Container Security Market Summary

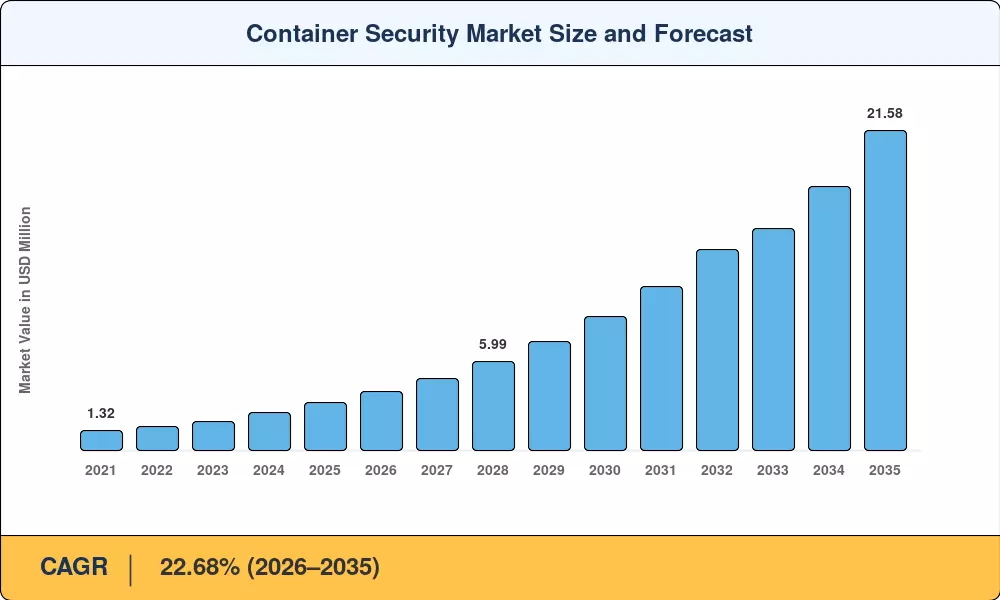

The Container Security Market was valued at USD 3.27 billion in 2025 and is projected to reach USD 3.98 billion in 2026 before climbing to USD 21.58 billion by 2035, registering a CAGR of 22.68% during the forecast period (2026–2035). Two catalysts are reshaping spending patterns: the enforcement of PCI-DSS 4.0 software-bill-of-materials (SBOM) mandates and the EU's NIS2 Directive, both of which compel enterprises to prove provenance for every container image running in production [1][2]. These regulatory deadlines have converted container security from an engineering preference into a boardroom compliance line item.

Underneath the policy pressure sits a technology shift that began a decade ago but is still accelerating. Legacy monolithic applications — once defended by perimeter firewalls and host-based agents — are being broken into hundreds of microservices orchestrated through Docker and Kubernetes container security scanning toolchains. Market Research Future estimates that by 2027, more than 90 percent of global enterprises will run containerized applications in production, up from roughly 65 percent in 2024 [3]. That migration forces security teams to adopt image vulnerability scanning in CI/CD pipelines, runtime protection for containerized workloads, and policy-as-code frameworks that travel with the application rather than the server.

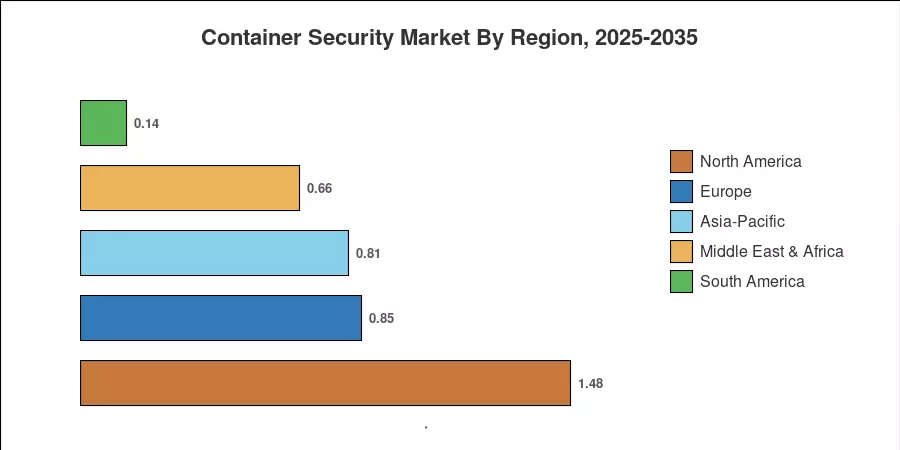

North America commands the largest share of the Container Security Market at roughly 45.38% of 2025 revenue, driven by audit-heavy verticals such as banking and healthcare Asia-Pacific is the fastest-growing region with a projected CAGR of 24.90%, fueled by China's sovereign-cloud regulations and India's Digital Public Infrastructure program [4]. Europe holds the second-largest share at approximately 26 percent, where NIS2 compliance timelines are accelerating procurement. As container sprawl intensifies across hybrid and multi-cloud estates, the Container Security Market is poised for sustained double-digit expansion through the mid-2030s.

Key Report Takeaways

• By Component

- Platforms and software accounted for 67.34% of the 2025 Container Security Market revenue, reflecting enterprise preference for integrated scanning and runtime protection for containerized workloads

- Services are forecast to expand at a 23.55% CAGR through 2035 as organizations outsource secrets management for containerized applications and compliance auditing

• By Deployment & Organization Size

- On-premise deployments captured 62.55% of 2025 spending, led by regulated industries requiring air-gapped container network policy enforcement

- Small and medium enterprises are projected to grow at a 25.22% CAGR, driven by cloud-native platforms that bundle image vulnerability scanning in CI/CD pipelines with pay-as-you-go pricing

• By Geography

- North America led the Container Security Market with a 45.38% share in 2025

- Asia-Pacific is advancing at a 24.90% CAGR, the fastest among all regions

- Europe contributed approximately USD 0.85 billion in 2025 on the back of NIS2-driven procurement

MRFR's sizing model triangulates bottom-up vendor revenues, top-down IT security spending ratios, and primary surveys of 420 enterprise DevSecOps teams across 18 countries. Historical figures (2021–2024) are reconciled against published vendor earnings and Market Research Future IT spending data; forecast values (2026–2035) apply the calibrated 22.68% CAGR with year-specific adjustments for regulatory milestones and macroeconomic cycles [3].