Cat Litter Market Summary

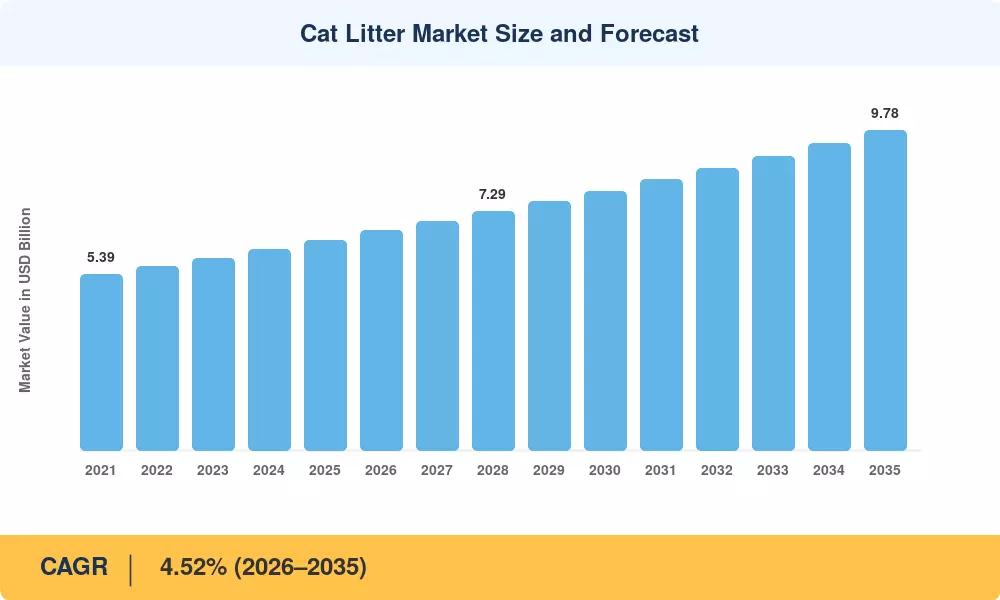

The Cat Litter Market reached an estimated USD 6.43 billion in 2025 and is projected to grow from USD 6.72 billion in 2026 to USD 9.78 billion by 2035, registering a CAGR of 4.52% during the forecast period. Rising pet humanization trends and a global surge in single-person households are anchoring this growth trajectory. The American Pet Products Association (APPA) reported that U.S. cat ownership climbed to 47.1 million households in 2024, while the European Pet Food Industry Federation (FEDIAF) documented a 3.8% year-over-year increase in European cat populations — both catalysts fueling sustained demand for clumping bentonite cat litter and premium substrates [2][3].

Product innovation is transforming the way people engage with litter products. Legacy clay-only formulas are being phased out in favor of silica gel crystal cat litter formulas, hybrid mineral-plant blends and biodegradable eco cat litter made from walnut shells, corn and recycled paper. Manufacturers spent an estimated USD 320 million in R&D in 2024 alone to develop odor control cat litter formula and dust-free processing methods that address crystalline silica health concerns [4]. The lightweight, sensor-compatible substrates are gaining popularity, especially in the automatic self-cleaning litter box industry, which is worth more than USD 1.2 billion globally [5].

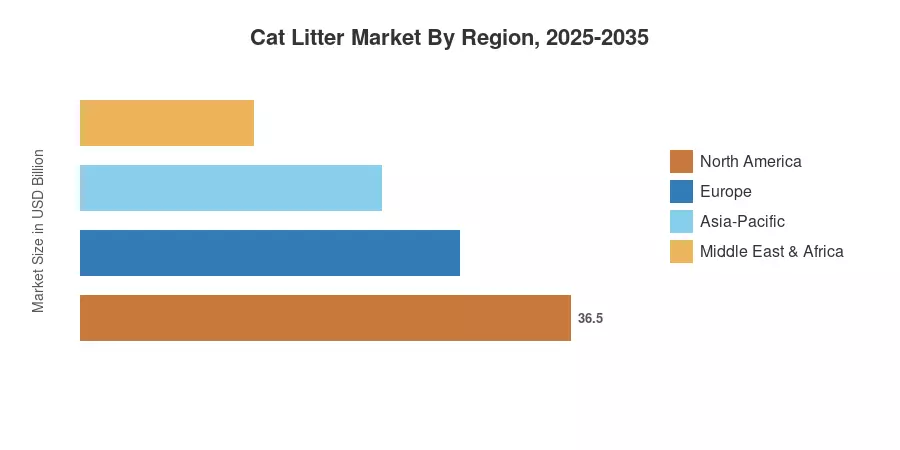

Europe accounted for the greatest revenue share of almost 40.2% in the Cat Litter Market in 2025, due to strict rules in the EU on packaging and biodegradability. The North American region is the fastest expanding, with a 4.82% CAGR through 2035, fueled by direct-to-consumer subscription models and premiumization. The Asia-Pacific is the second largest opportunity, with urban cat adoption in China, Japan and South Korea driving regional demand to surpass USD 1.1 billion. Over the next 10 years, brands that can balance freight efficiency and environmental integrity will be rewarded.

Key Report Takeaways

• By Product Type

- Clumping formulations captured 63.8% of Cat Litter Market revenue in 2025, reflecting consumer preference for easy-scoop convenience and superior odor control cat litter formula performance

- Non-clumping products are forecast to expand at an 8.14% CAGR through 2035, driven by veterinary-recommended post-surgical substrates and growing interest in biodegradable eco cat litter

• By Raw Material

- Clay-based substrates, dominated by clumping bentonite cat litter, accounted for USD 3.92 billion in 2025, underpinning the Cat Litter Market's traditional supply chain

- Silica gel crystal cat litter alternatives are projected to grow at a 5.35% CAGR through 2035, supported by health-monitoring innovations and lightweight shipping advantages

• By Distribution Channel

- The online channel held a 37.1% share of the Cat Litter Market in 2025, buoyed by subscription delivery and auto-replenishment platforms

- Hypermarkets are recording the highest projected channel CAGR at 8.04% through 2035, as brick-and-mortar retailers expand premium pet aisles

• By Region

- Europe led the Cat Litter Market with 40.2% revenue share in 2025

- North America is advancing at a 4.82% CAGR, the fastest among all regions

Cat Litter Market Size and Forecast (2021–2035)

The market size of MARKET RESEARCH FUTURE is derived from a bottom-up analysis of the revenue of manufacturer shipments, distributor sell-through, and trade import/export statistics across 32 countries. The market sizing has been validated through a top-down analysis using macroeconomic indicators such as pet population growth, disposable income trends, and urbanization rates..