Autonomous Navigation Market Summary

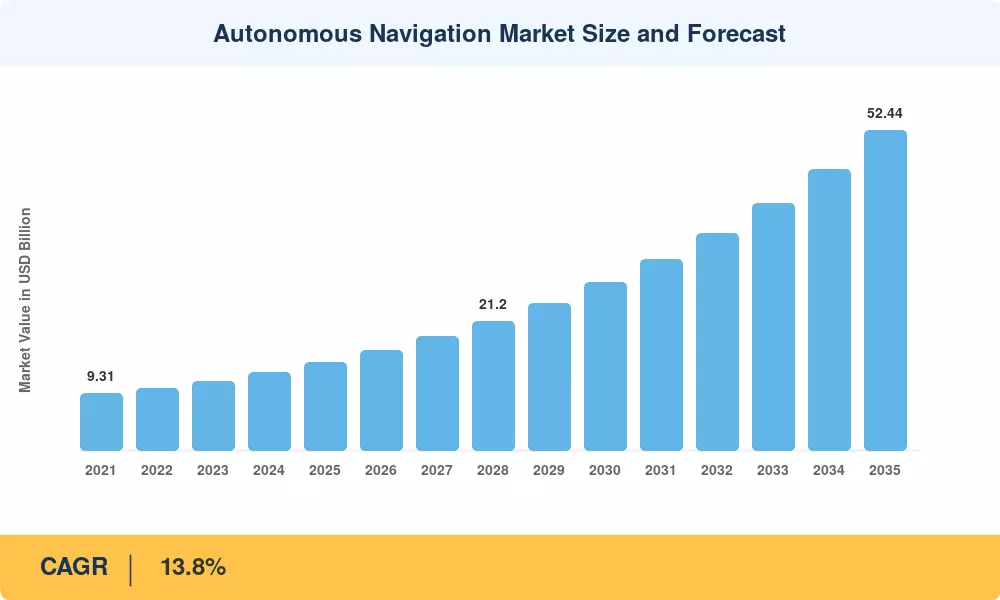

The Autonomous Navigation Market reached USD 14.38 billion in 2025 and is projected to grow from USD 16.37 billion in 2026 to USD 52.44 billion by 2035, registering a CAGR of 13.8% during the forecast period. Two catalysts anchor this trajectory: regulatory clearances for Level-3 conditional autonomy across the EU and select U.S. states, and a USD 4.2 billion wave of venture and defense capital channeled into navigation stack companies during 2024 alone [1]. These policy-and-capital tailwinds have pulled forward commercial timelines that once stretched into the next decade.

Legacy GPS-only positioning is giving way to multi-sensor fusion architectures that blend solid-state LiDAR, imaging radar, and inertial measurement units into unified stacks. Solid-state LiDAR unit costs dropped below USD 500 in 2024, a threshold that triggered OEM commitments for series production across passenger cars, commercial trucks, and warehouse robots [2]. That hardware deflation, paired with edge-AI inference chips capable of real-time simultaneous localization and mapping, has compressed the total cost of ownership for autonomous navigation platforms by roughly 30% compared with 2021 designs [3].

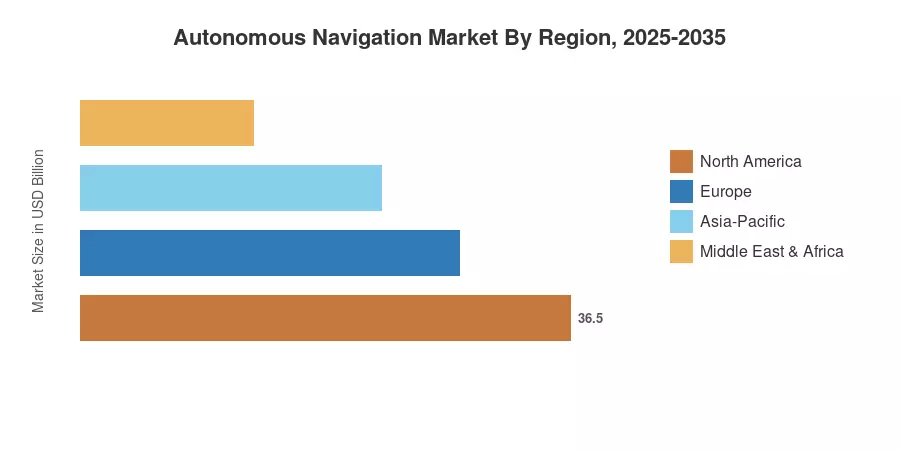

North America commands the largest share of the Autonomous Navigation Market at approximately 41.5%, driven by federal highway automation pilots and defense procurement cycles. The Middle East & Africa region is advancing at the fastest clip, with a projected 16.1% CAGR through 2035, fueled by smart-city mega-projects in Saudi Arabia and the UAE. Europe holds the second-largest position, supported by harmonized UNECE regulations that standardize autonomous driving approvals across member states. As sensor economics continue to improve and regulatory frameworks mature, the Autonomous Navigation Market is positioned for sustained double-digit expansion through the next decade.

Key Report Takeaways

• By Platform

- Automotive accounted for 49.4% of the Autonomous Navigation Market in 2024, underpinned by OEM investments in highway-pilot and valet-parking features.

- Industrial and logistics robots are expanding at the fastest platform CAGR of 16.3%, driven by warehouse automation demand across e-commerce fulfillment centers.

• By Component

- Hardware held a dominant 58.1% share of the Autonomous Navigation Market in 2024, reflecting the capital intensity of sensor suites and compute modules.

- Software is growing at a 15.5% CAGR as OEMs shift toward subscription-based feature activation and over-the-air update models.

• By Region

- North America led the Autonomous Navigation Market with a 41.5% revenue share in 2024, anchored by U.S. defense and commercial programs.

- The Middle East & Africa is the fastest-growing region at 16.1% CAGR, propelled by NEOM and Abu Dhabi autonomous transit initiatives.

Autonomous Navigation Market Size and Forecast (2021–2035)

Market Research Future employs a bottom-up revenue aggregation methodology, cross-referencing OEM shipment data, government procurement filings, and supply-chain invoicing with top-down macro indicators including GDP growth, R&D intensity ratios, and defense budget allocations. Historical figures (2021–2024) are validated against audited annual reports; forecast figures (2026–2035) incorporate scenario-weighted probability distributions.

.webp?v=1782993548)