Dairy Ingredients Market Summary

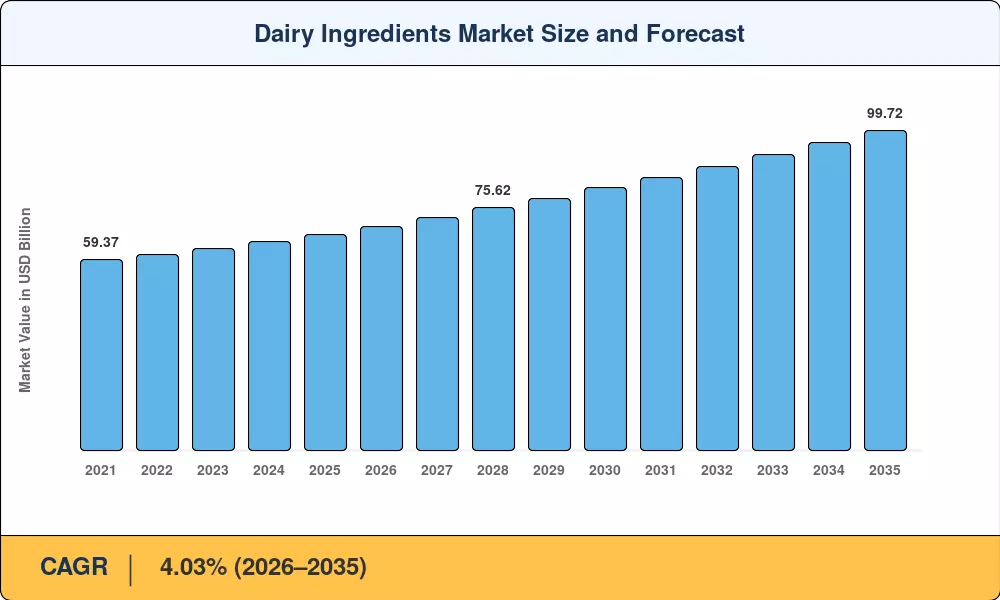

The Dairy Ingredients Market reached an estimated value of USD 67.26 Billion in 2025, with the sector projected to grow from USD 69.87 Billion in 2026 to USD 99.72 Billion by 2035, registering a CAGR of 4.03% across the forecast period. Rising global protein consumption, underpinned by public health campaigns promoting dairy-based nutrition and government food security stockpiling programs valued at over USD 14 Billion collectively, continues to anchor growth in the Dairy Ingredients Market. The World Bank's updated Food Security Action Plan and the EU's Farm to Fork Strategy have both reinforced procurement commitments for powdered and concentrated dairy ingredients, ensuring steady institutional demand through the decade [2].

Processing technology across the Dairy Ingredients Market is evolving rapidly. Conventional batch pasteurization and open-vat evaporation systems are giving way to continuous-flow membrane filtration, automated spray-drying towers, and precision fermentation platforms. Capital expenditure in next-generation dairy processing exceeded USD 5.8 Billion globally in 2024, according to industry estimates, with major cooperatives commissioning plants capable of producing specialty powders at 30% lower energy intensity [3]. These investments are compressing production costs while lifting output purity standards — a shift that favors large-scale, vertically integrated operators.

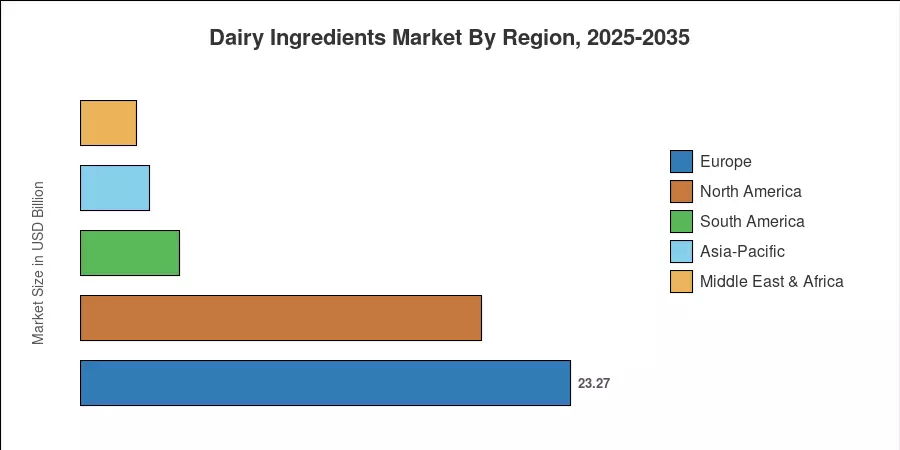

Europe commands the largest share of the Dairy Ingredients Market at approximately 34.6% of 2025 revenue, supported by stringent Codex Alimentarius compliance and an extensive cold-chain infrastructure across Western Europe. Asia-Pacific represents the fastest-growing region at a projected 4.88% CAGR, fueled by rising middle-class protein demand in India and China and favorable dairy development policies across ASEAN nations [4]. North America holds the second-largest position with roughly 28.3% share, driven by strong sports nutrition and infant formula manufacturing bases. As functional food innovation accelerates and emerging economies deepen dairy value chains, the Dairy Ingredients Market is poised for sustained expansion through 2035.

Key Report Takeaways

• By Product Type

- Milk Powders captured an estimated 63.8% of the Dairy Ingredients Market revenue in 2025, reflecting persistent demand from reconstituted beverage and bakery sectors.

- Whey Ingredients are projected to expand at a 4.35% CAGR through 2035, driven by sports nutrition and clinical nutrition applications.

• By Nature

- Conventional ingredients held approximately 83.5% of the Dairy Ingredients Market in 2025.

- Organic dairy ingredients are forecast to grow at a 5.30% CAGR over 2026–2035, reflecting premium consumer willingness-to-pay trends.

• By Application

- Food and Beverages represented roughly 47.7% of total demand within the Dairy Ingredients Market in 2025.

- Baby Food and Infant Formula applications are expected to register a 4.82% CAGR through 2035.

• By Region

- Europe retained approximately 34.6% of the Dairy Ingredients Market share in 2025.

- Asia-Pacific is forecast to grow at a 4.88% CAGR, the highest among all regions.

Market Size and Forecast (2021–2035)

The Dairy Ingredients Market sizing model integrates bottom-up revenue analysis from over 200 dairy processors globally, validated against top-down macroeconomic indicators including FAO milk production statistics, USDA trade data, and Eurostat dairy output figures [5]. Historical values reflect reported industry revenues; forecast values apply calibrated compound annual growth assumptions across product, nature, application, and geographic segments.

.webp?v=1783317664)