Bird Repellent Market Summary

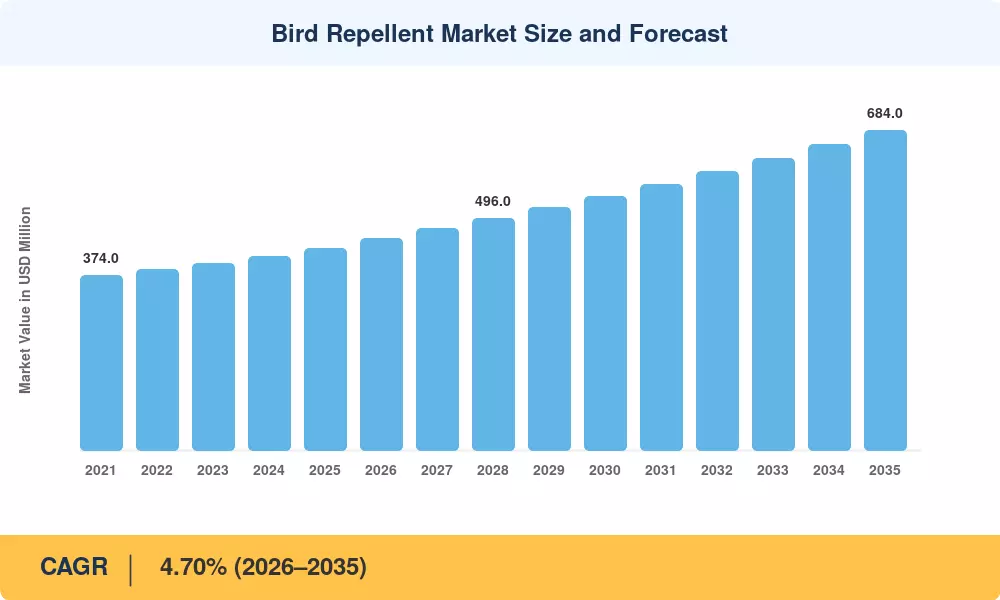

The bird repellent market stood at USD 432.10 million in 2025 and is projected to grow from USD 452.40 million in 2026 to USD 684.00 million by 2035, registering a CAGR of 4.70% during the forecast period (2026–2035). Tightening food-safety mandates from the U.S. FDA and European EFSA, combined with rising avian-borne disease alerts such as the H5N1 resurgence tracked by the WHO, have pushed both growers and property managers toward structured bird management programs [1][2].

Basic reflecting tape, static decoys and rudimentary noise emitters are slowly making way to sensor-equipped autonomous systems combining radar detection with laser deterrent and AI-driven behavioral analytics – legacy passive technologies. The USDA’s Wildlife Services program budgeted more than USD 30 million in fiscal 2024 to address avian crop damage in fruit and grain belts, driving the need for scalable repellant technology at the federal level [3]. This is shortening replacement cycles and increasing average order values across the bird repellent sector.

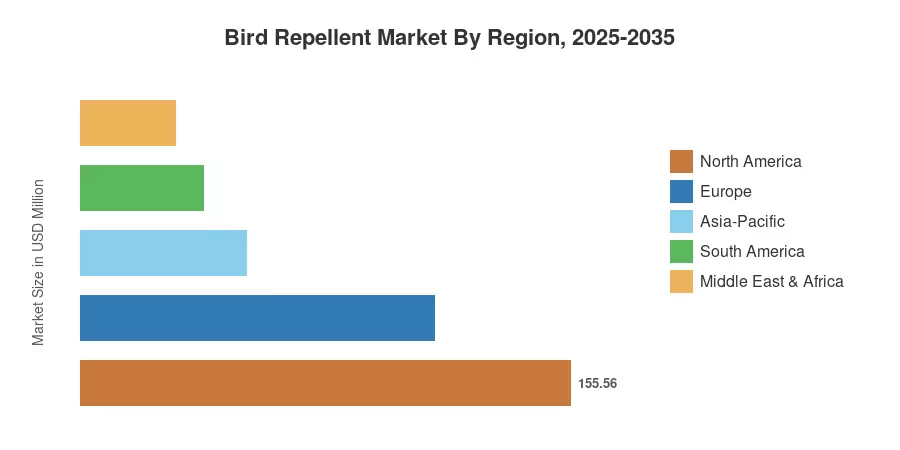

North America accounts for around 36.0% of the world’s revenues, driven by large-scale broadacre farming and stringent urban pest-management regulations. Asia Pacific is the fastest expanding market with a CAGR of 12.2%, led by India’s horticulture subsidies and China’s post-harvest loss reduction efforts. Europe takes second place with 26.0% share, where the law on biodiversity directs procurement to non-lethal products with ecological certification. These regional trends will influence the competitive landscape of the bird repellent market till 2035.

Key Report Takeaways

• By Product Type

- Chemical bird repellents accounted for approximately 58.0% of the bird repellent market in 2024, sustained by proven efficacy in large-scale agricultural applications.

- Natural and organic bird repellents are forecast to expand at a 16.3% CAGR through 2035, reflecting tightening pesticide-residue regulations across the EU and North America.

• By Form

- Sprays captured roughly 40.0% of the bird repellent market in 2024, preferred for ease of application across orchards and vineyards.

- Gels and pastes are poised to grow at a 14.8% CAGR to 2035, gaining traction in rooftop and structural installations.

• By End-Use

- Agriculture held a 56.0% share of the bird repellent market in 2024, led by row-crop and orchard segments in North America and Asia-Pacific.

- Non-agriculture end-uses are projected to advance at a 12.4% CAGR through 2035, powered by aviation safety mandates and commercial property management.

• By Geography

- North America commanded 36.0% of the bird repellent market in 2024, supported by USDA-funded wildlife-damage programs and municipal pest-control codes.

- Asia-Pacific is set to accelerate at a 12.2% CAGR to 2035, fueled by rapid urbanization and expanding protected-agriculture acreage.

Bird Repellent Market Size and Forecast (2021–2035)

MRFR’s size model utilizes primary survey data from over 120 distributors, government crop-loss databases (USDA NASS, FAO), trade-shipment data, and firm filings. Reported sales are the basis for the historical data; the future figures are based on the calibrated 4.70% CAGR with modifications for regulatory inflections and technology-adoption curves.

.webp?v=1783938003)