Dark Analytics Market Summary

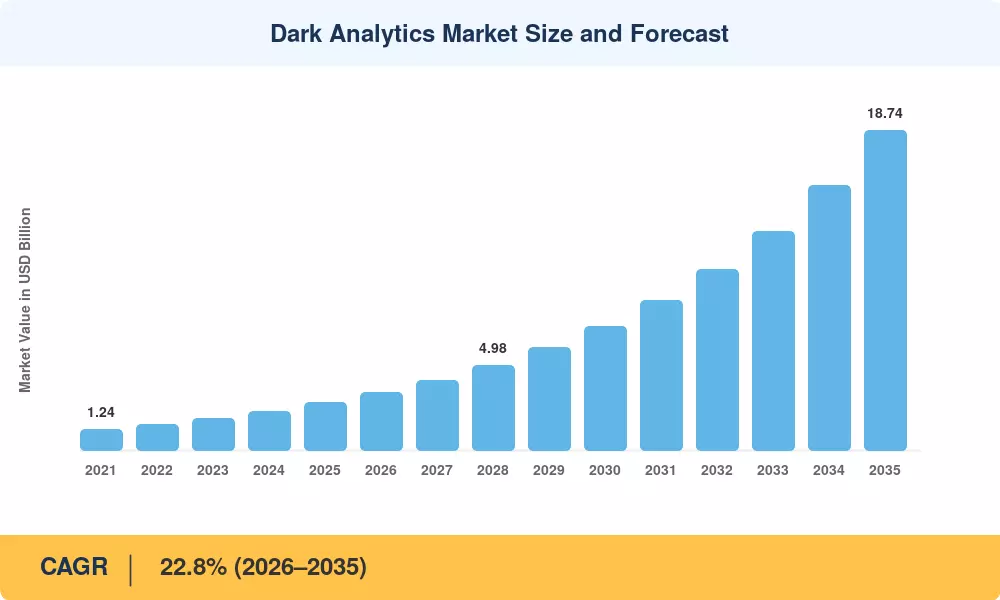

The Dark Analytics Market was valued at USD 2.82 billion in 2025 and is projected to reach USD 3.42 billion in 2026 before climbing to USD 18.74 billion by 2035, registering a CAGR of 22.8% during the forecast period (2026–2035). Enterprises are waking up to the reality that roughly 80% of their stored information sits untouched — log files, sensor feeds, legacy email archives, scanned documents — and regulatory frameworks such as the EU AI Act and the US Executive Order on AI (October 2023) are now compelling organizations to audit and govern these dormant assets [1][2]. That regulatory pressure, paired with corporate AI budgets that exceeded USD 154 billion globally in 2024, is channeling capital directly into dark data discovery and classification platforms.

A technology shift is replacing conventional ETL and warehouse pipelines with AI-native architectures. Large language models, vector databases, and retrieval-augmented generation (RAG) stacks can now ingest unstructured dark data processing solutions at scale, converting archived PDFs, call-center recordings, and IoT telemetry into queryable intelligence within hours rather than months. Cloud hyperscalers have slashed object-storage costs by more than 30% since 2022, lowering the economic barrier that historically discouraged enterprises from even retaining dark data, let alone analyzing it [5].

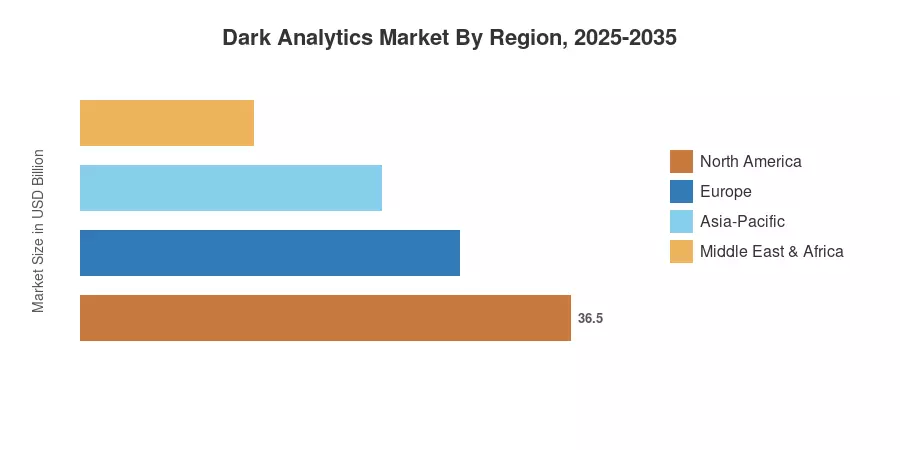

Early-mover financial institutions and federal data-governance laws have driven North America’s share of the Dark Analytics Market to roughly 39.2%. The Asia-Pacific is the fastest-growing market with a projected CAGR of 25.6%, driven by India’s Digital Personal Data Protection Act and the growth of smart city sensor networks in China. The second greatest proportion is Europe, with a little less than 26%, due to the regulatory measures of the GDPR, which are leading companies to list the hitherto unstructured processing of dark data across subsidiaries [6][7]. The next decade will reward vendors that combine hidden data mining, machine learning, privacy-preserving analytics, and real-time edge inference into a single commercial platform.

Key Report Takeaways

• By Analytics Type

- Predictive analytics captured a 45.1% share of the Dark Analytics Market in 2025, reflecting strong demand for forecasting models trained on previously unused enterprise datasets

- Prescriptive analytics is anticipated to register a 29.4% CAGR through 2035, as organizations move beyond prediction toward automated, AI-driven decision-making fueled by dark data discovery and classification

• By Deployment Model

- Cloud deployment retained a USD 2.00 billion revenue base in 2025, underscoring the dominance of scalable, multi-tenant platforms for AI extraction from unused enterprise data

- Edge and hybrid environments are projected to grow at a 27.2% CAGR to 2035, driven by latency-sensitive use cases in manufacturing and healthcare

• By End-User Vertical

- Financial services accounted for 29.3% of the Dark Analytics Market in 2025, led by anti-money-laundering and fraud-detection workloads running on hidden data mining with machine learning

- Healthcare is set to register the fastest vertical CAGR of 26.1% through 2035, as hospital systems unlock insights from archived enterprise data stored across legacy EHR platforms

• By Geography

- North America represented 39.2% of the Dark Analytics Market in 2025

- Asia-Pacific is poised to expand at a 25.6% CAGR through 2035, the fastest among all regions

Market sizing integrates bottom-up revenue analysis from vendor filings and top-down macroeconomic modeling calibrated against enterprise IT spending benchmarks published by Gartner, IDC, and national statistics bureaus. Historical figures (2021–2024) reflect audited revenues; 2025 is the base-year estimate; 2026–2035 values are forecast projections.

.webp?v=1782888023)