Cigarette Market Summary

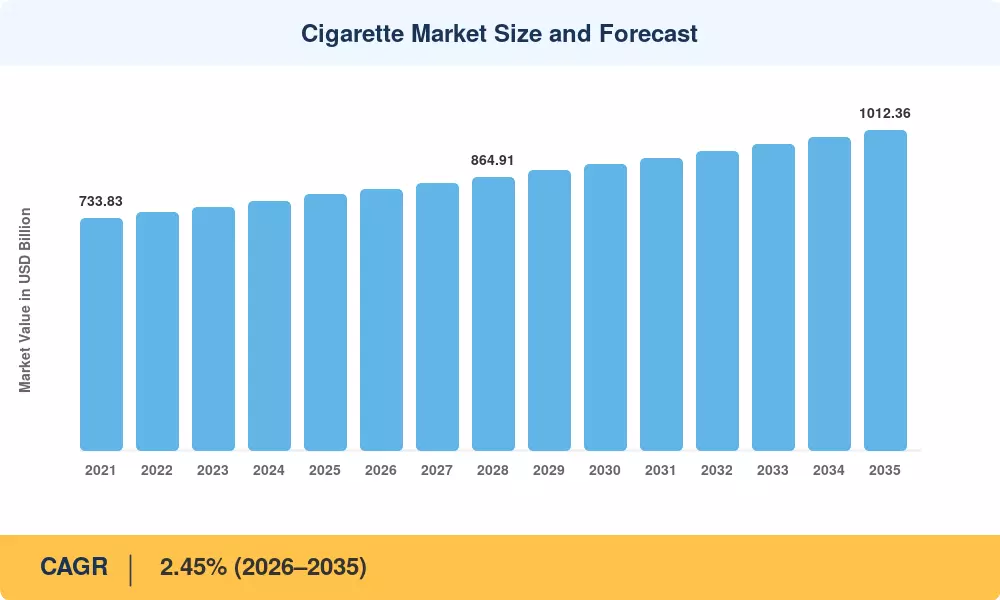

The global Cigarette Market reached an estimated USD 808.49 Billion in 2025 and is projected to grow from USD 828.70 Billion in 2026 to USD 1,012.36 Billion by 2035, registering a CAGR of 2.45% during the forecast period (2026–2035). Entrenched nicotine dependence among roughly 1.1 billion smokers worldwide and resilient tobacco cigarette consumption decline resistance in emerging economies anchor this trajectory, even as cigarette excise tax policy tightening in OECD nations reshapes the competitive landscape[2]. The WHO Framework Convention on Tobacco Control (FCTC) now covers 182 parties, yet enforcement gaps in low- and middle-income countries continue to sustain volume demand for traditional combustible products.

A quiet transformation is reshaping how cigarettes reach consumers and how manufacturers protect margins. Automation across production lines has cut unit costs by an estimated 8–12% since 2021, while track-and-trace technologies — mandated under the EU Tobacco Products Directive and gaining traction in Brazil and Kenya — help incumbents combat the USD 40+ Billion illicit trade that erodes legitimate Cigarette Market revenues [3]. Premiumization is accelerating value growth: premium cigarette brand market expansion in China, Japan, and Western Europe now offsets declining stick volumes in those same geographies, as adult smokers trade up rather than quit entirely.

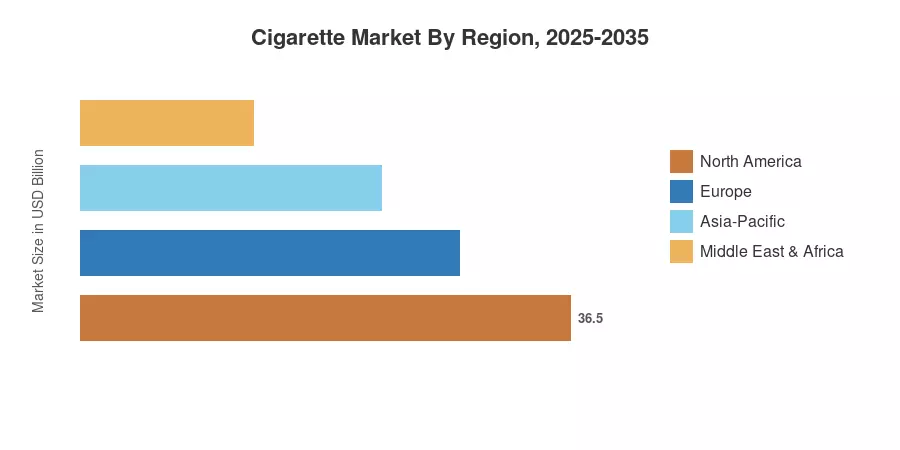

Asia-Pacific dominates the Cigarette Market with an estimated 44.63% share of 2025 revenue, powered by China's 300+ million-smoker base and rising disposable incomes across ASEAN nations Europe holds the second-largest share at roughly 22%, though menthol cigarette ban regulation and plain-packaging mandates continue to compress margins there. North America, while mature, sees the cigarette alternative vaping trend accelerating substitution, making it a bellwether for how regulatory posture shapes long-term tobacco demand. The next decade will be defined by how effectively legacy manufacturers balance premiumization against volume erosion.

Key Report Takeaways

• By Flavor Type

- Conventional unflavored cigarettes commanded approximately 90.57% of 2025 volume, reflecting deep consumer loyalty to traditional blends despite growing interest in menthol and capsule variants

• By Format

- Super-slim formats are advancing at a 3.58% CAGR through 2035, driven by health-conscious positioning and strong uptake among female smokers in Asia-Pacific and Europe

- King-size format held approximately 55.52% of 2025 volume, maintaining its status as the default Cigarette Market format globally

• By Category

- Mass-market lines accounted for an estimated USD 729.86 Billion of the 2025 Cigarette Market revenue, underpinning the industry's volume-driven economics

- The premium segment is set to grow at a 4.32% CAGR, reflecting premiumization trends in China and Western Europe, where tobacco cigarette consumption decline in volume is offset by value gains By End User

- Men represented roughly 89.82% of 2025 consumption; women constitute the fastest-growing demographic at an estimated 3.65% CAGR

• By Region

- Asia-Pacific captured the largest Cigarette Market share with approximately 44.63% of 2025 revenue and is expanding at a 3.72% CAGR

- North America held roughly 18% of global revenue in 2025, with the US market shaped heavily by cigarette excise tax policy and the cigarette alternative vaping trend

- The Middle East & Africa region is forecast to reach a 2.98% CAGR, buoyed by population growth and limited regulatory enforcement

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates primary interviews with tobacco executives, distributor sell-through data, excise-tax revenue filings from 45+ countries, and cross-validation against trade-association shipment reports. Historical figures (2021–2024) reflect actual industry performance; the 2025 base year uses preliminary data, and the 2026–2035 forecast applies a calibrated CAGR of 2.45%.