Black Start Generator Market Summary

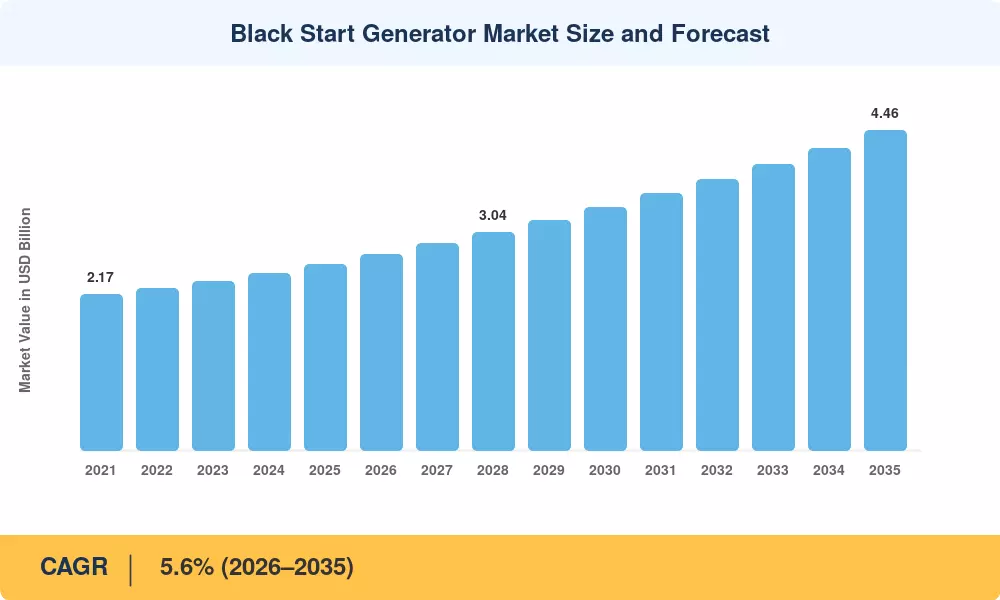

The black start generator market was valued at USD 2.59 billion in 2025 and is projected to reach USD 2.73 billion in 2026, climbing to USD 4.46 billion by 2035 at a CAGR of 5.6% during the forecast period. Tightening reliability mandates from NERC and FERC continue to compel transmission operators to maintain or upgrade their restart fleets, while the U.S. Department of Energy's Grid Resilience Innovation Partnership (GRIP) program — allocating over USD 10.5 billion through 2026 — is channeling fresh capital into restoration infrastructure [1][2].

A technology shift is underway within the black start generator market as legacy open-cycle diesel units give way to digitally controlled, hybrid battery-diesel platforms. Silicon-carbide power electronics and advanced alternator designs are reducing both start-up latency and emissions footprints. The European Commission's revised Trans-European Networks for Energy (TEN-E) regulation now explicitly includes black start assets in its cross-border infrastructure eligibility criteria, unlocking co-financing for operators modernizing aging gensets [3][4].

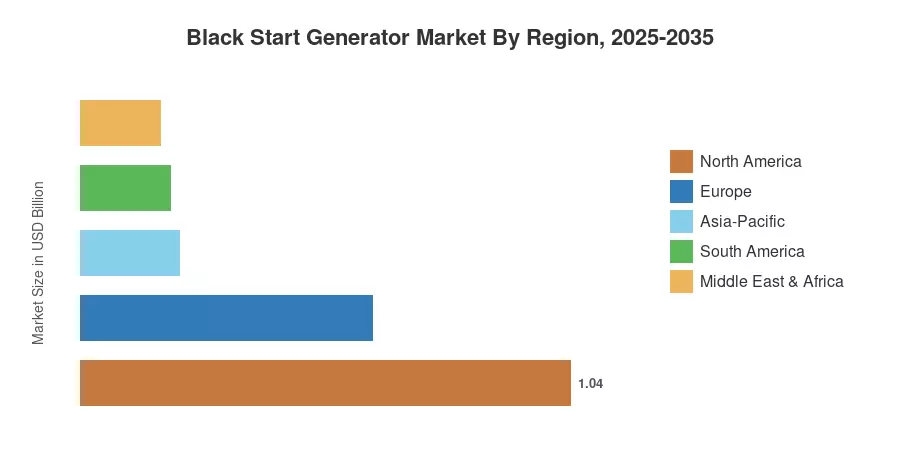

North America commanded roughly 40.0% of the black start generator market in 2025, anchored by mandatory NERC Standard EOP-005. Asia-Pacific is the fastest-growing region, expanding at approximately 8.0% CAGR as China's State Grid Corporation and India's Power Grid Corporation invest heavily in grid restoration capacity. Europe holds the second-largest position, driven by ENTSO-E harmonization of restoration codes across 35 transmission system operators. By 2035, the interplay of decarbonization targets and grid-stability regulations will keep this market on a sustained upward trajectory [5][6].

Key Report Takeaways

• By Fuel Type

- Diesel accounted for approximately 57.0% of the black start generator market in 2025, reflecting its logistical simplicity and proven cold-start reliability across diverse climates.

- Hybrid battery-diesel systems are the fastest-growing fuel segment, projected at a 9.7% CAGR through 2035.

• By Power Rating

- Units rated up to 1 MW captured roughly 49.6% share of the black start generator market in 2025.

- The 1–5 MW class is expected to grow at an 8.7% CAGR, driven by utility-scale restoration needs.

• By End-User

- Utilities and transmission operators held approximately 50.4% of the black start generator market in 2025.

- Data centers are advancing at a 9.2% CAGR, fueled by hyperscale expansion and uptime SLAs.

• By Region

- North America led with a 40.0% share of the black start generator market.

- Asia-Pacific is the fastest-growing region at approximately 8.0% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down revenue analysis with bottom-up OEM shipment data and is validated through expert interviews across 14 countries. Historical figures (2021–2024) reflect audited industry revenues; the 2025 base year is calibrated from preliminary shipment data; and the 2026–2035 forecast applies a compound annual growth framework adjusted for cyclical capital-expenditure patterns in the power sector.