Automotive ANC Systems Market Summary

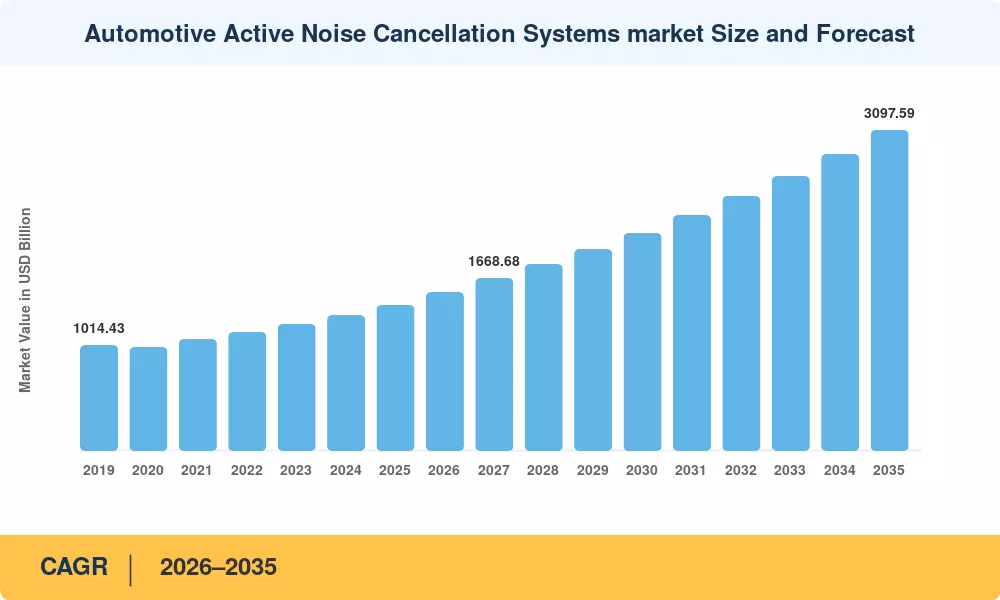

The global Automotive Active Noise Cancellation (ANC) Systems market was valued at USD 1,403.34 billion in 2025 and is projected to reach USD 3,097.59 billion by 2035, registering a compound annual growth rate (CAGR) of 8.15% during the forecast period 2026–2035. The market crossed the USD 1,529.84 billion threshold in 2026, the first year of the forecast window. Structural growth is underpinned by the accelerating global shift toward electric vehicles (EVs), which inherently lack internal-combustion-engine masking noise and therefore expose occupants to road and wind noise that must be actively managed. Concurrently, original equipment manufacturers (OEMs) pursuing aggressive lightweighting strategies are replacing heavy passive insulation materials—such as dense bitumen pads and mass-loaded vinyl barriers—with electronically driven ANC solutions that deliver superior noise attenuation at a fraction of the weight penalty. Consumer expectations for premium cabin acoustics have risen sharply, reinforced by the proliferation of in-car infotainment systems, voice-activated digital assistants, and hands-free communication features that demand a low-noise acoustic environment to function reliably.

From a technology standpoint, hybrid ANC architectures—combining feedforward and feedback signal paths—have emerged as the dominant technology segment, capturing the largest share of 2025 revenue. Hybrid systems leverage multiple reference microphones placed at the vehicle's exterior surfaces alongside error microphones inside the cabin to generate phase-inverted anti-noise signals in real time, yielding broadband cancellation across engine, road, and wind noise spectra. The fastest-growing technology segment is AI-enhanced adaptive ANC, propelled by recent strategic moves such as Analog Devices' August 2025 acquisition of an automotive AI audio processing startup that strengthens adaptive DSP and intelligent cabin acoustics capabilities, and NXP Semiconductors' June 2025 launch of an upgraded S32 automotive processing platform engineered for high-performance ANC workloads and AI-driven smart cockpit applications. These developments signal a clear trajectory toward software-defined, over-the-air-updatable noise management systems embedded within centralized vehicle compute architectures.

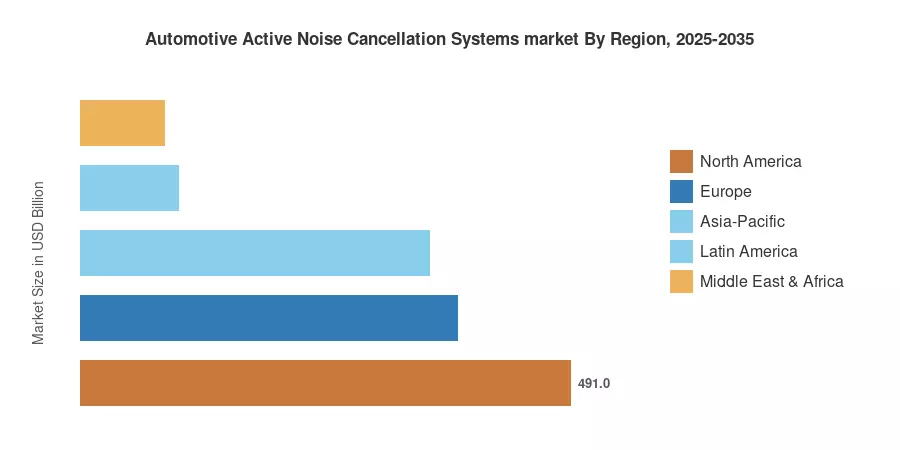

Regionally, North America commands the largest revenue share, driven by high consumer willingness to pay for premium vehicle features, a mature OEM ecosystem, and the rapid expansion of the North American EV market. Asia-Pacific is the fastest-growing region with the highest forecast CAGR, fueled by surging EV production in China, South Korea, and Japan, rising per-capita income supporting premiumization in India and Southeast Asia, and the strategic investments of regional tier-one suppliers such as Hyundai Mobis, which in December 2025 acquired a South Korean EV acoustic engineering firm to bolster its road-noise-reduction and vibration-optimization portfolio. Europe holds the second-largest market position, supported by stringent noise-pollution directives and strong demand for luxury and premium vehicles equipped with advanced cabin technologies. Looking ahead, the convergence of electrification, autonomous driving, and connected-vehicle platforms is expected to sustain double-digit growth pockets within the ANC market well into the next decade.

Key Report Takeaways

| Segment Dimension | Key Metric | Notes |

| Technology Type — Dominant | Hybrid ANC held the largest 2025 revenue share | Broadband cancellation across engine, road, and wind noise |

| Technology Type — Fastest Growing | AI-Enhanced Adaptive ANC, highest CAGR 2026–2035 | Driven by ADI and NXP platform launches |

| Vehicle Type — Dominant | Passenger Cars, the largest 2025 segment | Consumer premiumization and EV sedan proliferation |

| Vehicle Type — Fastest Growing | Heavy Commercial Vehicles, the highest CAGR | Regulatory push for driver-cabin comfort in long-haul transport |

| Propulsion Type — Dominant | ICE Vehicles, the largest installed base in 2025 | The legacy fleet is still dominant, though its share is declining |

| Propulsion Type — Fastest Growing | Electric Vehicles, the highest CAGR | Absence of engine masking noise creates structural demand |

| Application — Dominant | Road Noise Cancellation, largest 2025 share | Critical for EVs and lightweight vehicle architectures |

| Application — Fastest Growing | Wind Noise Cancellation, the highest CAGR | Growing importance of aerodynamic EV designs |

| Sales Channel — Dominant | OEM (factory-installed), largest 2025 share | Deep integration with vehicle ECU and audio systems |

| Sales Channel — Fastest Growing | Aftermarket, the highest CAGR | Retrofit kits expanding for mid-cycle and used EV markets |

| Region — Dominant | North America, ~35% of 2025 global revenue | Premium vehicle mix and high EV adoption rates |

| Region — Fastest Growing | Asia-Pacific, the highest regional CAGR | China/Korea EV production boom and tier-one supplier investment |

Market Size and Forecast (2019–2035)

MRFR's market sizing methodology combines a bottom-up revenue model aggregating OEM installation rates, average system selling prices, and aftermarket retrofit volumes across five geographic regions with a top-down cross-validation using supplier revenue disclosures, component shipment data, and patent filings. The base-year (2025) estimate is triangulated against primary interviews with tier-one audio system integrators and secondary sources, including automotive production databases, OEM annual reports, and industry association publications. Forecast-period projections apply segment-specific growth assumptions incorporating EV penetration curves, regulatory timelines, and technology adoption S-curves.