Automotive Display Market Summary

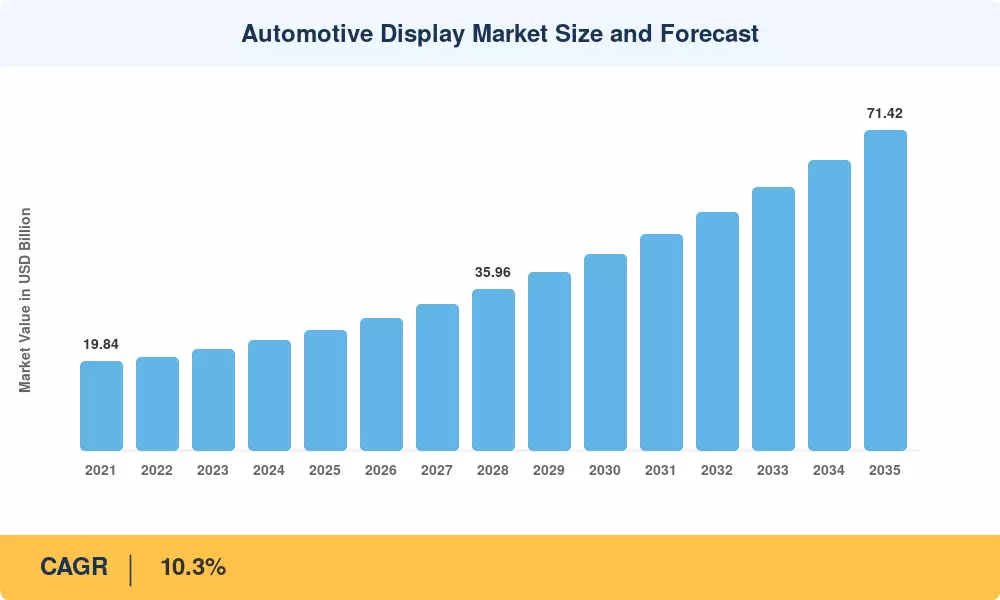

The Automotive Display Market reached an estimated USD 26.80 billion in 2025 and is projected to expand from USD 29.56 billion in 2026 to USD 71.42 billion by 2035, registering a compound annual growth rate of 10.3% across the forecast window. Two structural forces anchor this trajectory: the rapid electrification of passenger fleets the IEA projects global EV sales surpassing 20 million units by 2026 [1] and the parallel shift toward software-defined vehicle architectures that demand higher-resolution, larger-format cockpit screens.

Legacy analog gauge clusters and single-purpose infotainment units are giving way to integrated digital cockpits where a unified computing platform drives instrument clusters, center stacks, heads-up displays, and passenger screens simultaneously. Continental AG's investment of over EUR 1 billion in its automotive HMI division between 2023 and 2025 signals the capital intensity required to serve this transition [2]. Regulatory action is also accelerating adoption: Euro NCAP's Driver Engagement Protocol v1.0 now awards safety credits for augmented-reality head-up displays, prompting OEMs to specify display-rich dashboards across mid-range trims [3].

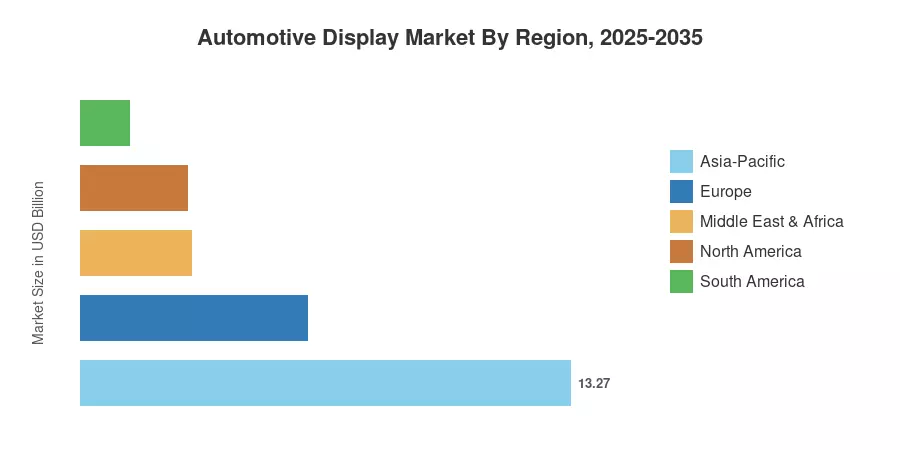

Asia-Pacific commands roughly 49.5% of the Automotive Display Market, propelled by Chinese EV production and panel-maker capacity expansions from BOE and CSOT. Europe holds the second-largest share at approximately 23%, driven by premium German automakers embedding wide-format screens. North America, accounting for about 19%, is the fastest-accelerating Western region as connected-vehicle mandates from NHTSA expand digital instrument requirements [4]. The decade ahead will be defined by how quickly OLED cost curves converge with LCD pricing — and which suppliers capture the resulting volume swing.

Key Report Takeaways

• By Product Type & Display Technology

- Center stack displays accounted for approximately 43% of the Automotive Display Market in 2025, underscoring their role as the primary HMI surface in modern cockpits.

- Head-up displays are forecast to advance at a 10.8% CAGR through 2035, benefiting from Euro NCAP incentives and AR overlay integration.

- Liquid crystal displays represented roughly 61% of total display shipments by value in 2025, although OLED units are expanding at an 11.5% CAGR as manufacturing yields improve.

• By Vehicle Type & Display Size

- Passenger cars dominated the Automotive Display Market with an estimated 81% share in 2025.

- Panels exceeding 10 inches are projected to grow at a 12.0% CAGR through 2035, reflecting OEM preference for wide-format and curved installations.

• By Region

- Asia-Pacific captured approximately 49.5% of the Automotive Display Market in 2025, with China alone representing over half of the regional revenue.

- Commercial vehicles constitute the fastest-growing end-use segment globally, registering a 12.6% CAGR as fleet operators digitize dashboards.

Automotive Display Market Size and Forecast (2021–2035)

Market estimates draw on a triangulated methodology combining OEM procurement data, panel-maker shipment disclosures, and tier-1 integrator revenue filings, cross-validated against vehicle production volumes from OICA and regional trade statistics.