Bile Duct Cancer Market Summary

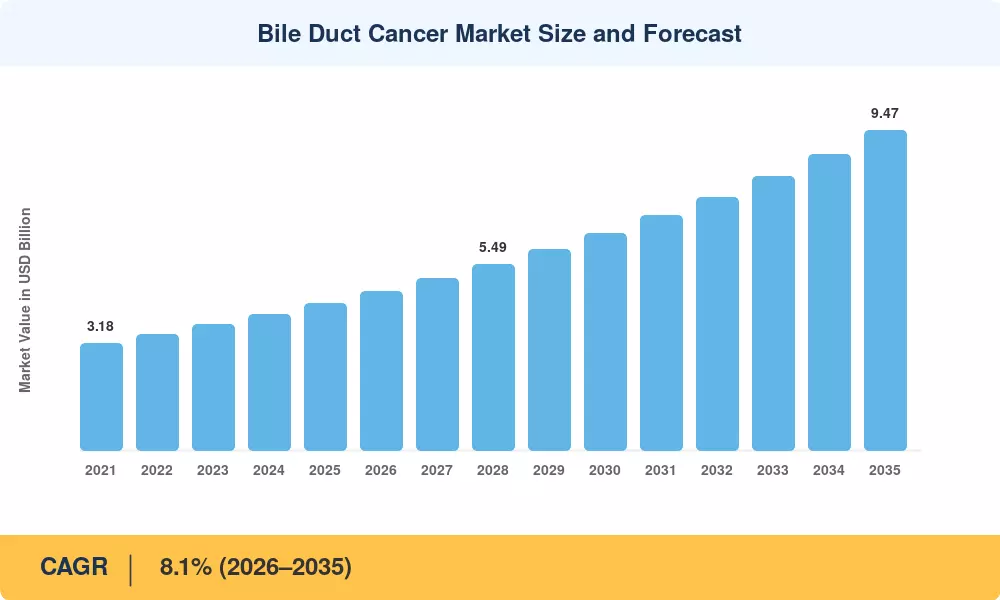

The Global Bile Duct Cancer Market size was valued at USD 4.35 Billion in 2025, and the market is projected to grow from USD 4.70 Billion in 2026 to USD 9.47 Billion by 2035, registering a CAGR of 8.1% during the forecast period 2026–2035. This expansion is underpinned by rising global incidence of cholangiocarcinoma treatment needs and sustained funding from national cancer institutes — the U.S. National Cancer Institute alone allocated over USD 6.8 billion to cancer research in fiscal year 2024, a meaningful share of which supports hepatobiliary studies [2]. Growing diagnostic precision and earlier-stage detection are channeling more patients into active biliary tract cancer therapy protocols, compressing the time between diagnosis and treatment initiation.

A decisive shift from conventional cytotoxic regimens toward molecularly targeted agents is redefining the Bile Duct Cancer Market. Legacy first-line chemotherapy combinations such as gemcitabine–cisplatin, long the backbone of hepatic duct cancer management, are being supplemented or replaced by FGFR inhibitors, IDH1 inhibitors, and immune checkpoint combinations. The FDA's accelerated approval of futibatinib and pemigatinib demonstrated regulatory willingness to fast-track bile duct tumor drugs with demonstrated objective response rates, catalyzing additional pharmaceutical investment exceeding USD 1.2 billion in biliary oncology pipeline assets between 2023 and 2025 [3].

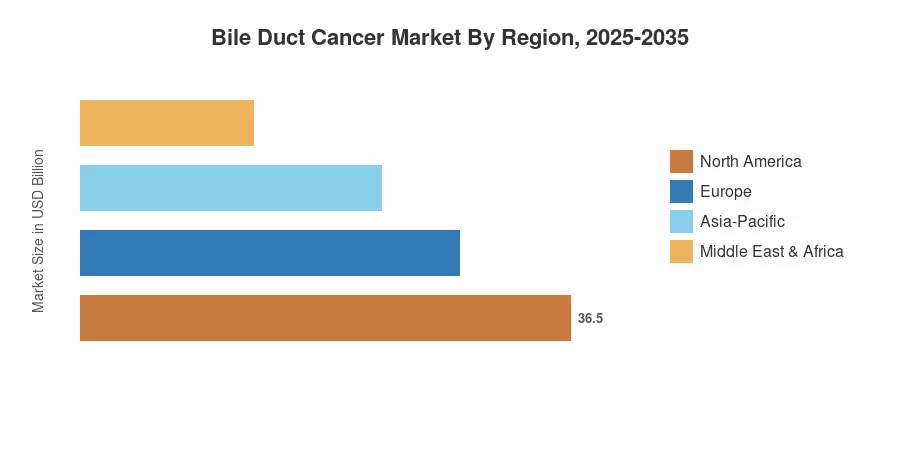

North America commands approximately 39% of the global Bile Duct Cancer Market revenue, supported by advanced referral networks and payer coverage for targeted therapies. Asia-Pacific is the fastest-growing region with a projected CAGR above 9.5%, driven by rising cholangiocarcinoma incidence in Southeast Asia and expanding access to ERCP bile duct oncology services. Europe holds the second-largest share at roughly 27%, anchored by Germany, France, and the UK's comprehensive cancer strategies. As precision diagnostics become more accessible across emerging economies, the Bile Duct Cancer Market is poised for sustained double-digit regional growth through 2035.

Key Report Takeaways

• By Type

- Intrahepatic bile duct cancer (iCCA) accounts for roughly 58% of total Bile Duct Cancer Market revenue, propelled by increasing diagnostic identification and the availability of targeted bile duct tumor drugs

- Extrahepatic bile duct cancer (eCCA) is projected to grow at a CAGR of 7.4% through 2035, as improvements in ERCP bile duct oncology and surgical resection techniques expand the addressable patient pool

• By Treatment Type

- Targeted therapy holds the fastest segment growth rate at 10.2% CAGR, reflecting accelerating adoption of FGFR and IDH inhibitors within the Bile Duct Cancer Market

- Chemotherapy remains the largest treatment segment by value, generating approximately USD 1.48 billion in 2025, though its share is gradually declining as cholangiocarcinoma treatment paradigms evolve

• By Region

- North America's dominance in the Bile Duct Cancer Market is reinforced by robust clinical trial infrastructure and insurance reimbursement for biliary tract cancer therapy

- Asia-Pacific's growth trajectory is fueled by high endemic incidence rates and government investments in hepatic duct cancer management capacity

Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model triangulates bottom-up revenue estimates from pharmaceutical sales, procedure volumes, and payer reimbursement data with top-down macroeconomic benchmarks. Historical figures draw on audited company filings, national cancer registry data, and WHO epidemiological reports. Forecast values apply the calibrated 8.1% CAGR derived from pipeline maturity modeling and addressable patient population projections.

.webp?v=1782976095)