Blue Hydrogen Market Summary

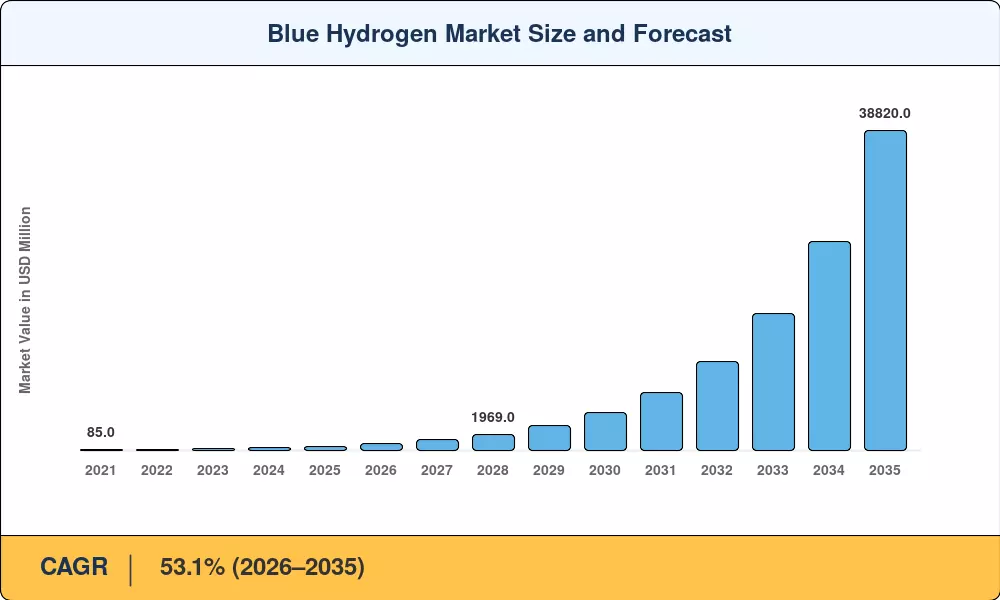

The Blue Hydrogen Market reached an estimated USD 540 Million in 2025, positioning it as one of the fastest-scaling energy transition verticals globally. Starting from a forecast base of USD 840 Million in 2026, the blue hydrogen market is projected to surge to USD 38,820 Million by 2035, registering a CAGR of 53.1% across the forecast period. Two policy catalysts anchor that trajectory: the United States' Inflation Reduction Act Section 45V production tax credit, which offers up to USD 3/kg for low-carbon hydrogen, and the European Union's Renewable Fuels of Non-Biological Origin (RFNBO) mandate that pulls blue hydrogen into industrial decarbonization targets [1][2].

A generational shift in reforming technology is reshaping the blue hydrogen market's supply side. Legacy steam methane reforming units—many dating from the 1990s and capturing less than 60% of CO₂—are giving way to next-generation autothermal reforming plants equipped with carbon capture units that achieve 95%+ capture rates. The U.S. Department of Energy's Regional Clean Hydrogen Hubs program has directed USD 7 billion across seven hubs, with at least three featuring blue hydrogen as a primary production pathway [3]. Shared carbon capture infrastructure in the North Sea, the U.S. Gulf Coast, and Alberta is lowering project CAPEX by an estimated 25–35% [4].

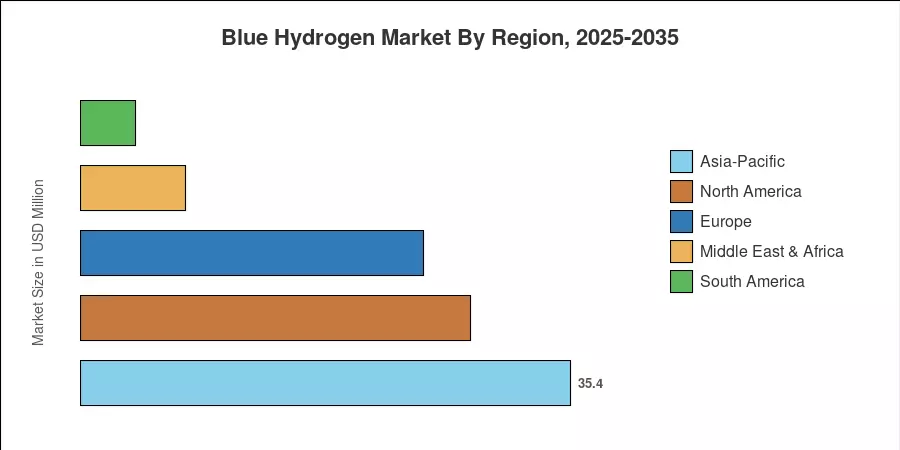

Asia-Pacific dominates the blue hydrogen market with approximately 35.4% of global revenue in 2025, driven by blue-ammonia back-haul corridors linking Saudi Arabia and Australia to Japan and South Korea. The region also posts the highest CAGR through 2035. North America follows at 28.2% share, buoyed by 45V economics and Gulf Coast sequestration capacity. Europe holds a 24.8% share, with the North Sea CO₂ storage cluster underpinning projects in the UK, Norway, and the Netherlands. The decade ahead will test whether policy certainty can keep pace with capital commitments now exceeding USD 50 billion in announced project pipelines worldwide [5].

Key Report Takeaways

• By Technology

- Steam Methane Reforming + CCS commanded roughly 57% of the blue hydrogen market in 2025, reflecting the installed base advantage of conventional reformers retrofitted with capture equipment.

- Autothermal Reforming + CCS is the fastest-growing technology segment in the blue hydrogen market, driven by superior capture efficiency and subsidy eligibility.

• By End-User Industry

- The refining sector led the blue hydrogen market by end-user share in 2025, accounting for approximately 36% of demand as refiners blended blue hydrogen into existing grey hydrogen supply chains.

- Transportation is projected to post the highest growth rate among end-user verticals, spurred by heavy-duty trucking and maritime bunkering pilots transitioning to commercial scale.

• By Region

- Asia-Pacific held the largest share of the blue hydrogen market in 2025, underpinned by Japan and South Korea's national hydrogen strategies and long-term offtake contracts.

- North America ranks second, with the U.S. Gulf Coast emerging as a global blue hydrogen export hub.

Blue Hydrogen Market Size and Forecast (2021–2035)

Market Research Future's sizing framework triangulates bottom-up plant-level capacity data against top-down policy spending, trade flow volumes, and engineering-procurement-construction contract values to derive annual estimates. Historical data covers 2021–2024 actuals; 2025 is the base year calibrated from operator disclosures and government registry filings. Forecast years 2026–2035 apply scenario-weighted growth factors anchored to announced project FIDs and subsidy phase-in schedules.

.webp?v=1784802862)