Current Sensor Market Summary

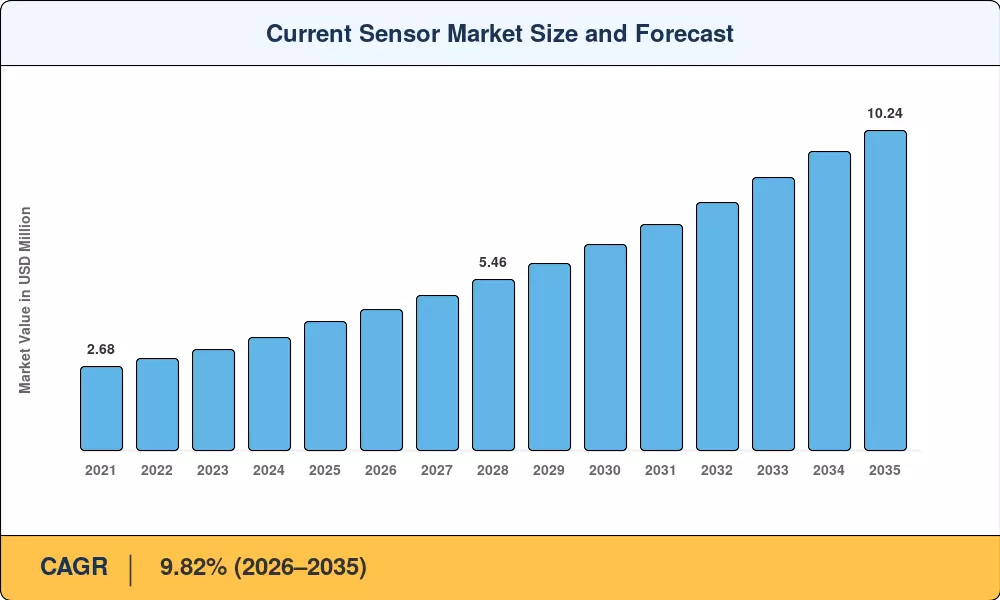

The Current Sensor Market reached an estimated USD 4.12 billion in 2025 and is projected to grow from USD 4.52 billion in 2026 to USD 10.24 billion by 2035, registering a CAGR of 9.82% during the forecast period (2026–2035). Electrification mandates across the automotive and industrial sectors are the primary catalysts behind this trajectory. The European Union's Euro 7 emissions standard — requiring real-time powertrain current monitoring in every new vehicle sold after 2025 — and the U.S. Inflation Reduction Act's USD 7,500 EV tax credits have accelerated OEM procurement of Hall-effect current sensing ICs and shunt resistor current measurement solutions at an unprecedented pace [1].

A decisive technology shift is reshaping the Current Sensor Market landscape. Legacy shunt-based architectures, dominant for decades in industrial motor drives, are giving way to non-contact current sensing for EV battery management systems and fluxgate current transducers for high accuracy in grid-tied inverters. Tunnelling magnetoresistance (TMR) sensor development attracted over USD 320 million in combined R&D investment from leading semiconductor firms between 2023 and 2025, signaling a migration toward galvanically isolated, high-bandwidth solutions that reduce board space by up to 40% [2].

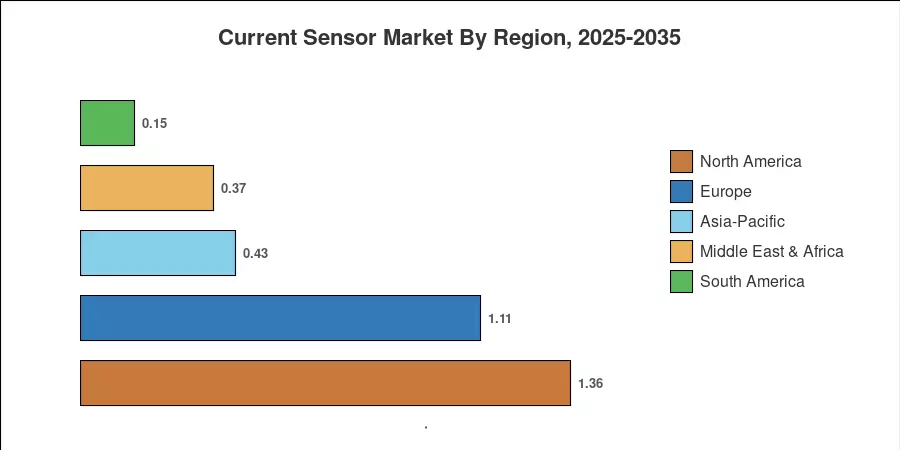

North America commands the largest regional share at approximately 33% of the Current Sensor Market, driven by data-center power monitoring demand for AI workloads and federal grid modernization programs. Asia-Pacific is the fastest-growing region with a CAGR exceeding 10.5%, fueled by China's EV production subsidies and India's PLI scheme for semiconductor manufacturing. Europe holds the second-largest share, near 27%, anchored by stringent functional-safety standards and renewable-energy integration targets. By 2035, the convergence of vehicle electrification, smart-grid deployment, and industrial automation will sustain double-digit growth pockets across all major geographies [3].

Key Report Takeaways

• By Sensor Type

- Hall-effect current sensing ICs dominated the Current Sensor Market with approximately 44% revenue share in 2025, reflecting their cost-performance advantage in automotive and consumer applications

- Fiber-optic current sensors are forecast to deliver a CAGR of 13.1% through 2035, gaining traction in high-voltage substation monitoring where electromagnetic immunity is critical

- Current transformer for AC power measurement devices accounted for roughly USD 0.74 billion in 2025, sustaining demand from legacy industrial metering upgrades

• By End-User Industry

- Automotive and transportation held the leading share of the Current Sensor Market at approximately 35% in 2025, propelled by EV battery management and ADAS power monitoring requirements

- The energy and power segment is advancing at an 11.4% CAGR to 2035, as solar and wind installations multiply sensor nodes per megawatt

• By Region

- Asia-Pacific captured roughly 43% of the Current Sensor Market in 2025, with China alone contributing over half of the regional volume

- North America's current sensor demand is underpinned by hyperscale data-center buildouts, with the region maintaining the largest absolute revenue through 2035

Current Sensor Market Size and Forecast (2021–2035)

MRFR's market sizing employs a bottom-up revenue model triangulated with import/export databases, company financial disclosures, and application-level demand estimates across automotive, industrial, energy, and telecom verticals. Historical figures (2021–2024) are validated against semiconductor shipment data from WSTS and SIA, while forecast years apply scenario-weighted growth assumptions calibrated to regional electrification roadmaps and technology adoption curves [4].

.webp?v=1782225630)