Data Integration Market Summary

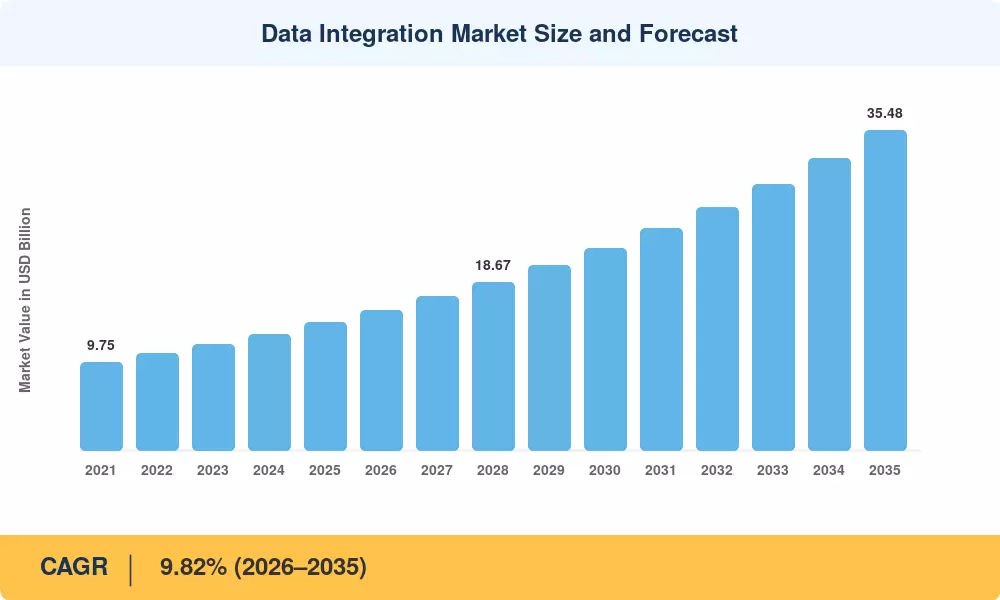

The data integration market reached an estimated USD 14.18 billion in 2025 and is projected to climb from USD 15.53 billion in 2026 to USD 35.48 billion by 2035, registering a CAGR of 9.82% across the forecast window. Two catalysts are accelerating spending: the European Union's Data Act, which mandates cross-platform data portability for enterprise cloud services by September 2025, and the cumulative USD 48 billion that Fortune 500 firms earmarked during 2023–2024 for AI-ready data infrastructure [1]. Together, these forces are converting data integration from a back-office utility into a board-level strategic priority.

Legacy batch-oriented ETL stacks—many dating to the early 2010s—are giving way to real-time data integration with Apache Kafka, stream-processing fabrics, and API-driven data integration for cloud apps. Enterprises now expect sub-second latency from operational data stores to analytics layers. Gartner estimates that by 2027, over 60 percent of new data-integration deployments will embed change data capture for real-time sync as a default capability, up from roughly 25 percent in 2023. This shift is pulling middleware vendors, hyperscalers, and niche pure-plays into intense competition for enterprise application integration middleware budgets.

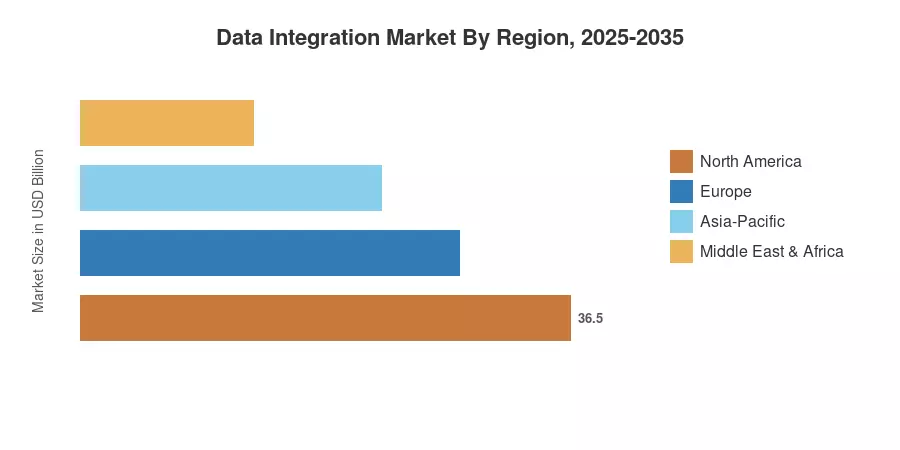

North America commands approximately 41% of global revenue, anchored by hyperscaler headquarters and a mature SaaS ecosystem. Asia-Pacific is the fastest-growing region at a projected CAGR near 19.1%, driven by India's Digital India programme and China's push toward sovereign data clouds. Europe holds the second-largest share at around 27%, propelled by GDPR-era data-governance mandates. As generative-AI workloads multiply, the data integration market is poised for sustained double-digit regional expansions well into the next decade

Key Report Takeaways

• By Component

- Cloud-based deployments captured roughly 62% of 2025 revenue, reflecting enterprise preference for elastic, API-driven data integration for cloud apps

- Tools—including ETL vs ELT for modern data pipelines platforms—accounted for an estimated USD 9.49 billion in 2025

- Services are forecast to expand at approximately 15.1% CAGR through 2035 as managed-integration demand rises

• By Deployment

- Cloud-based deployments captured roughly 62% of 2025 revenue, reflecting enterprise preference for elastic, API-driven data integration for cloud apps

• By Application

- Customer and sales analytics represented the leading application segment in the data integration market, holding about 31% of 2025 revenue

- The BFSI sector led end-user verticals with roughly 25.8% share in 2025

- Healthcare and life sciences is projected to grow at close to 20.3% CAGR, the fastest among verticals

• By End-User Vertical

- Customer and sales analytics represented the leading application segment in the data integration market, holding about 31% of 2025 revenue

• By Region

- North America generated approximately USD 5.81 billion in 2025, driven by enterprise application integration middleware upgrades across financial services

- Asia-Pacific's CAGR of ~19.1% makes it the primary growth frontier for the data integration market

Market Research Future (MRFR) 's sizing model triangulates vendor revenues, enterprise IT spending surveys, and bottom-up workload analysis across 32 countries. Historical figures (2021–2024) draw on audited filings and IDC spending trackers; forecast years apply a calibrated CAGR with annual modulation reflecting macroeconomic cycles and regulatory triggers.

.webp?v=1782888023)