Automotive Seat Belt Pretensioner Market Summary

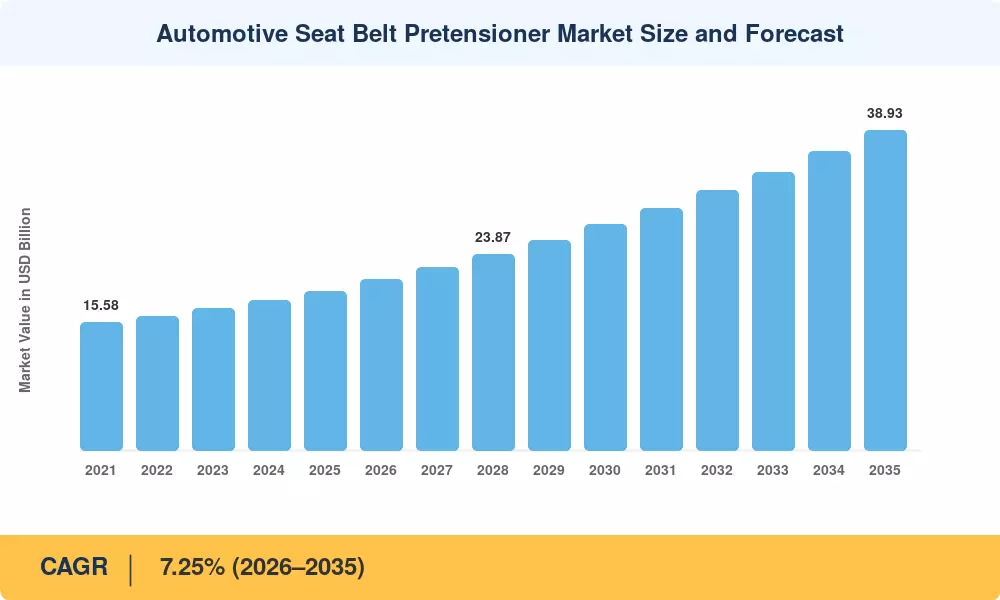

The Automotive Seat Belt Pretensioner Market was valued at USD 19.35 billion in 2025, with forecast-period revenues beginning at USD 20.75 billion in 2026 and climbing to USD 38.93 billion by 2035, registering a CAGR of 7.25% across the 2026–2035 window. Two catalysts anchor this trajectory: first, the World Health Organization's continued documentation of roughly 1.35 million annual road-traffic fatalities worldwide has intensified regulatory pressure on passive-restraint upgrades [1]; second, the European Union's General Safety Regulation (GSR 2), which entered force in July 2024, mandates advanced occupant-protection features in every new vehicle sold in the bloc, directly expanding pretensioner attach rates [2].

Technology transformation in the Automotive Seat Belt Pretensioner Market centers on the migration from purely mechanical, single-stage activators toward electronically controlled, multi-stage pretensioner units that communicate with the vehicle's central crash-sensing architecture. Legacy single-fire gas generators are giving way to dual-stage and adaptive systems capable of modulating belt tension based on occupant size and collision severity. Continental AG alone allocated over EUR 180 million in 2024 to next-generation restraint electronics, signaling the scale of R&D commitment across Tier-1 suppliers [3].

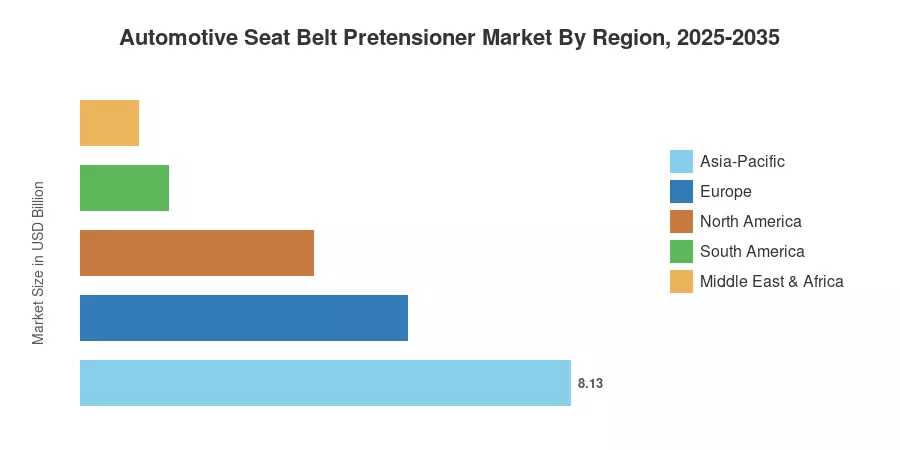

Asia-Pacific dominates the Automotive Seat Belt Pretensioner Market with approximately 42% of global revenue, driven by record vehicle production in China and India. The region is also the fastest-growing, posting a projected CAGR of 8.10% through 2035 as Bharat NCAP and China NCAP tighten crash-test protocols [4]. Europe holds the second-largest share at roughly 28%, underpinned by stringent EU type-approval standards and a mature supplier base. North America accounts for about 20%, with NHTSA rulemaking on enhanced frontal-impact protection providing a sustained demand floor. As electrification reshapes vehicle architectures, pretensioner integration with battery management and advanced driver-assistance systems will open the next wave of value creation across all regions.

Key Report Takeaways

• By Technology

- Retractor pretensioners command an estimated 62% revenue share of the Automotive Seat Belt Pretensioner Market, benefiting from universal OEM specification in front-seat applications.

- Buckle pretensioners are projected to grow at a CAGR of 8.45% through 2035, accelerated by rear-seat safety mandates in Europe and Asia.

• By Sector

- Passenger cars represent roughly USD 14.32 billion of the 2025 Automotive Seat Belt Pretensioner Market, reflecting higher per-vehicle pretensioner content than commercial platforms.

- The OEM channel captures approximately 85% of total demand, while aftermarket replacement volumes are expanding as vehicle parc ages globally.

• By Region

- Asia-Pacific leads the Automotive Seat Belt Pretensioner Market at around 42% share, with China alone contributing more than half of the regional revenue.

- Europe's share stands near 28%, reinforced by the EU GSR 2 mandate requiring advanced pretensioner integration on all new models.

- South America posts the second-highest regional CAGR at 7.55%, driven by Brazil's expanding NCAP adoption.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates bottom-up production volumes from OICA datasets, Tier-1 supplier revenue disclosures, and regulatory attach-rate models. Historical figures (2021–2024) are derived from audited financial statements and customs trade data; forecast values (2026–2035) apply a constant CAGR of 7.25%, adjusted for anticipated regulatory step-changes in 2027 and 2031.