Bronchoscopes Market Summary

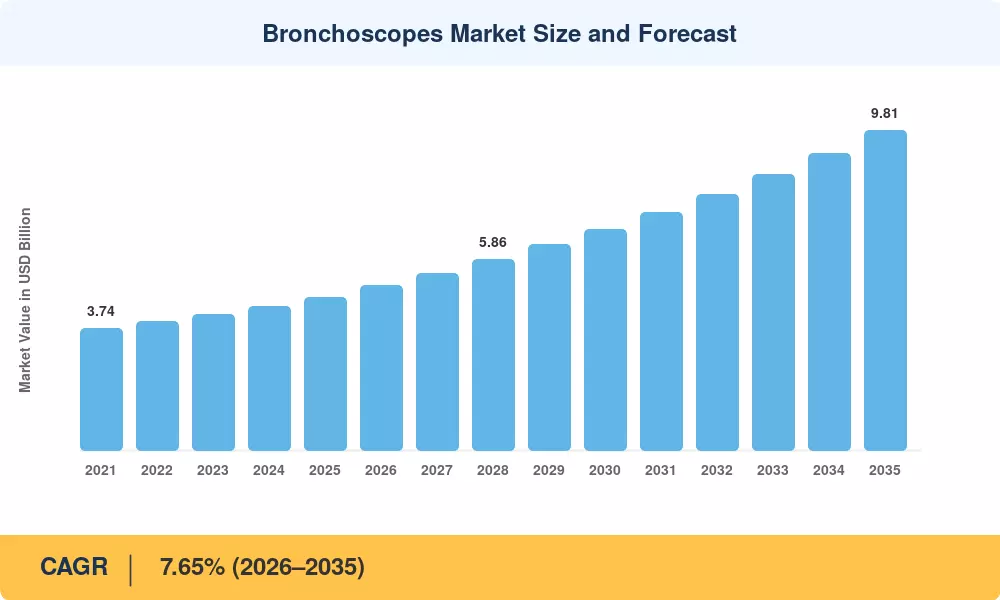

The Bronchoscopes Market size was valued at USD 4.69 Billion in 2025, and the market is projected to grow from USD 5.05 Billion in 2026 to USD 9.81 Billion by 2035, registering a CAGR of 7.65% during the forecast period 2026–2035. Two structural catalysts anchor this trajectory: the Centers for Medicare & Medicaid Services' HCPCS C1601 pass-through payment, which has lowered the economic barrier for hospitals adopting disposable scopes [1], and the persistent global rise in lung-cancer screening programs that continue to push procedure volumes higher year after year [2].

Technology shifts are reshaping the Bronchoscopes Market from the inside out. Legacy fiberoptic systems are giving way to high-definition digital platforms, and robotic-assisted navigation is compressing physician learning curves while improving diagnostic yield in peripheral lung lesions. The U.S. Preventive Services Task Force's expanded screening eligibility criteria have channeled an estimated USD 1.2 billion in incremental diagnostic spending toward bronchoscopy suites since 2022 [3]. Single-use devices, once a niche infection-control alternative, now represent the fastest-growing usage category as hospitals weigh reprocessing costs against cross-contamination risks flagged by the FDA [4].

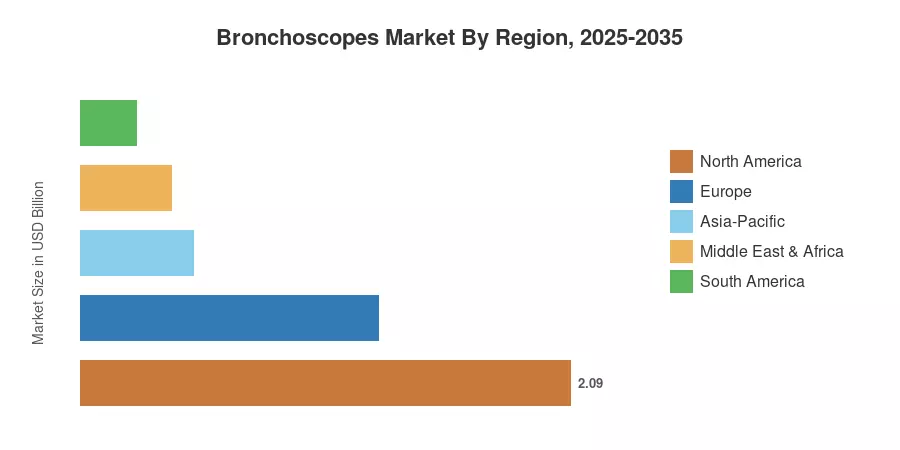

North America commanded roughly 44.5% of the Bronchoscopes Market in 2025, anchored by high procedural reimbursement rates and rapid robotic-platform adoption. Asia-Pacific stands out as the fastest-growing region at a forecast CAGR of 10.2%, driven by national screening mandates in China, Japan, and South Korea. Europe held the second-largest share at approximately 27%, supported by EU Medical Device Regulation compliance investments. As payers continue site-of-care shifts toward ambulatory settings, the Bronchoscopes Market is poised to evolve well beyond its traditional hospital-centric demand base.

Key Report Takeaways

• By Product Type

- Flexible bronchoscopes accounted for roughly 66.5% of the Bronchoscopes Market share in 2025, reflecting clinician preference for navigational versatility in complex airways.

- Rigid bronchoscopes recorded a CAGR of 5.3% through 2035, sustained by interventional pulmonology procedures requiring stent placement and foreign-body retrieval.

- Accessories generated approximately USD 0.89 Billion in 2025 revenue, driven by replacement cycles for biopsy forceps, brushes, and cleaning adapters.

• By Usage

- Reusable devices held a 69.6% share of the Bronchoscopes Market in 2025, though single-use scopes are expanding at a 17.0% CAGR through 2035.

• By Application

- Reusable devices held a 69.6% share of the Bronchoscopes Market in 2025, though single-use scopes are expanding at a 17.0% CAGR through 2035.

- Oncology represented the largest application at 39.0% of the Bronchoscopes Market, fueled by rising lung-cancer incidence globally.

- ICU airway management is the fastest-growing application, tracking a 13.7% CAGR as critical-care admissions expand in emerging economies.

• By Region

- North America captured 44.5% of the Bronchoscopes Market share in 2025.

- Asia-Pacific is forecast to grow at a 10.2% CAGR through 2035, the highest among all regions.

- Europe contributed approximately USD 1.27 billion in 2025, underpinned by MDR-compliance capital expenditures.

Market Size and Forecast (2021–2035)

Market Research Future's estimates blend bottom-up device shipment data from 85+ OEMs with top-down cross-referencing against national health-expenditure databases, CMS claims records, and trade-association procedure volumes. Historical figures draw on audited company filings; forecast values apply a calibrated compound growth model adjusted for regulatory pipeline events and demographic screening projections.