Bionic Eye Market Summary

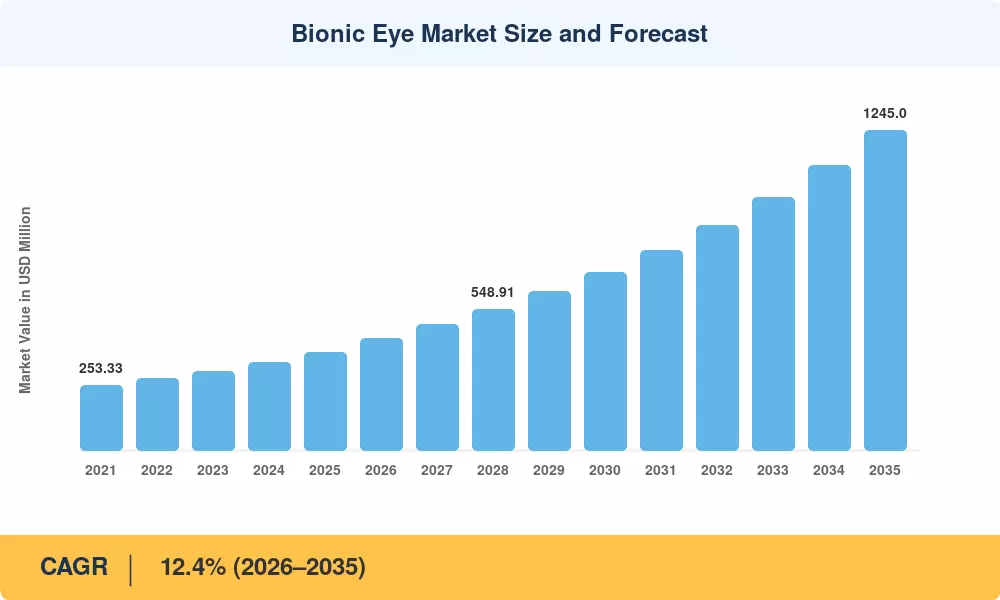

The Global Bionic Eye Market size was valued at USD 382.80 Million in 2025, and the market is projected to grow from USD 434.48 Million in 2026 to USD 1,245.00 Million by 2035, registering a CAGR of 12.4% during the forecast period 2026–2035. This expansion rests on an aging global population — the WHO estimates 2.2 billion people live with some form of vision impairment — combined with accelerated regulatory pathways such as the FDA's Breakthrough Device Designation program, which has shortened approval timelines for visual prosthetics by roughly 30% since 2020 [1]. Public funding bodies in the US, EU, and Australia have collectively channeled over USD 600 Million into neural-interface vision research since 2018 [2], creating a pipeline of devices approaching clinical viability.

The Bionic Eye Market is currently experiencing a fundamental technological transformation. Legacy external-camera configurations that are connected to wired processors are being replaced by entirely implantable systems that are powered by wireless telemetry. The active surface area of micro-electronic arrays has decreased to less than 1 mm², and the number of electrodes has increased to over 100 channels. This has resulted in a shift in resolution from rudimentary phosphene perception to functional shape recognition [3]. The cortical pathway has been validated as a viable alternative to retinal approaches, as evidenced by the combined grant funding of cortical implant initiatives at Monash University, Baylor College of Medicine, and several European consortia, which exceeds USD 150 million [4].

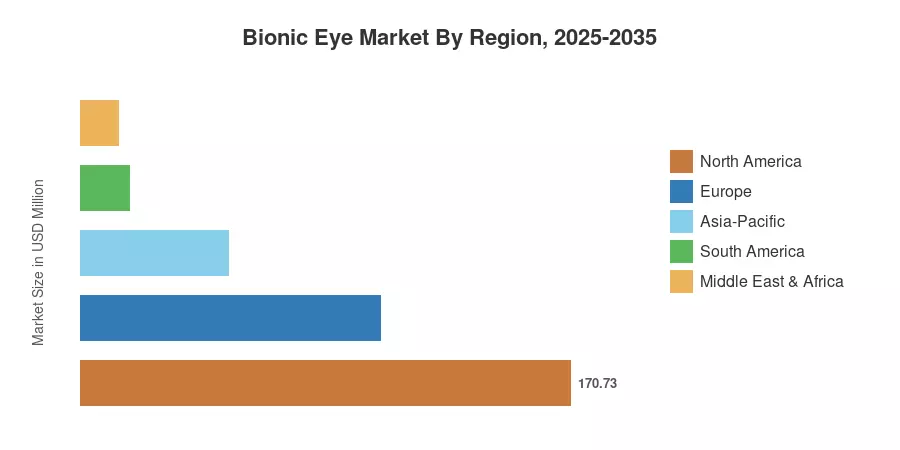

North America is responsible for approximately 44.6% of the Bionic Eye Market, which is primarily driven by a concentration of clinical trial sites and robust Medicare reimbursement codes (CPT 0100T–0101T). The Asia-Pacific region is expected to experience the highest rate of growth, with a compound annual growth rate (CAGR) of 13.5%. This growth is being driven by the increasing capacity of ophthalmic surgical procedures in China, India, and South Korea. Europe's second-largest position is anchored by Horizon Europe neurotechnology grants and NHS pilot programs, with an approximate 27.3% share. The Bionic Eye Market is poised to evolve from a niche surgical intervention to a scalable clinical platform in the coming decade as device miniaturization continues and cost profiles improve.

Key Report Takeaways

• By Technology

- Retinal prosthesis held approximately 54.2% of the Bionic Eye Market share in 2025, reflecting its longer clinical track record and established surgical protocols.

- Cortical visual prosthesis is expanding at a 13.2% CAGR through 2035 as multi-center trials validate superior resolution potential for patients ineligible for retinal devices.

• By Device Placement

- External wearable systems led the Bionic Eye Market with about 69.4% share in 2025, owing to lower surgical complexity.

• By Component

- Power and telemetry modules are growing at a 13.3% CAGR, driven by wireless charging breakthroughs that eliminate percutaneous connectors.

• By End-User

- Hospitals and eye-care chains captured roughly 48.9% of revenue in the Bionic Eye Market in 2025, serving as the primary implantation setting.

• By Region

- Asia-Pacific is set to expand at the highest regional CAGR of 13.5% during 2026–2035, led by government-subsidized ophthalmic programs in China and India.

Market Size and Forecast (2021–2035)

Market Research Future employs a bottom-up revenue methodology for the Bionic Eye Market, triangulating device shipment volumes, average selling prices across retinal, cortical, and optic-nerve platforms, and procedure reimbursement data from 40+ national health systems. Historical figures (2021–2024) draw on company filings and MedTech regulatory clearance databases, while the forecast (2026–2035) applies scenario-weighted CAGR modeling anchored to clinical-trial pipeline maturity curves.