Carbon Offset Carbon Credit Market Summary

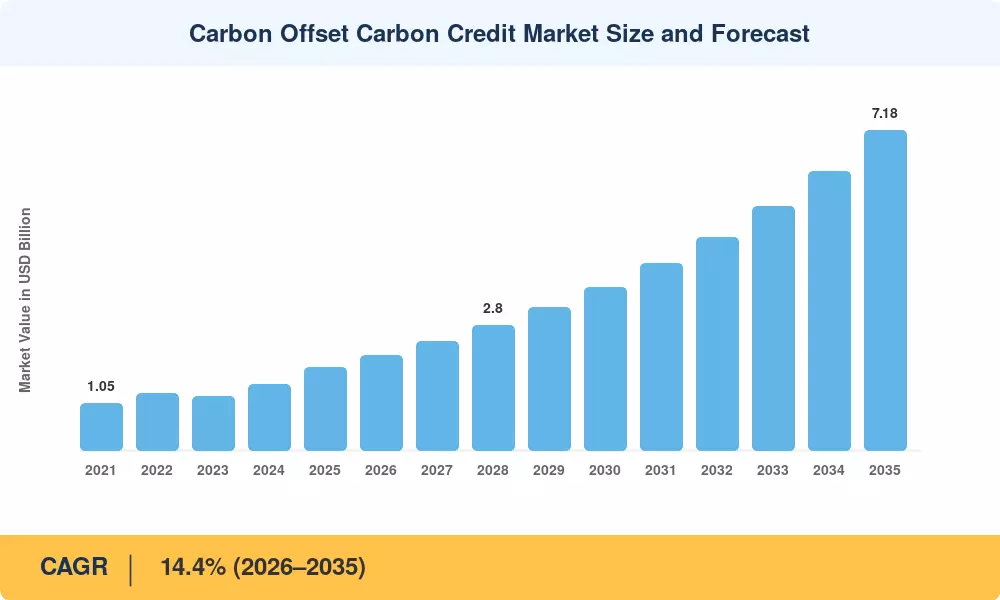

The Carbon Offset Carbon Credit Market reached an estimated USD 1.87 billion in 2025 and is projected to grow from USD 2.14 billion in 2026 to USD 7.18 billion by 2035, registering a CAGR of 14.4% during the forecast period (2026–2035). Two forces are accelerating this trajectory: the tightening of national emissions caps under Article 6 of the Paris Agreement and the surge of corporate climate pledges — over 6,000 companies globally have now set science-based targets, many requiring offset procurement to close residual emissions gaps [1]. Regulatory momentum, particularly through the EU Carbon Border Adjustment Mechanism (CBAM) that began its transitional phase in 2023, has injected compliance-driven urgency into credit demand [2].

A structural transformation is reshaping how credits are generated, verified, and retired. Legacy offset projects with opaque additionality claims are giving way to digitized measurement, reporting, and verification (MRV) platforms that use satellite imagery and IoT sensors. BloombergNEF estimates that investment in carbon-market infrastructure — registries, exchanges, and tokenization platforms — exceeded USD 1.3 billion in 2024 alone [3]. Governments are simultaneously expanding compliance schemes: China's national ETS now covers more than 5 billion tonnes of CO₂ annually, and South Korea's K-ETS tightened its free-allocation ratio by 3 percentage points in 2024 [4].

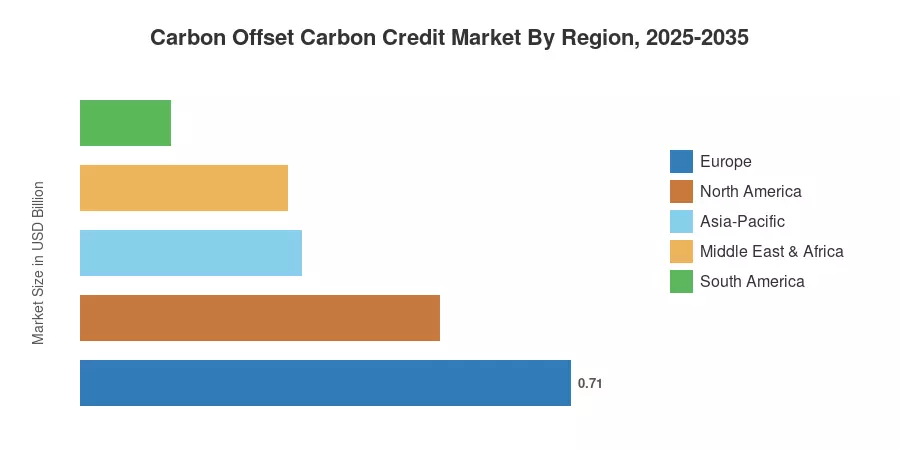

Europe commands the dominant share of the Carbon Offset Carbon Credit Market at approximately 38% of global value, underpinned by the EU Emissions Trading System's mature auction-based framework. Asia-Pacific is the fastest-growing region, posting a projected CAGR above 17%, driven by nascent compliance schemes in India, Indonesia, and Vietnam. North America holds the second-largest share near 28%, buoyed by California's cap-and-trade program and the Inflation Reduction Act's clean-energy incentives [5]. The convergence of mandatory disclosure rules and voluntary ambition suggests the Carbon Offset Carbon Credit Market will remain one of the highest-growth segments in environmental finance through 2035.

Key Report Takeaways

• By Credit Type

- Compliance credits account for roughly 62% of the Carbon Offset Carbon Credit Market by value, reflecting the dominance of regulated ETS programs globally.

- Voluntary credits are expanding at a CAGR of approximately 18.6% through 2035, driven by corporate sustainability mandates and rising demand from the aviation sector.

• By Project Type

- Nature-based solutions represent the largest project category, valued at an estimated USD 0.58 billion in 2025, as forestry and land-use projects attract institutional capital.

- Renewable energy credit projects are expected to grow at a CAGR near 13.2% as solar and wind additionality standards become more stringent.

• By Region

- Europe holds the leading regional position in the Carbon Offset Carbon Credit Market, commanding a 38% share of global value in 2025.

- Asia-Pacific is forecast to register the strongest CAGR at 17.1%, with China and India introducing new or expanded compliance mechanisms.

- North America accounts for approximately USD 0.52 billion in 2025 revenue, anchored by California's cap-and-trade and voluntary purchases by US technology firms.

Carbon Offset Carbon Credit Market Size and Forecast (2021–2035)

Market Research Future analysts derived historical estimates from verified carbon registry transaction data (Gold Standard, Verra, American Carbon Registry) combined with compliance market auction records from ICAP. Forecast projections incorporate econometric modeling that weights regulatory pipeline probability, corporate pledge conversion rates, and credit price elasticity scenarios.