Calcined Petroleum Coke Market Summary

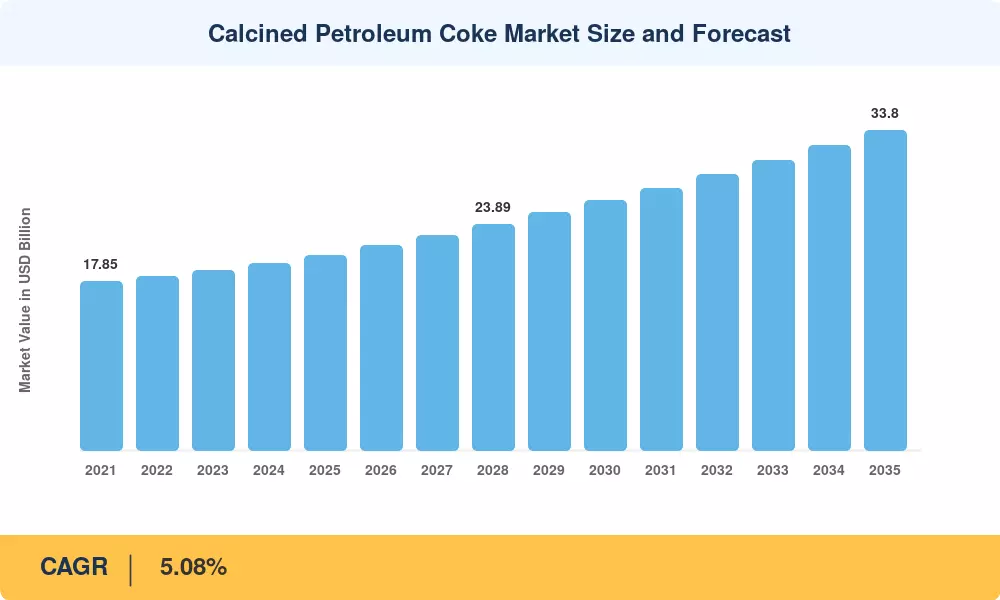

The calcined petroleum coke market was valued at USD 20.58 Billion in 2025 and is projected to grow from USD 21.63 Billion in 2026 to USD 33.80 Billion by 2035, registering a CAGR of 5.08% during the forecast period (2026–2035). This expansion is anchored by sustained demand from primary aluminum production — which consumes roughly 70% of all calcined material globally — and by tightening sulfur-content specifications that are pushing refiners toward higher-quality delayed coking units [1]. China's 14th Five-Year Plan allocated over USD 12 Billion to modernize its smelting infrastructure through 2025, creating durable procurement cycles for premium-grade coke [2].

The calcined petroleum coke market is experiencing a structural shift in supply economics. Middle-East refiners have pivoted from crude export toward in-house delayed coking, reducing the global surplus of sponge-grade feedstock and lifting spot prices for calcinable material by 18–22% since 2022 [3]. At the same time, the European Union's Carbon Border Adjustment Mechanism (CBAM), phased in from 2026, is redirecting trade flows: producers in regions with relaxed emission standards are gaining price advantage, while EU-based smelters face rising input costs [4].

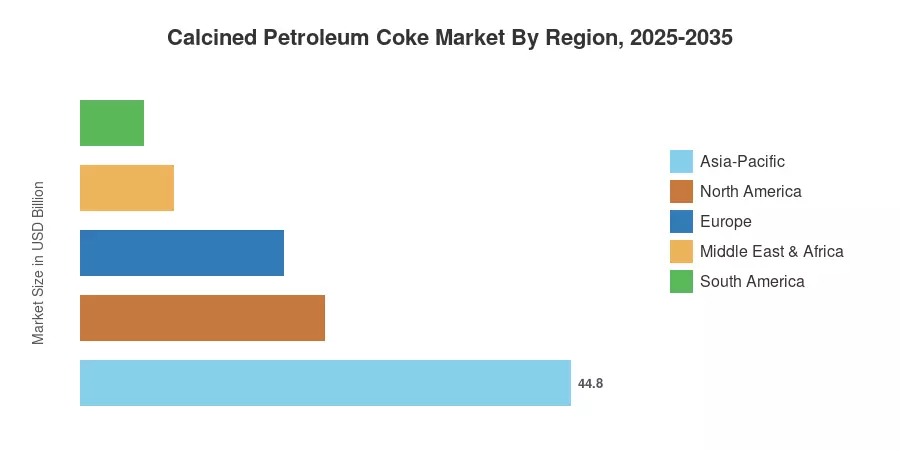

Asia-Pacific commanded 44.8% of the calcined petroleum coke market in 2025, driven by China's aluminum capacity and India's cement and steel sectors. The Middle East & Africa region is forecast to record the highest regional CAGR at 6.14% through 2035, supported by Saudi Arabia's downstream integration strategy under Vision 2030. North America held the second-largest share at 22.3%, underpinned by robust refinery throughput in the U.S. Gulf Coast corridor. The calcined petroleum coke market trajectory through 2035 will hinge on how quickly low-carbon alternatives penetrate the anode supply chain.

Key Report Takeaways

• By Type

- Fuel Grade held the dominant share of the calcined petroleum coke market in 2025, accounting for 57.2% of total revenue.

- Calcined Coke is forecast to register the fastest growth at a 6.20% CAGR through 2035, driven by rising anode-grade specifications in smelting operations.

• By Application

- The calcined petroleum coke market was led by the Calcined Petroleum Coke application segment, which captured 51.1% of revenue in 2025.

- The Green Petroleum Coke application segment is expected to post the highest growth rate at 6.23% CAGR through 2035.

• By Region

- Asia-Pacific dominated the calcined petroleum coke market with a 44.8% revenue share in 2025, led by China and India.

- The Middle East & Africa region is projected to achieve the highest CAGR of 6.14% during 2026–2035.

Market Size and Forecast (2021–2035)

Market size estimates draw on a proprietary bottom-up methodology combining refinery coking capacity data, trade-flow modeling, and primary interviews with over 45 industry participants across six regions. Historical data (2021–2024) relies on verified customs statistics and company financial disclosures, while the forecast period applies scenario-weighted demand curves validated against IEA and World Bank projections [1][5].