Customer Information System Market Summary

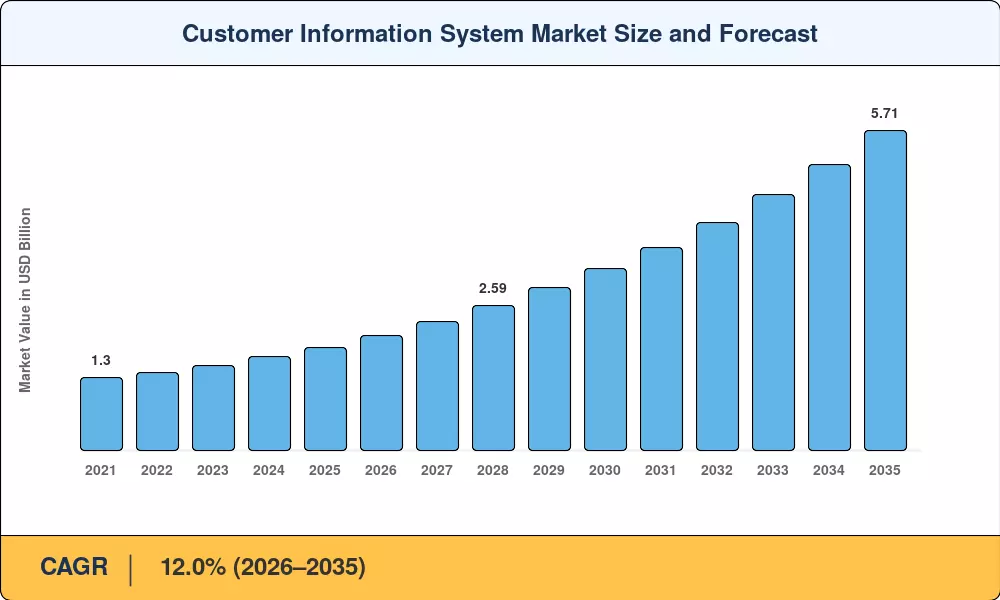

The customer information system market reached an estimated USD 1.84 billion in 2025 and is projected to grow from USD 2.06 billion in 2026 to USD 5.71 billion by 2035, registering a compound annual growth rate of 12.0% during the forecast period. Regulatory mandates on billing transparency — including FERC Order 2222 provisions and state-level consumer protection statutes — have compelled utilities and large enterprises to replace aging account management platforms with modern, API-driven architectures [1]. Capital expenditure commitments from the top 20 North American investor-owned utilities alone exceeded USD 4.8 billion for IT modernization programs between 2023 and 2025 [2].

The transformation reshaping the customer information system market centers on migrating from monolithic, on-premises billing engines — many of them 15 to 25 years old — toward cloud-native platforms that unify metering, billing, and real-time engagement layers. Southern California Gas Company's multi-year CIS replacement program, budgeted at over USD 300 million, illustrates the scale of these transitions [3]. Similar programs are underway at Enel, Tokyo Electric Power, and several UK water authorities, signaling that this is a global phenomenon rather than a North American outlier.

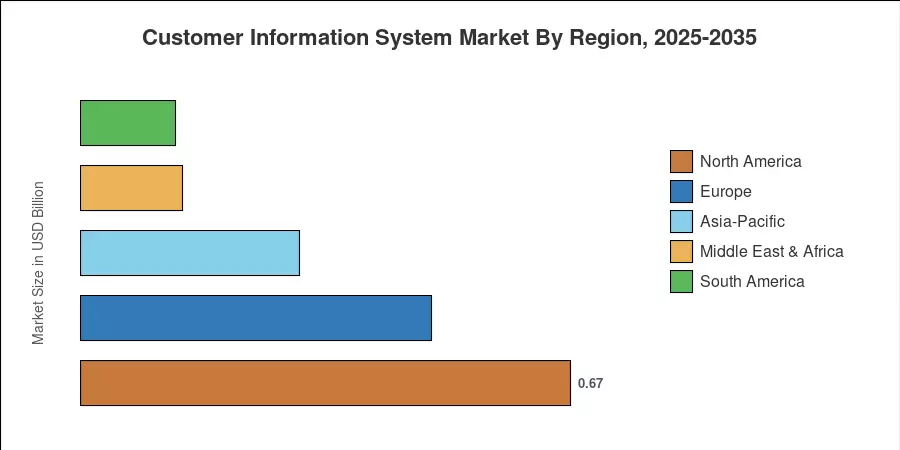

North America commands roughly 36.4% of the customer information system market, anchored by early smart-grid adoption and complex rate structures that demand sophisticated billing logic. Asia-Pacific is the fastest-growing region at a projected 16.4% CAGR, fueled by smart-city initiatives across India, China, and Southeast Asia. Europe holds the second-largest share at approximately 26.1%, driven by EU energy market deregulation timelines. The next decade will see competitive intensity sharpen as cloud vendors and legacy incumbents converge on the same digital-core value proposition.

Key Report Takeaways

• By Deployment

- On-premises installations accounted for 64.5% of customer information system market revenue in 2025, reflecting the entrenched nature of legacy billing infrastructure across regulated utilities.

- Cloud-based CIS deployments are forecast to expand at a 19.4% CAGR through 2035, outpacing the overall customer information system market growth rate by a significant margin.

• By Component

- The solutions segment held 74.6% revenue share of the customer information system market in 2025, encompassing billing engines, meter-data management modules, and customer self-service portals.

- Services — including implementation, migration consulting, and managed operations — are expected to register a 15.6% CAGR to 2035.

• By End-User

- Energy and utilities represented 47.8% of the customer information system market in 2025, making it the largest vertical by a wide margin.

- The retail CRM vertical is projected to post the fastest growth at a 17.2% CAGR, driven by omnichannel engagement demands.

• By Region

- North America led the customer information system market with a 36.4% share in 2025, supported by advanced metering infrastructure rollouts.

- Asia-Pacific is positioned as the fastest-growing region at 16.4% CAGR, underpinned by urbanization and national digitization agendas.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated research methodology combining primary interviews with CIS vendors and utility CIOs, bottom-up revenue modeling from disclosed contract values, and top-down validation against macroeconomic IT-spending benchmarks published by and.