Beer Market Summary

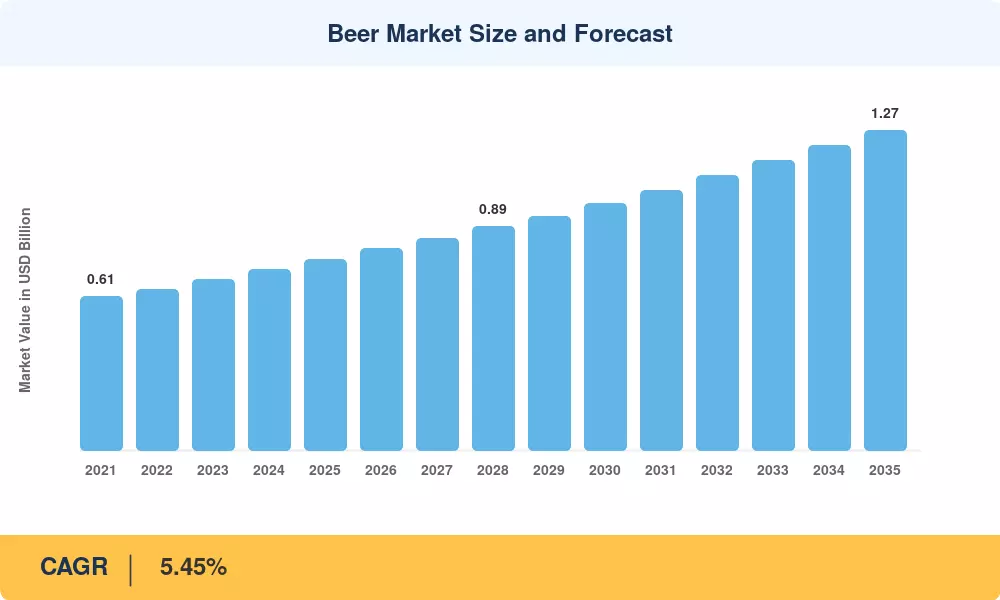

The global Beer Market reached USD 0.76 trillion in 2025 and is positioned to start the forecast at USD 0.80 trillion in 2026, climbing to USD 1.27 trillion by 2035 at a 5.45% CAGR. Two catalysts anchor this trajectory: roughly USD 14 billion in announced brewery capex between 2024 and 2027 across Asia-Pacific and Latin America, and the European Union's revised Packaging and Packaging Waste Regulation, which is reshaping beer packaging sustainability requirements for every major exporter [1][2]. The Beer Market sits at the intersection of cultural consumption habits and rapid portfolio reinvention.

Brewing operations are undergoing a quiet but decisive technology shift. Legacy gravity-fed brewhouses and manual quality lines are giving way to AI-assisted fermentation control, IoT-enabled cold-chain monitoring, and aluminum can lines that replace heavier glass bottling. Heineken alone has committed roughly USD 3.7 billion through 2030 to digitize breweries and decarbonize its packaging mix [3], signaling how operational modernization is now inseparable from category growth.

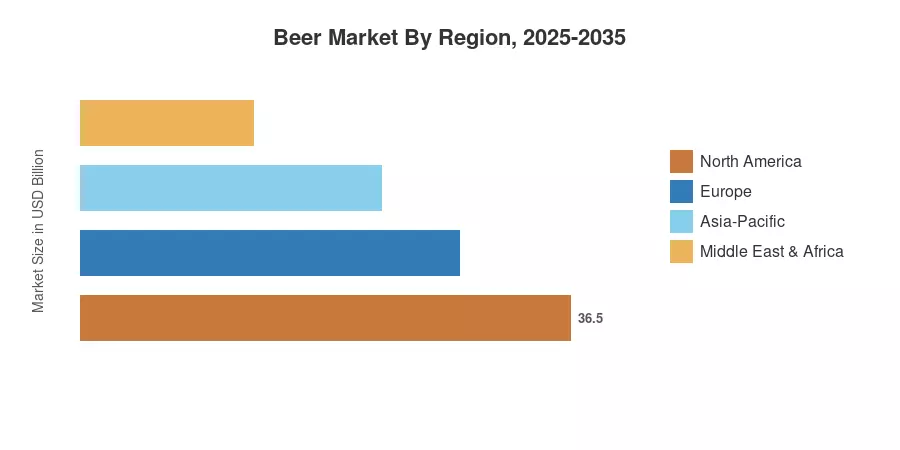

Asia-Pacific commands 32.8% of global revenue in 2025 and remains the fastest-growing region at a 5.77% CAGR, propelled by premiumization in China and Vietnam. Europe follows as the second-largest region, anchored by Germany, the UK, and a maturing low-alcohol beer innovation cluster. The decade ahead will reward brewers who combine cultural fluency with disciplined capital allocation.

Key Report Takeaways

• By Product Type

- Lager dominated the Beer Market in 2025 with an 81.4% volume share, supported by mainstream pricing and deep distribution

- Non/low-alcohol beer is poised for the fastest growth at a 5.62% CAGR through 2035, driven by Gen-Z moderation behavior

• By Category

- Premium beer is set to expand at a 5.78% CAGR, outpacing the standard segment in the Beer Market

- The standard segment retains dominance but is structurally ceding share.

• By Packaging

- Cans will record a 5.92% CAGR, the fastest packaging format, reflecting beer packaging sustainability priorities

• By Distribution

- Off-trade channels are projected to grow at a 5.39% CAGR, lifted by at-home consumption

- On-trade venues retain a revenue edge due to higher per-unit pricing

• By Region

- Asia-Pacific holds 32.8% of 2025 revenue in the Beer Market, while South America emerges as a secondary growth engine

Market Size and Forecast (2021–2035)

Market sizing combines brewery production volumes from national statistical agencies, customs trade flows, retail audits from Nielsen and IRI, and primary interviews with brewery procurement teams across 22 countries. Historical revenues are reconciled to USD using period-average exchange rates.