Brain Health Supplements Market Summary

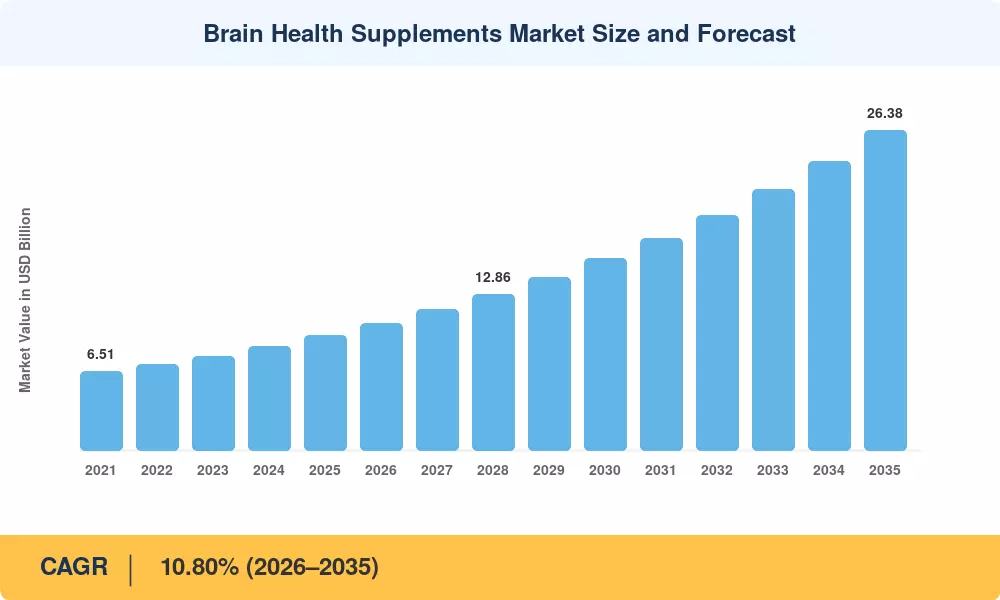

The Global Brain Health Supplements Market size was valued at USD 9.46 Billion in 2025, and the market is projected to grow from USD 10.48 Billion in 2026 to USD 26.38 Billion by 2035, registering a CAGR of 10.80% during the forecast period 2026–2035. Two catalysts are accelerating demand faster than historical trend lines: the Alzheimer's Association reported roughly 6.9 million Americans aged 65-plus living with Alzheimer's disease in 2024 [1], and national health agencies across the EU committed over EUR 1.2 billion to dementia-prevention research programs through 2030 [2]. These policy-driven investments have turned a once-niche wellness category into a mainstream healthcare priority.

Product innovation is reshaping the Brain Health Supplements Market at the formulation level. Conventional single-ingredient capsules are giving way to clinically dosed, multi-stack blends that pair botanical actives with bioavailability enhancers such as liposomal delivery systems and cyclodextrin complexation. The U.S. National Institutes of Health allocated USD 3.7 billion to neuroscience research in fiscal year 2024 [3], spurring a pipeline of ingredient-efficacy studies that manufacturers now cite on product labels.

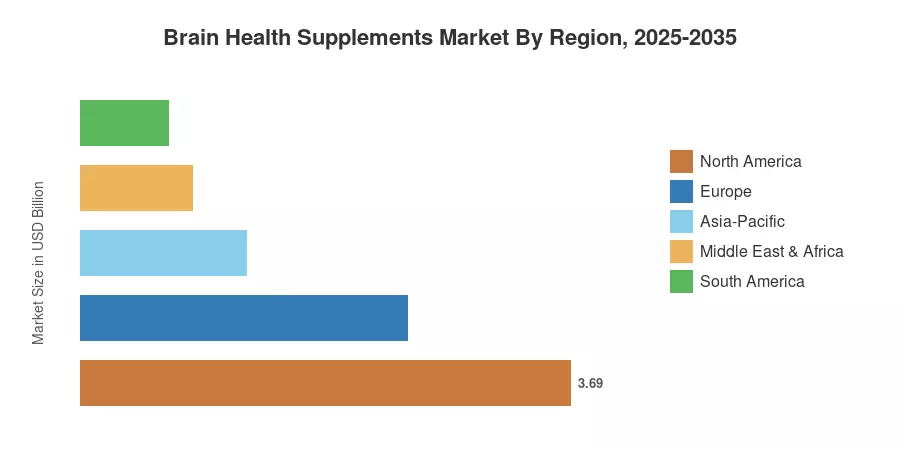

North America commands approximately 39% of global revenue, anchored by high per-capita supplement spending and direct-to-consumer digital channels. Asia-Pacific is the fastest-growing region, with a projected CAGR exceeding 13.2%, driven by rapidly aging populations in Japan, South Korea, and China. Europe holds the second-largest share at roughly 26%, supported by tightening EU health-claim regulations that favor established, science-backed brands. As clinical evidence deepens and regulatory frameworks mature, the Brain Health Supplements Market is positioned for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Product Type

- Vitamins & Minerals accounted for the largest revenue share in 2025, driven by widespread consumer familiarity with B-vitamins, vitamin D, and magnesium formulations for cognitive upkeep.

- Natural Molecules are projected to register a CAGR of 12.6% through 2035 as clinical trials validate compounds like citicoline and alpha-GPC for neuroprotection.

- Herbal Extracts generated approximately USD 2.46 billion in 2025, reflecting strong demand for bacopa monnieri and ginkgo biloba across Asian and European markets.

• By Application

- Memory Enhancement held the dominant position in the Brain Health Supplements Market, capturing roughly 28% of global demand.

- Stress & Anxiety applications are expanding at a CAGR of 13.1%, propelled by post-pandemic workplace wellness programs.

- Sleep & Recovery supplements reached USD 1.32 billion in 2025, with melatonin-plus-L-theanine stacks gaining traction among shift workers.

• By Region

- North America led the Brain Health Supplements Market with USD 3.69 billion in 2025, supported by robust e-commerce infrastructure.

- Asia-Pacific is forecast to grow at 13.2% CAGR, outpacing all other regions through 2035.

- Europe captured approximately 26% of total revenue, with Germany and the UK as primary demand centers.

Market Size and Forecast (2021–2035)

Market Research Future estimates are derived from a combination of bottom-up revenue modeling across product types, applications, and distribution channels, validated through primary interviews with manufacturers, distributors, and regulatory bodies. Historical figures (2021–2024) reflect reported and estimated actuals; forecast figures (2026–2035) apply a calibrated compound growth model.