Biopsy Devices Market Summary

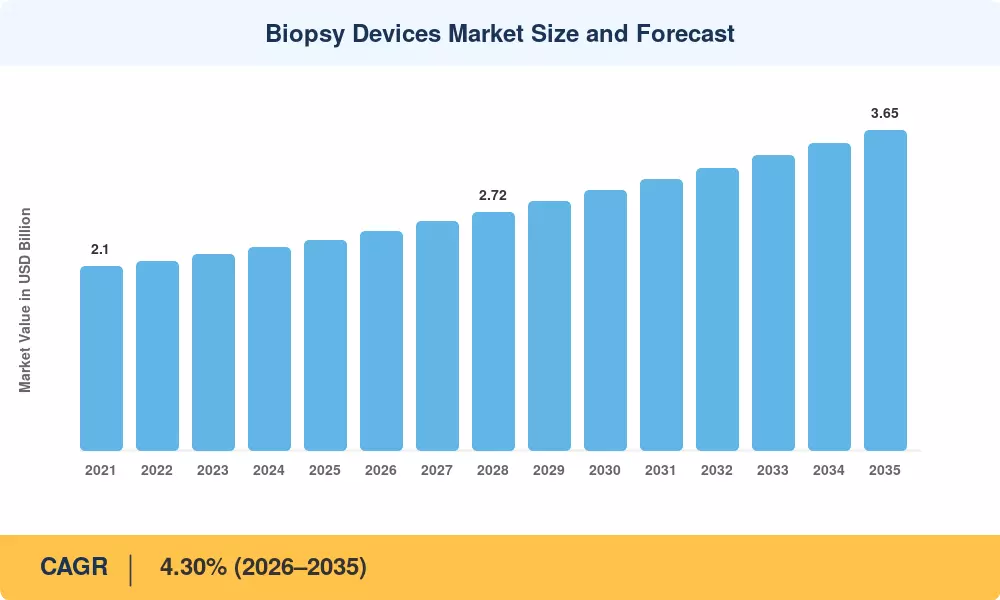

The Global Biopsy Devices Market size was valued at USD 2.40 Billion in 2025, and the market is projected to grow from USD 2.50 Billion in 2026 to USD 3.65 Billion by 2035, registering a CAGR of 4.30% during the forecast period 2026–2035. This trajectory is anchored in government-funded screening mandates — Australia's bulk-billed low-dose CT lung screening program, the EU's Beating Cancer Plan allocating EUR 4 billion across member states, and the U.S. National Cancer Institute's expanded early-detection portfolio — all of which funnel more patients toward tissue confirmation procedures [1][2].

A technology inflection point is reshaping how biopsies are performed. Legacy freehand needle techniques are giving way to integrated platforms that pair vacuum-assisted aspiration with AI-powered image guidance, cutting procedural time by an estimated 30–40% while improving specimen adequacy rates above 95% [3]. Medtronic's 2024 launch of its AI-fused stereotactic platform and Hologic's acquisition of an automated specimen-verification startup underscore where capital is flowing [4]. Regulatory bodies in the U.S. and EU have also streamlined 510(k) and CE-MDR pathways for single-use biopsy instruments, further lowering barriers to device innovation.

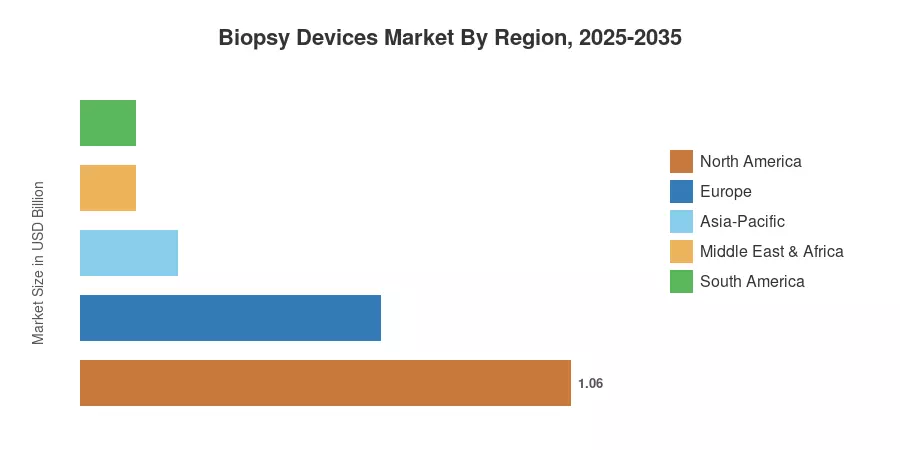

North America commands the largest share of the Biopsy Devices Market at approximately 44% of 2025 revenue, driven by high screening penetration and insurer-mandated biopsy protocols. Asia-Pacific is the fastest-growing region with a projected CAGR of 8.90%, fueled by China's expanding county-level cancer screening infrastructure and India's Ayushman Bharat hospital investment cycle [5]. Europe represents the second-largest region at roughly a 27% share, anchored by the UK's National Health Service breast-screening overhaul and Germany's DRG reimbursement expansion for outpatient biopsy procedures. As diagnostic workflows become increasingly decentralized, the Biopsy Devices Market is positioned for sustained multi-year expansion.

Key Report Takeaways

• By Product Type

- Needle-based biopsy instruments captured 47.5% of the Biopsy Devices Market revenue share in 2025, led by demand for spring-loaded core systems in breast and liver applications.

- Procedure trays are forecast to register a 5.20% CAGR through 2035, reflecting the hospital preference for pre-packaged sterile kits that reduce setup variability.

• By Application

- Breast biopsy procedures held a 33.4% share of the Biopsy Devices Market in 2025, supported by organized mammography-screening recall pathways across OECD nations.

- Lung biopsy is projected to grow at a 9.70% CAGR through 2035 as low-dose CT screening expands eligibility criteria in North America and Oceania.

• By End User

- Hospitals accounted for 63.4% of 2025 end-user spending, reflecting their role as the primary venue for complex image-guided procedures.

- Ambulatory surgical centers represent the fastest-growing channel, posting a projected 9.90% CAGR as payors incentivize outpatient migration.

• By Region

- North America generated approximately 44.1% of Biopsy Devices Market revenue in 2025.

- Asia-Pacific is forecast to achieve the highest regional CAGR at 8.90% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework integrates bottom-up hospital procedure volumes, average selling prices by device category, distributor sell-through data, and national cancer registry incidence rates. Historical data (2021–2024) is triangulated against U.S. FDA 510(k) clearance databases, EU MDR registrations, and company-reported medical-device segment revenues. Forecast projections (2026–2035) apply an econometric model anchored to screening policy adoption curves, demographic aging indices, and technology replacement cycles.