Consumer IoT Market Summary

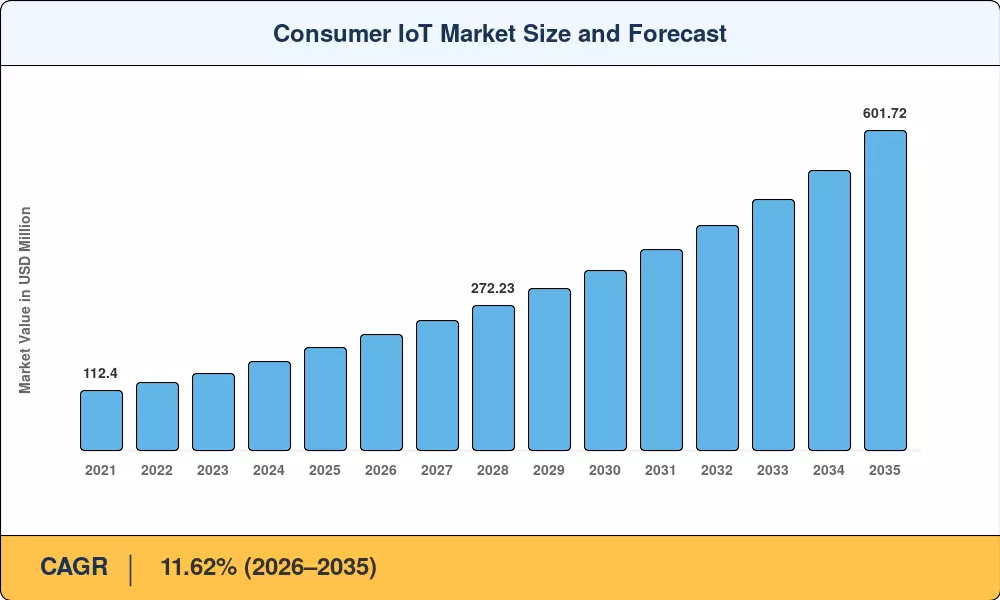

The consumer IoT market was valued at USD 193.97 billion in 2025 and is projected to reach USD 218.50 billion in 2026 before climbing to USD 601.72 billion by 2035, advancing at a CAGR of 11.62% during the forecast period (2026–2035). This expansion is propelled by escalating regulatory mandates around residential energy efficiency — the U.S. Inflation Reduction Act alone has channeled over USD 9 billion toward smart home retrofits and energy management IoT for residential homes — alongside the commercial maturation of Matter and Thread protocol for consumer IoT interoperability[2].

A sweeping technology transformation is reshaping how households interact with connected devices. Legacy proprietary ecosystems built on fragmented Zigbee and Z-Wave stacks are giving way to unified architectures enabled by Matter 1.5, which introduced cross-brand camera and sensor interoperability in late 2024. Investment in on-device large-language-model inference has surpassed USD 4.2 billion cumulatively across the top four platform holders, enabling voice assistant-integrated IoT home devices to process commands locally rather than relying on cloud round-trips [3][4].

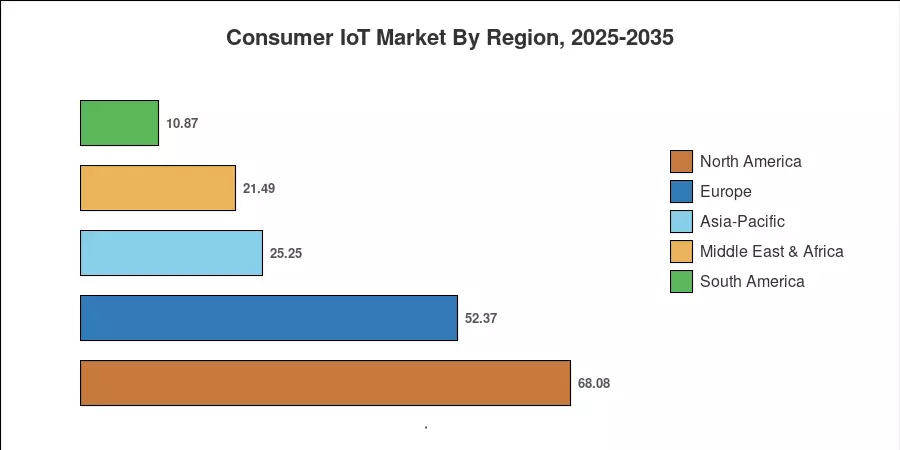

North America commands the largest share of the consumer IoT market at roughly 35.1% of 2025 global revenue, underpinned by dense broadband penetration and aggressive smart home IoT devices and ecosystems bundling by cable and telecom operators. Asia-Pacific, growing at the fastest clip among all regions, benefits from India's Production-Linked Incentive scheme for IoT hardware and China's "Digital Household" Five-Year Plan subsidies. Europe holds the second-largest share at approximately 27%, driven by the EU Energy Performance of Buildings Directive mandating smart thermostat pre-installation in new construction from 2027 onward [5][6].

Key Report Takeaways

• By Product Type

- Hardware accounted for roughly 44.2% of consumer IoT market revenue in 2025, reflecting continued demand for smart home IoT devices and ecosystems across residential deployments

- Services are expected to register a CAGR of 12.18% through 2035, as recurring subscription models for wearable health IoT for consumers gain traction

• By Connectivity Technology

- Wi-Fi maintained a dominant share of approximately 40.1% of consumer IoT market deployments in 2025, driven by Wi-Fi 6E and Wi-Fi 7 router upgrades

- Ultra-Wideband connectivity is forecast to grow at a 12.56% CAGR through 2035, fueled by precision-location use cases in voice assistant-integrated IoT home devices

• By Application

- Home Automation captured the largest segment of consumer IoT market revenue at roughly 42.3% in 2025, led by energy management IoT for residential homes

- Healthcare Devices are poised to expand at a 12.85% CAGR through 2035, reflecting surging demand for wearable health IoT for consumers, such as continuous glucose monitors and ECG patches

• By Region

- North America held the dominant position in the consumer IoT market in 2025, accounting for 35.1% of global revenue

- Asia-Pacific is set to register the highest growth at a 13.02% CAGR between 2026 and 2035

MRFR's proprietary triangulation methodology cross-references bottom-up device shipment data from 140+ OEMs, top-down macroeconomic indicators (broadband penetration, disposable income indices), and validated trade-flow databases to derive annual market sizing for the consumer IoT market.

.webp?v=1785575852)