Corn Starch Market Summary

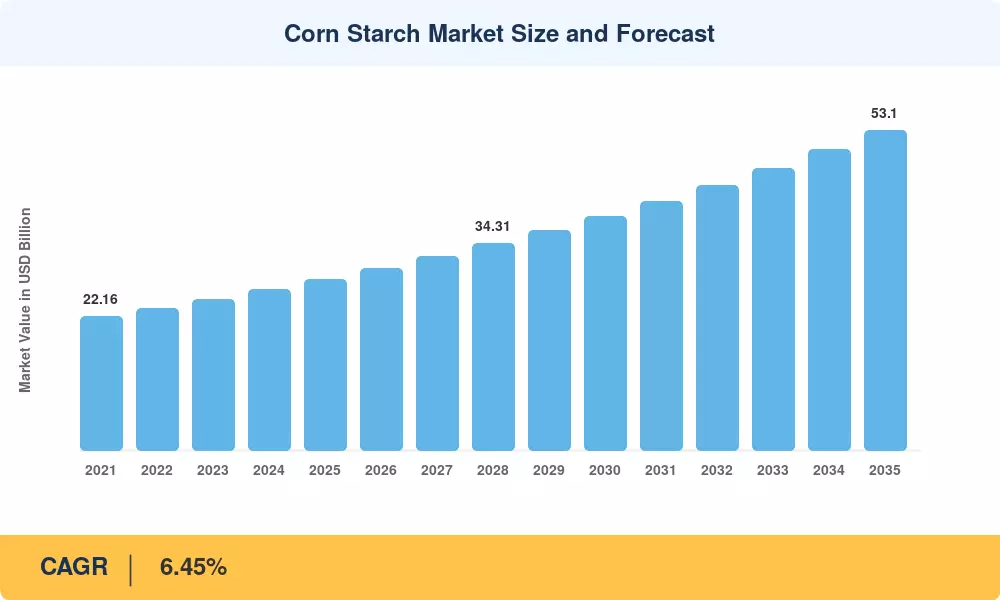

The Corn Starch Market closed 2025 at roughly USD 28.45 billion and is projected to enter 2026 at USD 30.28 billion, advancing to USD 53.10 billion by 2035 at a 6.45% CAGR through the forecast window. Two policy levers anchor that trajectory: the USDA BioPreferred Program's continued expansion of federal procurement preferences for renewable-carbon ingredients, and the FDA's 2025 reaffirmation of clean-label labeling guidance that has accelerated reformulation cycles among packaged-food majors. Capital deployment in wet-milling modernization crossed USD 1.8 billion in 2025, with Cargill and ADM together committing roughly USD 600 million to enzyme-assisted starch modification lines.

Procurement is shifting away from petroleum-derived thickeners and synthetic excipients toward bio-based alternatives, with native corn starch food ingredient demand replacing legacy modified phosphates in dairy, soup, and bakery formats. The Corn Starch Market has absorbed a 22% year-over-year jump in patent filings tied to enzymatic conversion, indicating a clear pivot from commodity tonnage to functional specialization. Asia-Pacific's packaged-food output, now valued at USD 920 billion per FAO data, is the largest demand pull globally.

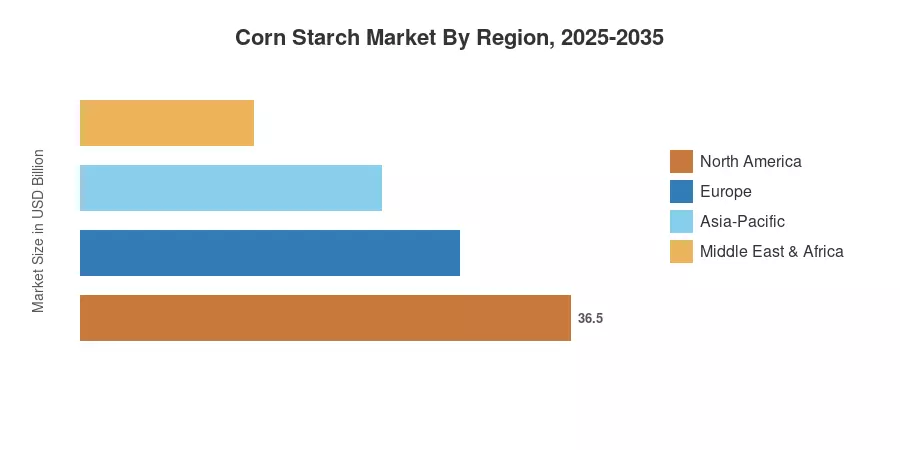

North America held 33.6% of 2025 turnover, anchored by mature US wet-milling capacity, while Asia-Pacific is poised to log a 7.85% CAGR through 2035 on the back of generic-drug excipient demand and confectionery growth. Europe remains the second-largest cluster, supported by EU bio-economy targets pushing biodegradable packaging adoption. The decade ahead will reward producers who can certify non-GMO grades at scale.

Key Report Takeaways

• By Type

- Native starch led the Corn Starch Market with 53.5% revenue share in 2025

- Modified grades are projected to advance at a 7.05% CAGR through 2035, the fastest among type segments

- Pre-gelatinized variants of modified food starch thickener are gaining share in instant-mix categories

• By Form

- Powder form generated USD 23.6 billion in 2025 across the Corn Starch Market

- Liquid starch is forecast to grow at a 7.62% CAGR, fastest among form categories

• By Application

- Food and beverages captured 48.2% of revenue in 2025

- Pharmaceutical corn starch excipient demand is forecast to grow at an 8.05% CAGR through 2035

- Industrial corn starch application in paper and corrugating is expected to reach USD 7.4 billion by 2035

• By Region

- North America commanded 33.6% of Corn Starch Market revenue in 2025

- Asia-Pacific is forecast to log a 7.85% CAGR through 2035

- Europe held USD 7.2 billion in 2025 turnover

Market Size and Forecast (2021–2035)

Market sizing draws on USDA Economic Research Service grind data, Corn Refiners Association tonnage disclosures, customs trade flows from UN Comtrade, and company-reported wet-milling revenue triangulated against MRFR's primary interviews with 42 procurement leads across food, pharma, and paper verticals. Volume-to-value conversion uses regional FOB pricing benchmarks updated quarterly.

.webp?v=1783339557)