Building Thermal Insulation Market Summary

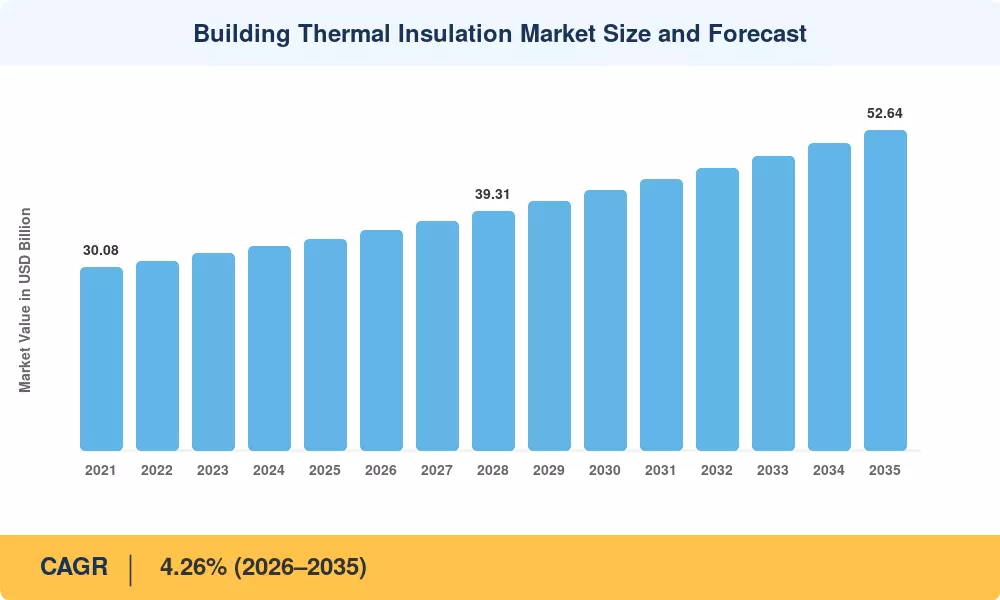

The Building Thermal Insulation Market stood at USD 34.78 billion in 2025 and is projected to reach USD 36.16 billion in 2026, climbing to USD 52.64 billion by 2035 at a CAGR of 4.26% during 2026–2035. Tightening energy-performance building codes across the EU, North America, and parts of Asia-Pacific have converted insulation from an optional upgrade into a compliance requirement. The European Commission's revised Energy Performance of Buildings Directive (EPBD), targeting near-zero-energy standards for all new structures by 2030, is a direct demand catalyst that underpins the Building Thermal Insulation Market trajectory through the forecast period [1].

Materials innovation is shifting the competitive landscape. Under the Kigali Amendment, regulators are phasing out high-GWP blowing agents, which is leading to the replacement of legacy polystyrene foams with low-global-warming-potential (GWP) formulations. At the same time, prefabricated insulated panel systems are on the rise – the worldwide prefabricated building market secured over USD 130 billion in investment pledges during 2023-2024, drawing insulation suppliers deeper into off-site construction supply chains [2]. Architects may now predict thermal performance in real-time to shorten material selection cycles with digital specification tools.

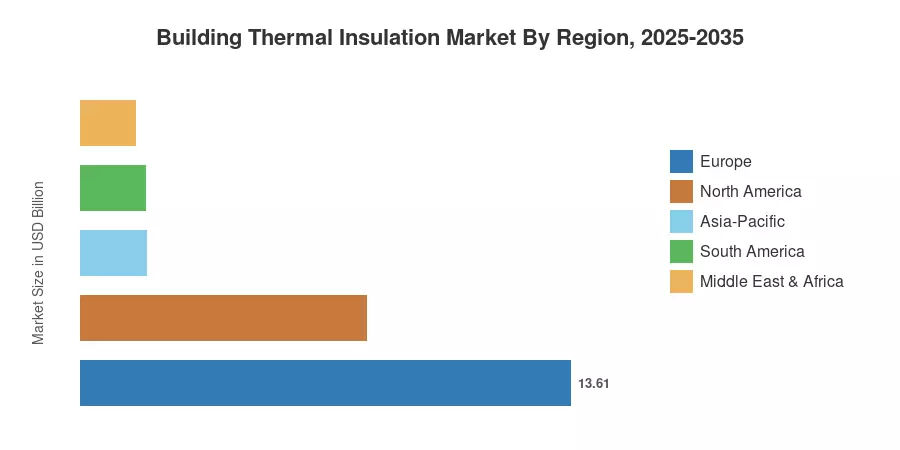

Europe dominates the Building Thermal Insulation Market, generating 39.12% of revenue in 2025 due to strict retrofit requirements and carbon-pricing policies. Asia-Pacific is the fastest expanding area with a CAGR of 5.23% through 2035, driven by China’s dual-carbon ambitions and India’s Energy Conservation Building Code revisions. North America’s second-largest segment is 22.80% [3], anchored by Inflation Reduction Act subsidies and state-level green building rules. The next 10 years will depend on how quickly the economics of refurbishment improve in price-sensitive developing markets.

Key Report Takeaways

• By Material Type

- Fiberglass held a 37.1% share of the Building Thermal Insulation Market in 2025, retaining its position as the dominant material segment due to cost-effectiveness and broad code compliance.

- Polystyrene insulation is expanding at a 4.51% CAGR through 2035, driven by lightweight panel demand in commercial roofing applications.

• By Application

- Roof installations captured a 27.14% share in 2025, reflecting mandatory cool-roof and thermal-envelope regulations in temperate and tropical climates.

- Acoustic partition and HVAC duct insulation applications are advancing at a 5.19% CAGR during 2026–2035

• By End-User

- Residential construction accounted for a 52.23% share of the Building Thermal Insulation Market in 2025, supported by housing stimulus programs across emerging economies.

• By Geography

- Europe retained its dominant position in the Building Thermal Insulation Market with a 39.12% share in 2025, while Asia-Pacific is tracking the fastest expansion at a 5.23% CAGR.

Market Size and Forecast (2021–2035)

A unique combination of bottom-up and top-down approaches derives Market Research Future (MRFR) estimates. Historical values (2021–2024) are based on verified shipment data and trade statistics; base year (2025) incorporates preliminary quarterly filings; and forecast period (2026–2035) utilizes demand-side modeling calibrated against construction-activity forecasts, energy-code timelines and raw-material price indices.