Chemotherapy Market Summary

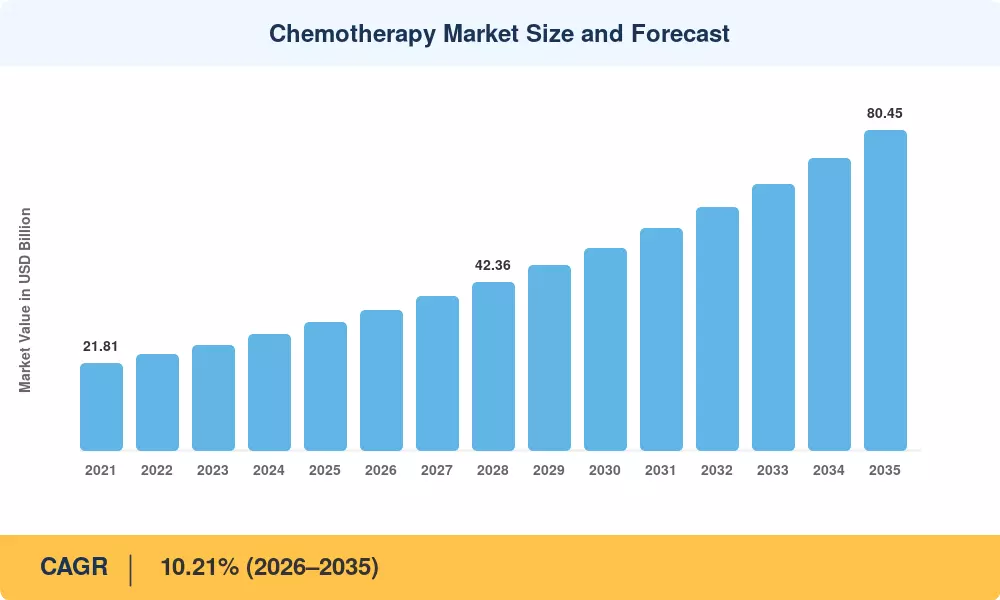

The global Chemotherapy Market reached USD 32.18 billion in 2025 and is projected to expand from USD 35.24 billion in 2026 to USD 80.45 billion by 2035, registering a CAGR of 10.21% during the forecast period (2026–2035). This trajectory is anchored by the persistent rise in global cancer incidence — the WHO estimates 20 million new cases annually by 2025 — and by national cancer-control plans that ring-fence public spending for antineoplastic treatment regimens across both high-income and developing economies [2]. Government procurement frameworks, such as India's Ayushman Bharat oncology expansion and the EU Beating Cancer Plan's EUR 4 billion commitment, continue to guarantee baseline demand for cytotoxic drug therapy.

A silent revolution is taking place in the delivery of oncology medication infusions to patients. Legacy single-agent intravenous chemotherapy regimens are being increasingly replaced by multi-agent fixed-dose combinations, oral capecitabine-based regimens, and antibody–drug conjugates including cytotoxic payloads. Between 2022 and 2024 alone, the FDA authorized 14 combination chemotherapy indications and biosimilar versions of platinum-based cancer medications in European tenders, which have reduced treatment costs by 30–45% [3]. The change is reducing the cost per cycle and expanding the pool of eligible patients.

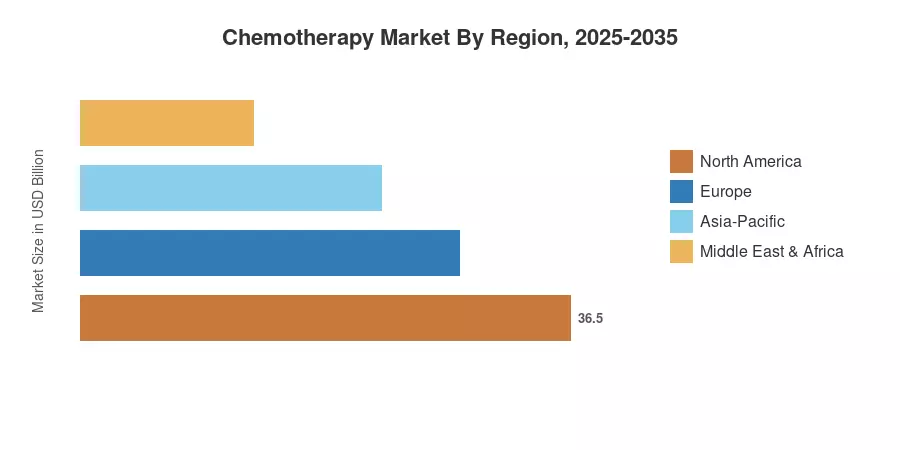

North America is anticipated to account for approximately 41.2% of the Chemotherapy Market due to high oncology spend per capita and extensive payer coverage. Asia-Pacific is expected to be the fastest-expanding region with a CAGR of 11.14% through 2035, driven by healthcare infrastructure build-outs in China and India. Europe accounts for the second-largest share at around 26.8% due to standardized EMA approval pathways and biosimilar acceptance [4]. The chemotherapy market is expected to continue its double-digit expansion well into the next decade as cancer screening programs expand in emerging economies.

Key Report Takeaways

• By Drug Class

- Alkylating agents accounted for 40.8% of the Chemotherapy Market in 2025, driven by their foundational role in combination antineoplastic treatment regimens for solid tumors and hematologic malignancies

- Antimetabolites are forecast to grow at a 10.75% CAGR through 2035, reflecting expanded use of capecitabine and pemetrexed in oral cytotoxic drug therapy schedules

• By Route of Administration

- Oral therapies represented 54.3% of the Chemotherapy Market in 2025, as patient-preference data increasingly favor at-home dosing over hospital-based oncology drug infusion

- Intravenous chemo protocols are projected to expand at 10.85% CAGR, underpinned by new platinum-based cancer drugs and antibody–drug conjugate approvals

• By Indication

- Blood cancers captured USD 8.05 billion of the Chemotherapy Market in 2025, led by multi-agent protocols for acute leukemias

- Breast cancer treatments are forecast to rise at 10.95% CAGR to 2035, reflecting trial-validated neoadjuvant and adjuvant chemotherapy regimens

• By Region

- North America dominated the Chemotherapy Market with 41.2% revenue share in 2025

- Asia-Pacific is anticipated to grow at 11.14% CAGR, the highest among all regions

Chemotherapy Market Size and Forecast (2021–2035)

Market Research Future's market sizing draws on pharmaceutical sales audits, hospital procurement databases, national cancer registries, and payer reimbursement filings across 42 countries. Historical figures (2021–2024) reflect actual reported revenues; forecast values (2026–2035) apply a calibrated CAGR validated against regulatory pipeline data and demographic cancer-incidence projections.

.webp?v=1782975712)