Data Management Platform Market Summary

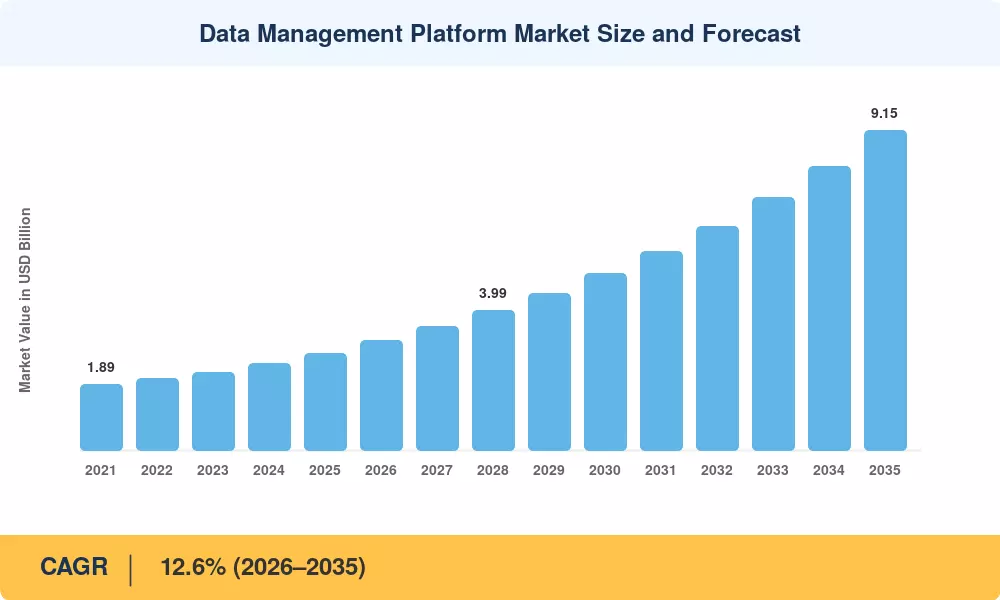

The Data Management Platform Market reached USD 2.76 billion in 2025 and is projected to grow from USD 3.14 billion in 2026 to USD 9.15 billion by 2035, registering a CAGR of 12.6% during the forecast period (2026–2035). Tightening data privacy legislation — including GDPR enforcement actions that exceeded EUR 2.1 billion in cumulative fines through 2024 and the phased deprecation of third-party cookies across major browsers — has pushed enterprises toward unified, consent-driven data architectures [1]. These regulatory catalysts, combined with retail media networks generating an estimated USD 45 billion in global ad spend by 2024, have turned the Data Management Platform Market into a critical infrastructure category for data-driven marketing and analytics [2].

Legacy tag-management and siloed analytics stacks are giving way to composable, API-first orchestration layers powered by embedded machine learning. Cloud-native platform spending across advertising technology alone surpassed USD 12 billion globally in 2024, reflecting the industry's decisive shift toward elastic, real-time decisioning environments [3]. Organizations now consolidate audience activation, identity resolution, and consent management within a single platform rather than stitching together point solutions.

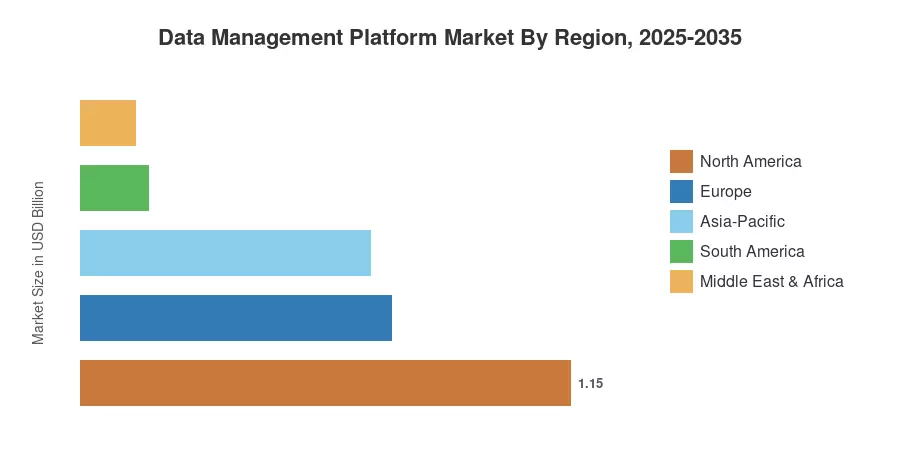

North America held 41.6% of the Data Management Platform Market in 2025, anchored by the United States' mature programmatic advertising ecosystem and stringent state-level privacy statutes. Asia-Pacific is the fastest-growing region at a 24.8% CAGR through 2035, driven by expanding digital advertising budgets across India, Southeast Asia, and China [4]. Europe accounted for the second-largest share at 26.3%, buoyed by GDPR-aligned platform investments. The Data Management Platform Market is set to benefit from 5G rollouts, edge computing adoption, and the growing monetization of consented first-party data assets through the balance of this decade.

Key Report Takeaways

• By Functionality

- First-party data modules captured 49.2% of the Data Management Platform Market revenue in 2025, reflecting enterprises' pivot to owned audience data amid cookie deprecation.

- Second-party data capabilities are expanding at a CAGR of 18.2% through 2035, powered by data clean rooms and secure collaboration partnerships.

• By Deployment

- Cloud-based delivery models held a 74.5% share of the Data Management Platform Market in 2025, driven by scalability requirements for real-time audience activation.

• By Enterprise Size

- SMEs posted the fastest growth at a 16.4% CAGR, as self-service platforms lowered adoption barriers.

• By Region

- North America generated USD 1.15 billion in 2025 Data Management Platform Market revenue, sustained by advanced programmatic ecosystems.

- Asia-Pacific is advancing at a 24.8% CAGR through 2035, the fastest among all regions.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining top-down industry sizing, bottom-up vendor revenue aggregation, and secondary validation through regulatory filings and advertising expenditure databases. Historical figures reflect verified platform subscription revenues, professional services, and managed data activation fees. Forecast estimates incorporate macroeconomic indicators, digital advertising spend trajectories, and privacy regulation adoption curves.