Automotive Steel Wheels Market Summary

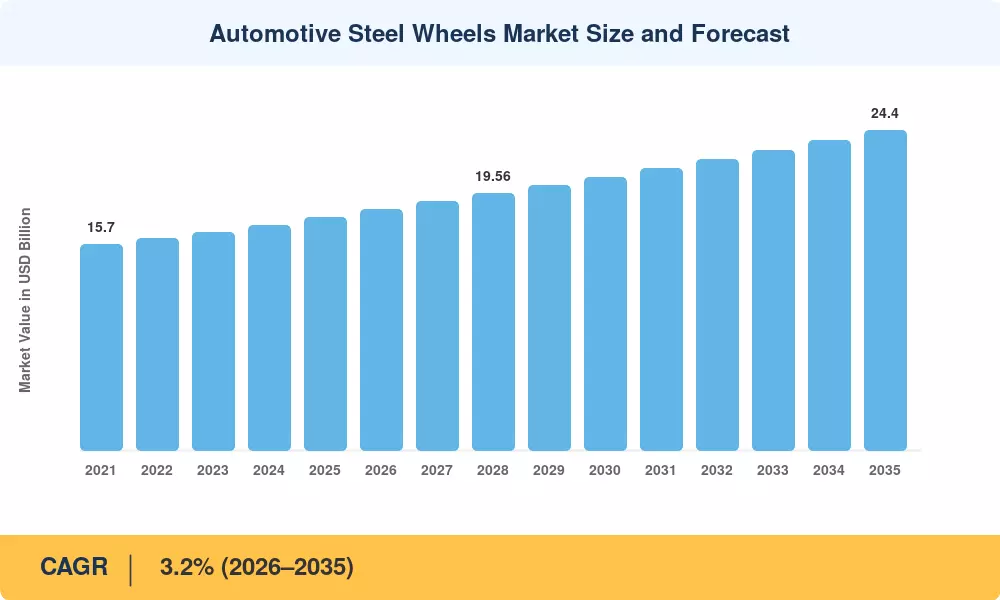

The Automotive Steel Wheels Market was valued at USD 17.80 billion in 2025 and is projected to grow from USD 18.37 billion in 2026 to USD 24.40 billion by 2035, registering a CAGR of 3.2% during the forecast period (2026–2035). Rising commercial vehicle production across emerging economies and government infrastructure spending programs — including India's USD 1.3 trillion National Infrastructure Pipeline and China's 14th Five-Year Plan logistics targets — continue to underpin demand for cost-effective steel wheel solutions [1][2]. The Automotive Steel Wheels Market benefits from the sheer volume of budget-segment vehicles produced annually, where steel remains the default wheel material.

Steel wheels are not being replaced so much as repositioned. While alloy alternatives dominate premium passenger segments, advances in steel forming technology — flow-forming and single-piece stamping — have reduced per-unit weight by 10–15% over the past decade, narrowing the performance gap [3]. OEMs increasingly specify high-strength low-alloy (HSLA) steels that meet crash-safety and load-rating requirements at roughly 40–60% lower cost than equivalent aluminum designs [4].

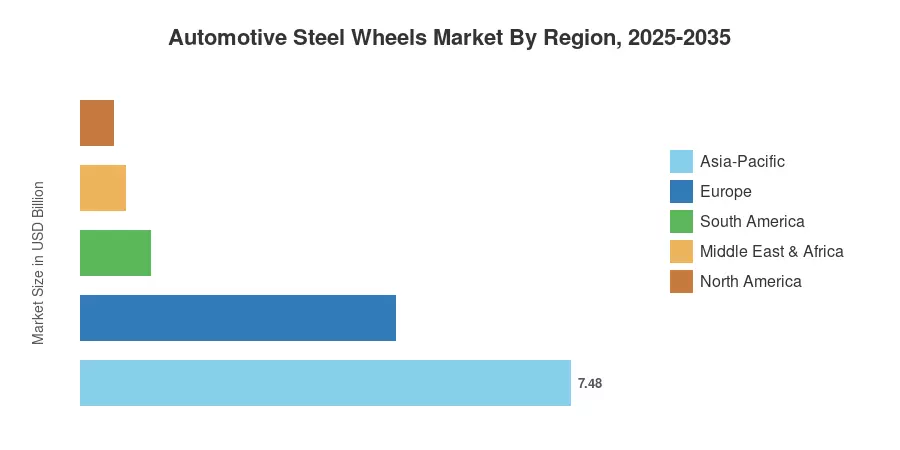

Asia-Pacific commands roughly 42% of the global Automotive Steel Wheels Market, driven by vehicle production hubs in China, India, and Southeast Asia. Europe holds an estimated 27% share, anchored by commercial fleet replacement cycles and EU CO₂ fleet-emission targets that keep lighter steel variants competitive [5]. North America represents approximately 20% of the market, while South America and the Middle East & Africa account for the balance. The fastest growth through 2035 is expected in Asia-Pacific, with a regional CAGR of 4.1%, as infrastructure investment and urbanization accelerate truck and bus demand.

Key Report Takeaways

• By Vehicle Type

- Passenger cars account for the largest share of the Automotive Steel Wheels Market at approximately 52% of global revenue, sustained by a high-volume economy and mid-segment production.

- Heavy commercial vehicles represent the fastest-growing segment with a CAGR of 4.3%, reflecting fleet expansion in logistics-intensive markets.

- Light commercial vehicles contributed USD 3.90 billion in 2025, supported by last-mile delivery fleet build-outs.

• By Sales Channel

- OEM sales dominate the Automotive Steel Wheels Market, holding roughly 68% share, as steel wheels remain standard fitment across base-trim and fleet models.

- The aftermarket segment is projected to grow at a CAGR of 3.6%, driven by replacement demand in aging vehicle populations across Latin America and South Asia.

• By Region

- Asia-Pacific leads the Automotive Steel Wheels Market with a 42% revenue share in 2025.

- Europe remains the second-largest region, valued at USD 4.81 billion.

- North America's market grows at a CAGR of 2.8%, shaped by pickup-truck and Class 8 truck volumes.

Market Size and Forecast (2021–2035)

Data in this section is compiled from OEM production statistics, trade association records (OICA, ACEA), customs data, and primary interviews with wheel manufacturers. Historical values (2021–2024) reflect actual shipments; the base year (2025) blends preliminary shipment data with econometric modeling. Forecast projections apply a weighted compound growth model calibrated to vehicle production outlooks published by IHS Markit and LMC Automotive[7].