Debt Collection Software Market Summary

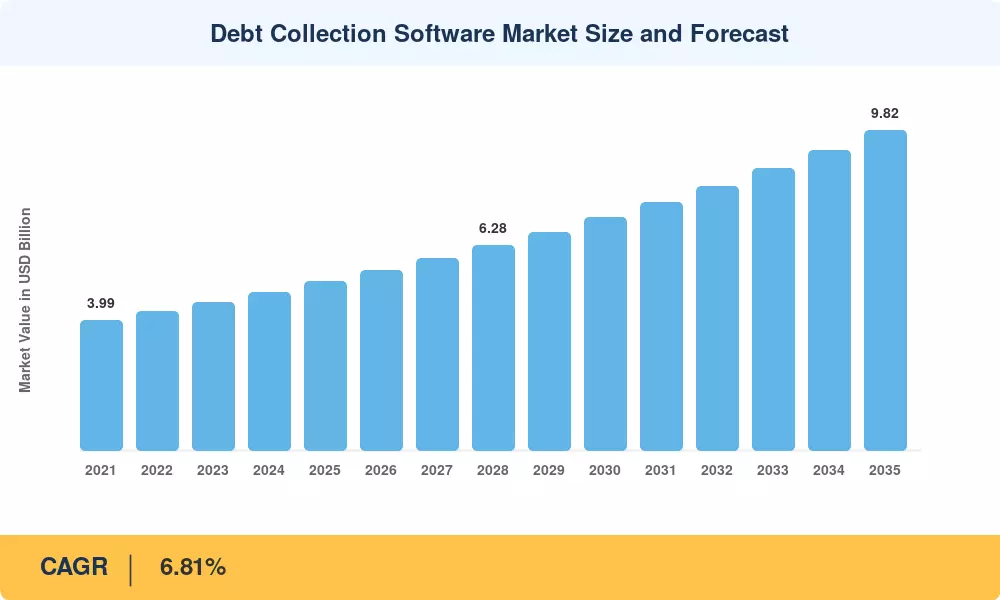

The debt collection software market reached an estimated USD 5.19 billion in 2025 and is projected to grow from USD 5.54 billion in 2026 to USD 9.82 billion by 2035, registering a CAGR of 6.81% during the forecast period. Two catalysts are accelerating this trajectory: the U.S. Consumer Financial Protection Bureau's updated Regulation F enforcement framework, which pushed agencies toward FDCPA-compliant debt management software, and record-high household debt service ratios across OECD economies that exceeded 14.2% in late 2024 [1]. With more than USD 1.1 trillion in receivables now routed through digital platforms annually, creditors face mounting pressure to modernize or lose ground.

Legacy on-premises collection suites — many built on decade-old telephony stacks — are giving way to cloud-native platforms integrating AI-powered debt recovery automation, real-time insolvency scoring, and omnichannel debt collection communication platforms. A 2024 McKinsey Digital survey estimated that top-quartile agencies deploying predictive dialer for debt collection calls alongside behavioral analytics recovered 18–22% more principal than peers still relying on manual workflows [2]. This technology shift is not incremental; it represents a structural re-platforming of how the industry engages debtors.

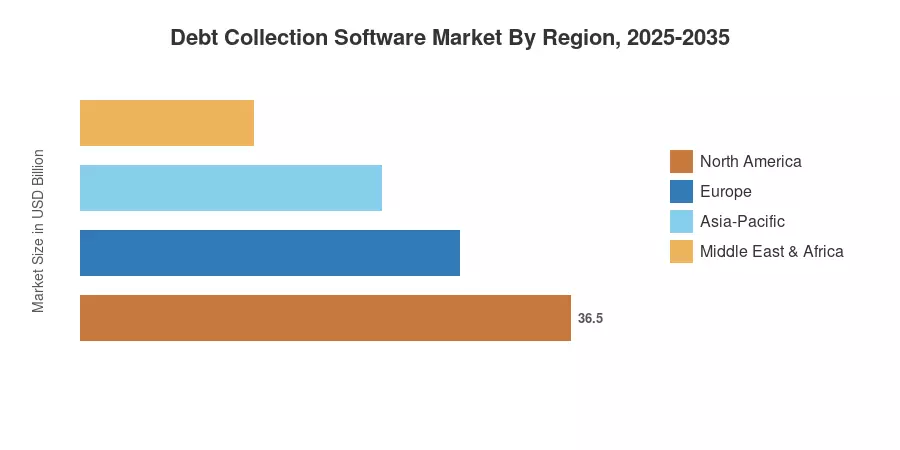

North America commands roughly 37% of the debt collection software market, anchored by the sheer scale of U.S. consumer credit and healthcare receivables. Africa ranks as the fastest-growing region at a projected CAGR exceeding 7.9%, driven by mobile-money proliferation and fintech-led microfinance expansion [3]. Europe holds the second-largest share near 26%, where the EU's AI Act transparency mandates for automated scoring are compelling vendors to invest in explainability layers. The decade ahead will reward platforms that blend compliance intelligence with debtor-centric self-service payment portals for debt resolution.

Key Report Takeaways

• By Component

- Software accounted for approximately 67% of the debt collection software market in 2025, reflecting entrenched demand for AI-powered debt recovery automation modules across enterprise portfolios

- Services are forecast to expand at around 8.9% CAGR through 2035 as agencies outsource implementation, training, and managed analytics

• By Deployment Mode

- Cloud-based platforms captured roughly 76% of the debt collection software market share in 2025, buoyed by lower upfront costs and elastic scalability

- On-premises solutions continue to serve regulated financial institutions requiring on-site data sovereignty

• By End-User Industry

- Financial institutions represented the largest vertical at approximately 41% share, deploying FDCPA-compliant debt management software across consumer lending and credit-card portfolios

- The retail and e-commerce segment is expected to post a CAGR of roughly 9.0% through 2035, propelled by surging buy-now-pay-later delinquencies

• By Region

- North America held about 37% of the debt collection software market in 2025

- Africa is projected to register the highest CAGR at approximately 7.9% during the forecast period

Market Research Future (MRFR)'s estimates blend bottom-up vendor revenue analysis with top-down macroeconomic modeling of consumer and commercial debt volumes across 42 countries. Historical data draws from audited annual reports, central bank credit statistics, and third-party IT spending trackers; forecast values apply Market Research Future (MRFR)'s calibrated CAGR to the 2025 base year.

.webp?v=1782888023)