Customer Data Platform Market Summary

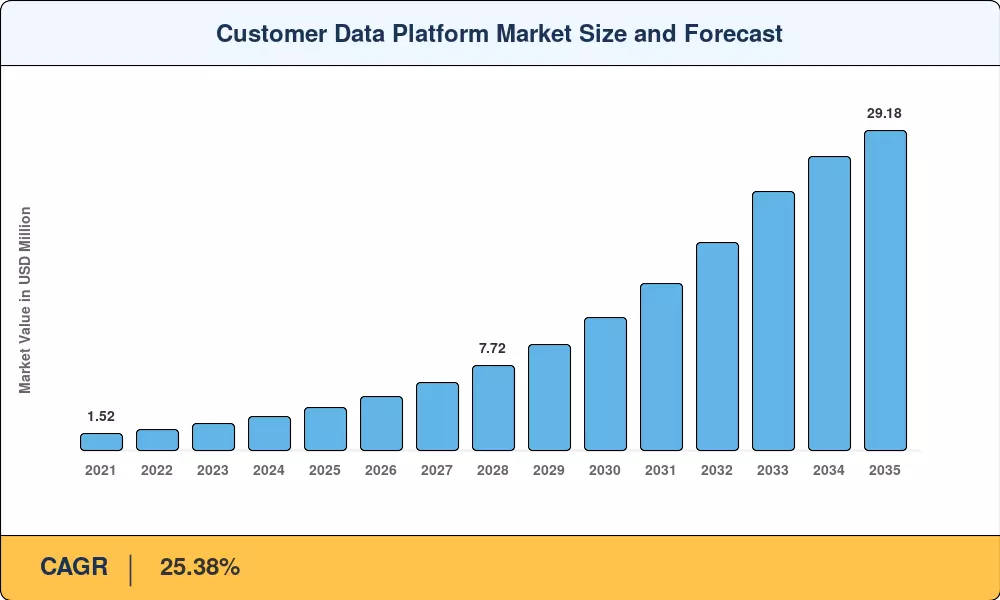

The customer data platform market reached an estimated USD 3.89 billion in 2025 and is projected to grow from USD 4.93 billion in 2026 to USD 29.18 billion by 2035, registering a CAGR of 25.38% during the forecast period. The phase-out of third-party cookies across major browsers and the enforcement of stricter data privacy mandates — including GDPR amendments in the EU and emerging US state-level privacy statutes — have pushed enterprises to invest aggressively in GDPR-compliant customer data management infrastructure that centralizes first-party data assets [2]. These twin pressures have turned what was once a martech luxury into a boardroom-level data infrastructure priority.

Legacy marketing clouds and siloed CRM systems are rapidly giving way to composable, warehouse-native architectures that support real-time customer data unification platforms. Enterprises allocated an estimated USD 12.6 billion globally to first-party data stack modernization projects in 2024, a figure expected to climb 18% annually through 2028 as AI-driven audience segmentation in CDP environments moves from pilot programs into production workloads [3]. Generative AI agents demanding sub-second profile access have further accelerated the shift toward event-driven, streaming-first data topologies.

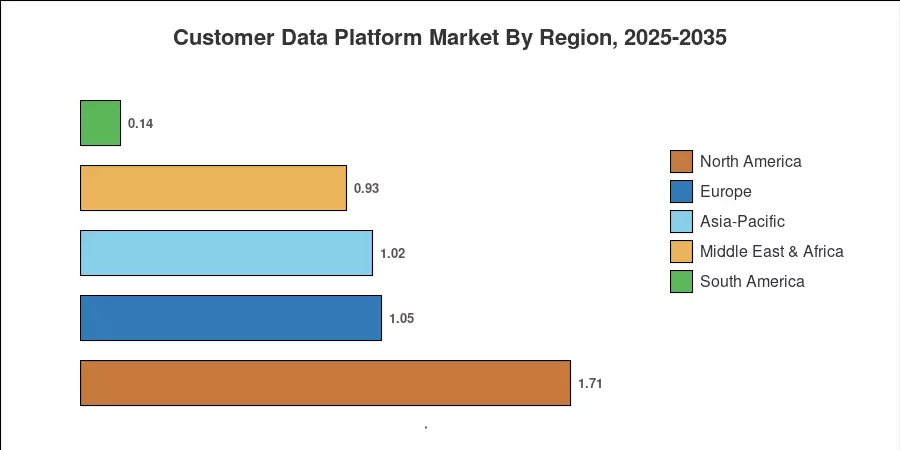

North America commands a leading position in the customer data platform market with approximately 44% of global revenue in 2025, propelled by early enterprise adoption and a mature SaaS ecosystem. Asia-Pacific is the fastest-growing region at a projected CAGR of 26.31%, fueled by rapid digital commerce expansion across India, Southeast Asia, and China. Europe holds the second-largest share at roughly 27%, where stringent GDPR enforcement continues to accelerate first-party data activation with CDP solutions across banking, retail, and telecom verticals. The decade ahead will reward vendors who embed privacy-by-design principles alongside composable integration layers.

Key Report Takeaways

• By Component

- Platforms accounted for approximately 74% of total customer data platform market revenue in 2025, reflecting enterprise preference for unified, out-of-the-box identity resolution and activation capabilities

- Services are forecast to expand at a CAGR of 25.72% through 2035, driven by rising demand for implementation consulting, data migration, and AI-driven audience segmentation in CDP deployments

• By Deployment Mode

- Cloud deployment represented roughly USD 4.19 billion in 2025, as organizations favor elastic scalability and warehouse-native architectures for real-time customer data unification platforms

- On-premise deployment retains traction among regulated industries requiring GDPR-compliant customer data management within sovereign data boundaries

• By End-User Industry

- Retail and e-commerce led the customer data platform market with an estimated 33% share in 2025, leveraging CDP for personalized omnichannel campaigns that unify in-store and digital touchpoints

- Healthcare is projected to post the fastest sectoral CAGR of 26.65% through 2035, driven by patient journey orchestration and first-party data activation with CDP in telehealth workflows

• By Region

- North America captured the largest regional share in 2025, underpinned by early-mover enterprise adoption and robust venture investment in CDP startups

- Asia-Pacific is expected to grow at a CAGR of 26.31%, as rapid digital transformation across India, China, and ASEAN economies accelerates demand

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue analysis of over 85 CDP vendors, validated against enterprise IT spending surveys and top-down macroeconomic modeling. Historical data (2021–2024) relies on audited vendor disclosures; forecast figures (2026–2035) apply a calibrated compound growth model anchored to the 2025 base year.