Biosensors Market Summary

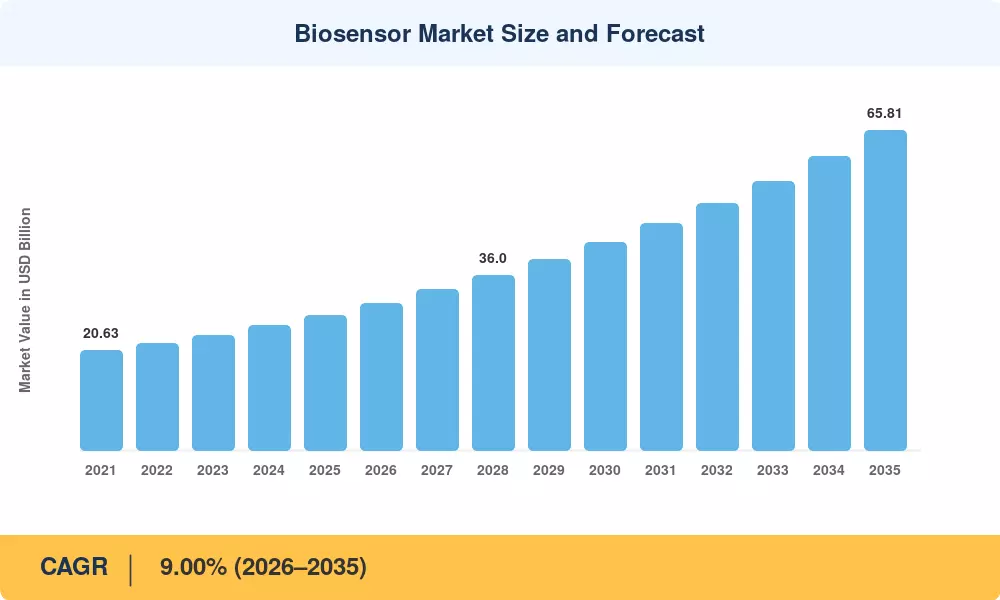

The Biosensor Market reached a valuation of USD 27.80 billion in 2025 and is projected to grow from USD 30.30 billion in 2026 to USD 65.81 billion by 2035, registering a compound annual growth rate of 9.00% across the forecast window. This expansion trajectory sits at the intersection of two powerful catalysts: the global surge in chronic disease prevalence — the WHO estimates 1.27 billion people will live with diabetes by 2050 [1] — and aggressive government programs that position rapid diagnostics as front-line public health infrastructure. The U.S. BARDA alone committed over USD 1.1 billion between 2023 and 2025 to accelerate next-generation diagnostic platforms [2].

The biosensor market is being revolutionized from the inside out, driven by a fundamental technical shift. Miniaturized AI-powered sensing devices that can detect several analytes in less than five minutes are replacing traditional immunoassay operations in the lab. Continuous surveillance systems first developed for glucose management have since been adapted to lactate, cortisol, and cardiac troponin [3], with more than USD 4.8 billion in venture and strategic investment since 2022. Regulatory authorities in the EU and Japan have established accelerated review paths for software-as-a-medical-device biosensors, reducing standard approval durations by 30–40% [4].

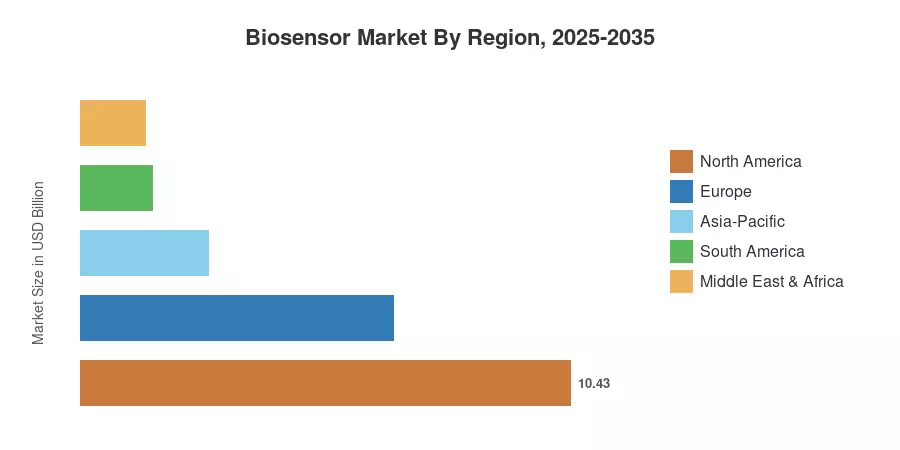

North America holds the lion's share in the Biosensor Market, with a 37.5% stake, supported by robust reimbursement policies and a mature digital health ecosystem. Asia-Pacific is the fastest-growing market, with a predicted CAGR of 9.80% till 2035, driven by the deployment of India’s Ayushman Bharat and China’s 14th Five-Year Plan for biomedical instruments. Europe accounted for 24.0% of the market, underpinned by the EU In Vitro Diagnostic Regulation that redefined compliance requirements in 2022. Sensing hardware is converging with cloud analytics and consumer wearables, and the Biosensor Market is entering a phase of structural acceleration that will alter care delivery across clinical and consumer settings.

Key Report Takeaways

• By Product Type

- Medical biosensors accounted for 69.0% of the Biosensor Market in 2025, reflecting sustained demand from diabetes management and cardiac care segments.

- Wearable and embedded biosensor configurations are forecast to register a 10.70% CAGR between 2026 and 2035, outpacing traditional benchtop formats.

• By Technology

- Electrochemical platforms generated USD 17.81 billion in 2025, maintaining their position as the dominant sensing architecture in the Biosensor Market.

- Optical biosensor technologies are projected to expand at a 10.90% CAGR through 2035, driven by fluorescence and surface plasmon resonance innovations.

• By End User

- Point-of-care testing captured 61.0% of end-user demand in 2025, reflecting the decentralization of diagnostics from hospital laboratories.

- Home healthcare diagnostics is the fastest-growing end-user channel in the Biosensor Market, anticipated to achieve an 11.50% CAGR over the study period.

• By Geography

- North America led the Biosensor Market with a 37.5% revenue share in 2025.

- Asia-Pacific is projected to record a 9.80% CAGR to 2035, the fastest of any region.

Biosensor Market Size and Forecast (2021–2035)

Market sizing is based on primary interviews with device OEMs, component suppliers and hospital procurement teams, in addition to secondary research of regulatory filings, trade association databases and published financial disclosures. Historical numbers (2021–2024) are validated using customs trade data and business revenue breakdowns. Forecast forecasts are made using a bottom-up demand model calibrated to disease prevalence curves, reimbursement expansion timelines and technology adoption S-curves.