest-growing region in the Automatic Identification System Market, posting a projected CAGR of 8.10%, as Brazil and Argentina modernize aging coastal AIS network infrastructure Europe holds the second-largest share at approximately 24.5%, underpinned by EU mandates on emissions monitoring that rely on AIS-derived voyage data. The next decade will see the convergence of AIS maritime vessel tracking with autonomous navigation systems reshape competitive dynamics across every major waterway.

Key Report Takeaways

• By Application

- Vessel Tracking and Monitoring accounted for 40.35% of the Automatic Identification System Market in 2025, reflecting the universal regulatory mandate for real-time ship transponder AIS receiver carriage on commercial tonnage

- Maritime Security and Search-and-Rescue (SAR) is projected to grow at an 8.18% CAGR through 2035, as coastguards invest in AIS data analytics platform capabilities for threat detection

- Fleet Management solutions reached approximately USD 105.6 million in 2025, buoyed by logistics operators embedding AIS maritime vessel tracking feeds into route-optimization engines

• By Platform & Component

- Vessel-based AIS transponders held 76.10% share in the Automatic Identification System Market in 2025, underpinned by mandatory carriage regulations for SOLAS vessels

- Class B Transponders are expanding at an 8.12% CAGR through 2035, driven by voluntary adoption among fishing fleets and recreational craft

• By Solution

- Terrestrial AIS held a dominant 61.45% share of the Automatic Identification System Market in 2025, anchored by established coastal AIS network deployments in Europe and North America

- Satellite AIS (Sat-AIS) is on track for an 8.52% CAGR through 2035 as LEO constellation operators expand maritime coverage

• By Region

- Asia-Pacific commanded a 44.28% share of the Automatic Identification System Market in 2025

- South America is projected to register the fastest regional CAGR of 8.10% over 2026–2035

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue modeling from equipment OEMs, satellite service providers, and vessel traffic management AIS software vendors with top-down validation against IMO fleet registries and national maritime authority budgets. Historical figures (2021–2024) derive from audited company filings and trade-association databases; forecast figures (2026–2035) apply segment-level CAGR projections calibrated against policy-pipeline analysis.

.webp?v=1783339232)