Chitosan Market Summary

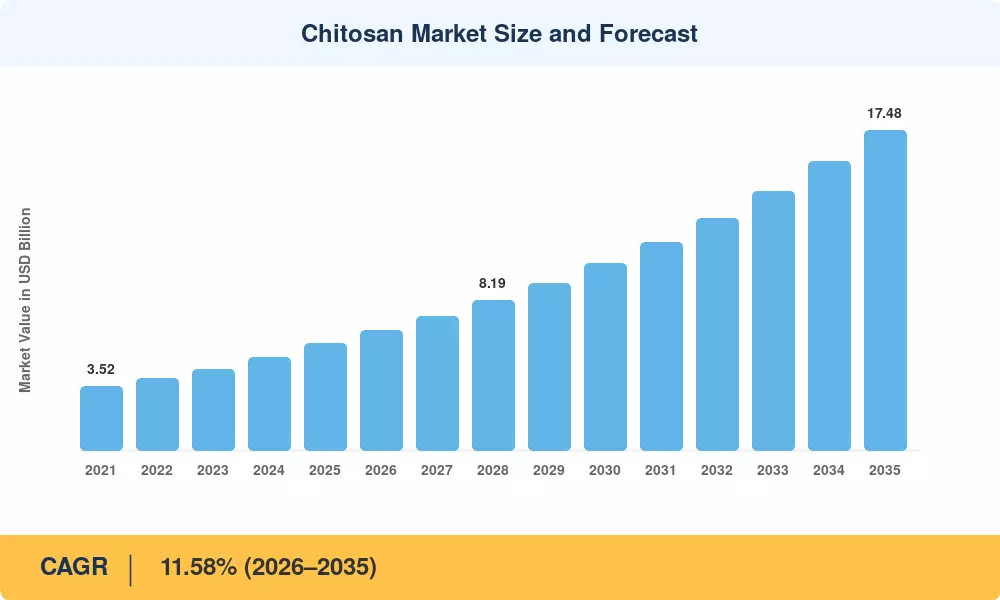

The global Chitosan Market reached an estimated USD 5.82 billion in 2025 and is projected to grow from USD 6.58 billion in 2026 to USD 17.48 billion by 2035, registering a CAGR of 11.58% over the forecast period. This expansion is anchored in the European Union's 2024 recast of the Urban Wastewater Treatment Directive, which is pushing municipal utilities to replace synthetic polyacrylamide flocculants with shellfish-derived chitosan biopolymer alternatives, and in escalating EPA heavy-metal discharge limits across the United States that favor chitosan water treatment chelators[2].

A structural transformation is reshaping the Chitosan Market as legacy petroleum-based polymers lose ground to marine-origin biopolymers. Pharmaceutical developers are scaling nano-chitosan carriers for pharmaceutical chitosan drug delivery applications that demonstrate significantly improved tumor drug accumulation rates, while cosmetic formulators integrate chitosan oligosaccharides into clean-beauty product lines [3]. Venture capital is validating this shift—circular-economy processors such as Tidal Vision closed a USD 6.5 million Series A round in 2024, signaling strong investor appetite for high-margin chitosan food preservative coating and agricultural chitosan biopesticide products [4].

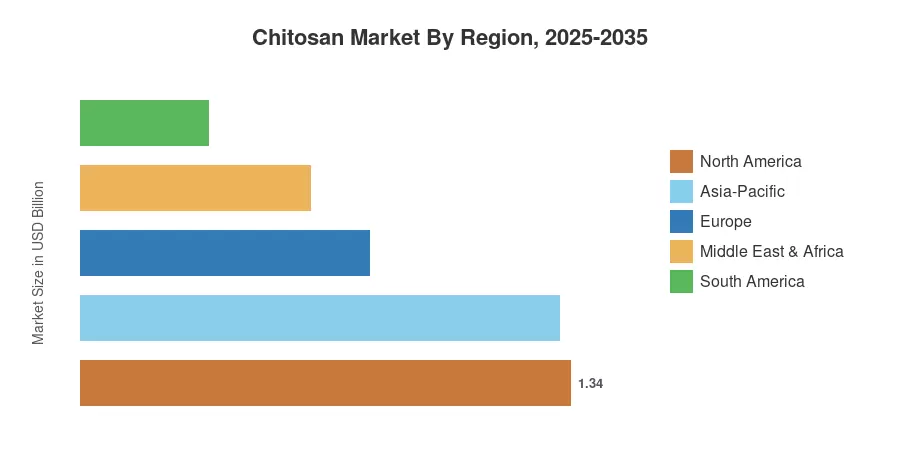

North America commands the largest share of the Chitosan Market at roughly 23% of global revenue, driven by robust demand from the U.S. water and wastewater sector. Europe is the fastest-growing region, expanding at a projected 13.58% CAGR through 2035 as regulatory mandates accelerate the adoption of biodegradable flocculants. Asia-Pacific ranks as the second-largest region, with China and India investing heavily in agricultural chitosan biopesticide formulations to reduce chemical pesticide dependency

Key Report Takeaways

• By Source

- Shrimps accounted for approximately 42% of the Chitosan Market in 2025, reflecting dominance across Southeast Asian and Indian processing corridors

- Crabs are forecast to expand at a 12.45% CAGR through 2035, fueled by crab-shell waste valorization programs in Alaska and Canada

• By Grade & Form

- Industrial-grade specifications represented about 43% of the Chitosan Market in 2025, underpinned by chitosan water treatment demand

- Nano and micro particle forms are advancing at a 12.95% CAGR, driven by pharmaceutical chitosan drug delivery research

• By Application

- Water treatment held roughly 26% of the Chitosan Market, the largest single end-use category in 2025

- Pharmaceutical and biomedical applications will register the fastest growth at a 12.82% CAGR as clinical validation of hemostatic dressings accelerates

• By Region

- North America led the Chitosan Market with approximately 23% share in 2025

- Europe is on track to expand at a 13.58% CAGR through 2035, the fastest among all regions

Chitosan Market Size and Forecast (2021–2035)

MRFR's market sizing methodology combines bottom-up revenue modeling from over 120 chitosan producers with top-down cross-validation against trade data from UNCOMTRADE and national customs databases. Historical figures (2021–2024) rely on audited company filings, while the forecast (2026–2035) applies a calibrated CAGR of 11.58% against the 2025 base year.

.webp?v=1783938003)