Automotive Engine Encapsulation Market Summary

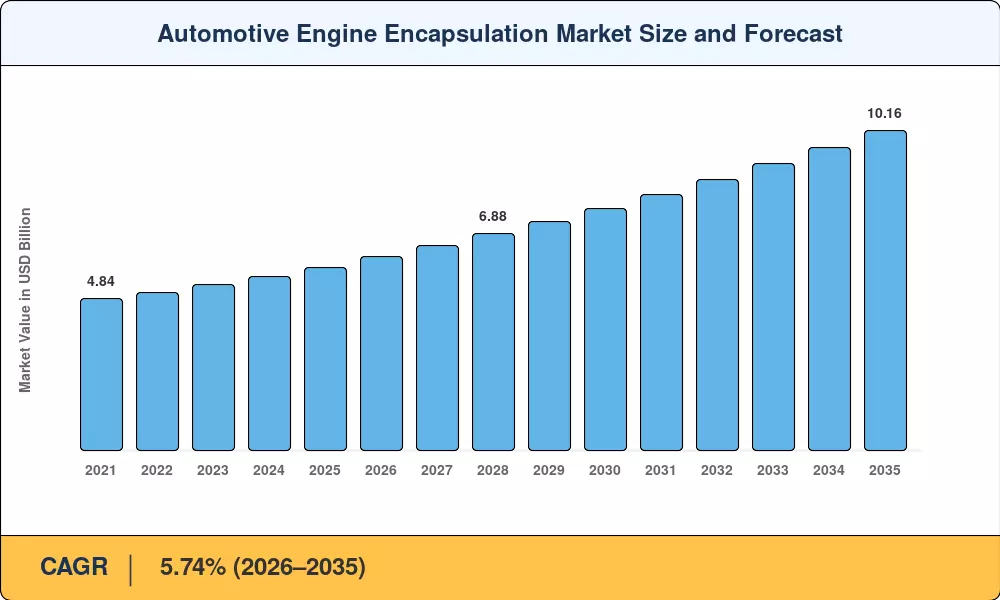

The Automotive Engine Encapsulation Market was valued at USD 5.82 Billion in 2025 and is projected to reach USD 6.15 Billion in 2026 before climbing to USD 10.16 Billion by 2035, registering a CAGR of 5.74% during 2026–2035. Tightening Euro 7 cold-start emissions limits and California's Advanced Clean Cars II mandate are compelling automakers to treat under-hood thermal retention as a compliance necessity rather than a premium add-on. That regulatory tailwind, combined with OEM commitments exceeding USD 515 billion to electrification programs globally through 2030 [1], is reshaping how powertrains are packaged and insulated.

A fundamental shift in encapsulation design is underway. Legacy single-layer fiberglass covers are giving way to multi-functional composite assemblies that simultaneously manage heat retention, cabin noise attenuation, and aerodynamic drag. Digital-twin simulation loops now allow engineers to merge structural, thermal, and acoustic functions into fewer components, reducing part counts by 15–20% on new-generation platforms [2]. Gigacasting adoption by leading EV manufacturers has further accelerated the integration of encapsulation elements into underbody mega-castings.

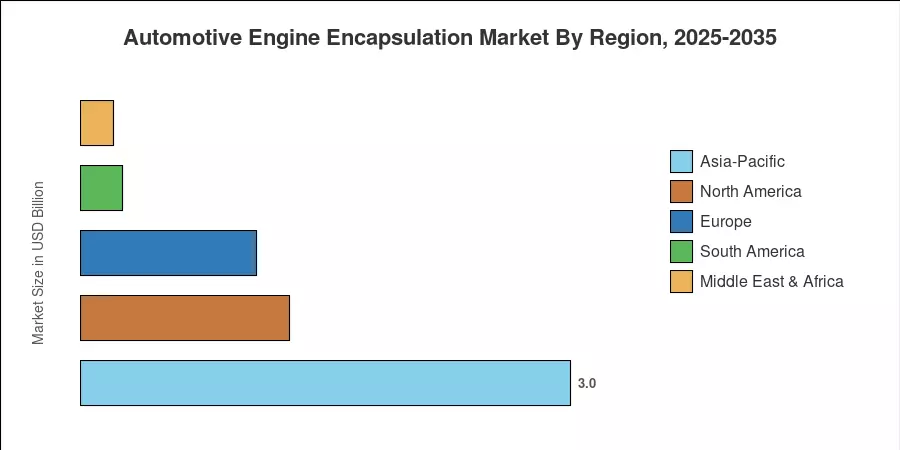

Asia-Pacific dominated the Automotive Engine Encapsulation Market with an estimated 51.5% share in 2025, driven by China's 28-million-unit annual vehicle output and India's Production-Linked Incentive scheme for auto components [3]. Europe held the second-largest share at roughly 18.5%, where premium German OEMs set the pace on NVH standards. Asia-Pacific is also the fastest-growing region at an 8.75% CAGR, with the market poised to benefit as Southeast Asian assembly hubs scale production through the forecast period.

Key Report Takeaways

• By Product Type

- Engine-mounted encapsulation systems accounted for 54.7% of the Automotive Engine Encapsulation Market in 2025, reflecting their critical role in cold-start thermal management.

- Body-mounted designs are projected to grow at a 7.84% CAGR through 2035 as lightweight platforms integrate encapsulation into structural body panels.

• By Material

- Carbon fiber composites captured 36.6% of the Automotive Engine Encapsulation Market share in 2025, supported by declining precursor costs.

• By Fuel Type

- Carbon fiber composites captured 36.6% of the Automotive Engine Encapsulation Market share in 2025, supported by declining precursor costs.

- Electric and hybrid powertrain encapsulation segments are advancing at an 8.14% CAGR, the fastest across fuel categories.

• By Region

- Asia-Pacific commanded over half of the Automotive Engine Encapsulation Market revenue in 2025 and leads the growth trajectory at 8.75% CAGR.

- North America represented approximately 22.0% of global revenue, propelled by pickup truck and SUV thermal management upgrades.

Market Size and Forecast (2021–2035)

Market Research Future's estimation framework combines bottom-up supplier revenue triangulation with top-down vehicle production multipliers, cross-validated against OEM procurement disclosures and trade association data.