Commercial Aircraft Landing Gear Market Summary

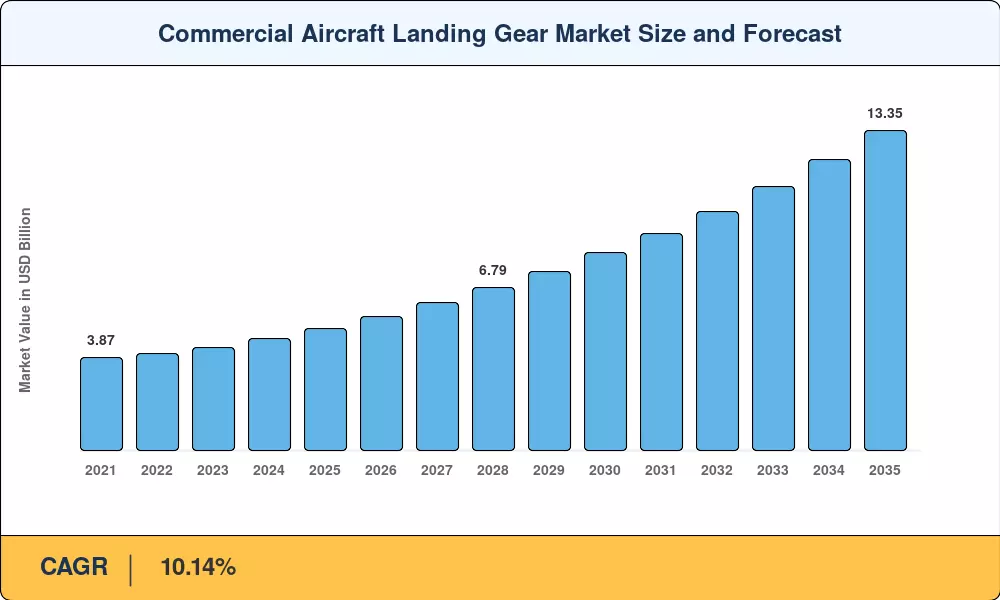

The Commercial Aircraft Landing Gear Market was valued at USD 5.08 billion in 2025 and is projected to reach USD 5.60 billion in 2026 before expanding to USD 13.35 billion by 2035, registering a compound annual growth rate of 10.14% during the 2026–2035 forecast window. Record-high single-aisle order backlogs — exceeding 14,000 aircraft across major OEMs — have locked in multi-year production schedules that translate directly into landing-gear procurement commitments [1]. Airlines face regulatory pressure to cut per-seat emissions under ICAO's Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), incentivizing fleet renewal with lighter, more efficient airframes that require next-generation gear systems [2].

The transformation of technology in the Commercial Aircraft Landing Gear Market is driven towards the replacement of traditional hydraulic actuation with electro-mechanical and electro-hydrostatic. Safran Landing Systems committed approximately EUR 250 million between 2022 and 2024 on additive-manufactured titanium components and electric taxi systems, providing weight savings of more than 280 kilograms per shipset on narrowbody platforms [3]. The uptake of carbon-ceramic brakes has moved from widebody flagships down into narrowbody fleets, leading to a reduction in brake system mass of almost 40% with improved repair intervals from 1500 to over 3000 landings [4].

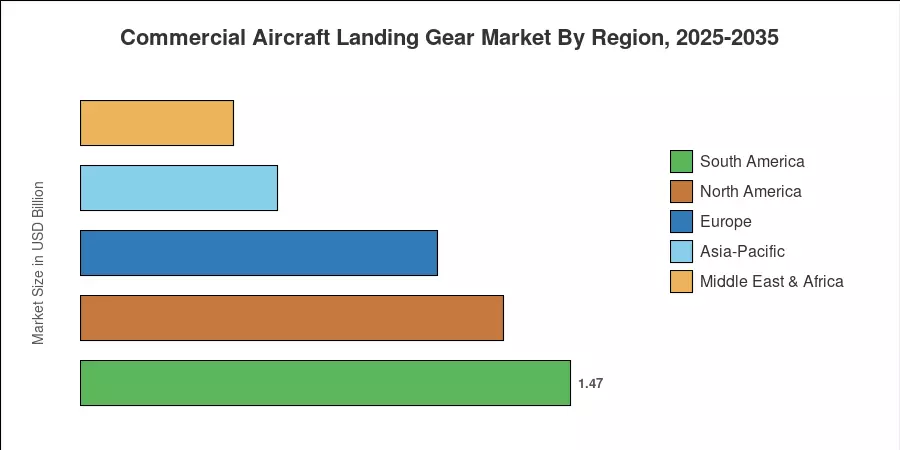

South America is the largest region with about 29% of worldwide revenue, supported by clustered MRO activity in Brazil and major fleet-replacement projects among Latin carriers. The Asia-Pacific area is the fastest-expanding region with a predicted CAGR of 11.64%. The growth is spurred by fleet development in China and India. North America is the second-largest market and is driven by the OEM production facilities and the aftermarket scale. The Commercial Aircraft Landing Gear Market is at an inflection point where the convergence of manufacturing rate increases, material innovation and sustainability standards is reshaping demand through the future decade.

Key Report Takeaways

• By Landing Gear Type

- Main landing gear assemblies accounted for 80.1% of the Commercial Aircraft Landing Gear Market revenue in 2025, reflecting the structural complexity and premium pricing of multi-wheel bogie systems on narrowbody and widebody platforms.

- Nose landing gear is forecast to grow at a 10.33% CAGR through 2035, driven by electric nose-wheel taxi integration and steerable nose-gear electronics upgrades across next-generation single-aisle programs.

• By Aircraft Type

- Narrowbody platforms captured 70.1% share of the Commercial Aircraft Landing Gear Market in 2025, as A320neo-family and B737 MAX production ramp-ups dominated OEM procurement.

- Widebody landing-gear systems are projected to expand at an 11.04% CAGR through 2035, supported by long-haul fleet renewals and twin-aisle new-program launches.

• By Geography

- South America led the Commercial Aircraft Landing Gear Market with a 29% regional share in 2025, anchored by large-scale MRO operations and fleet modernization cycles.

- Asia-Pacific is forecast to advance at an 11.64% CAGR, driven by the expansion of indigenous aircraft programs and growing passenger traffic across China, India, and ASEAN nations.

Market Size and Forecast (2021–2035)

The historical and predicted numbers below are a mix of primary research and OEM delivery dates, airline fleet planning and MRO spending trends. Historical figures (2021–2024) are derived from reported revenue of the five main landing-gear suppliers, and forecast-period projections are developed using a calibrated growth model using production-rate trajectories and aftermarket lifetime assumptions.