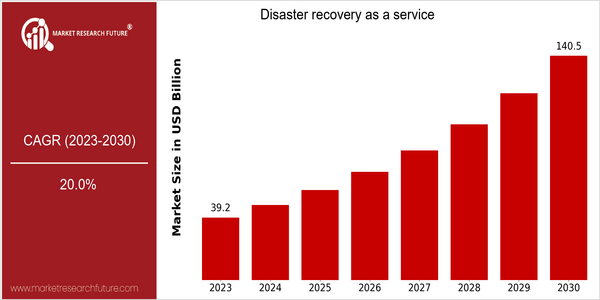

Disaster Recovery Service Size

Market Size Snapshot

| Year | Value |

|---|---|

| 2023 | USD 39.2 Billion |

| 2030 | USD 140.5 Billion |

| CAGR (2023-2030) | 20.0 % |

Note – Market size depicts the revenue generated over the financial year

Disaster Recovery as a Service (DRaaS) is a market that is expected to grow substantially in the near future, with a forecasted market size of $39 billion by 2023, which is expected to grow to $140 billion by 2030. This represents a high CAGR of 20.4 per cent during the forecast period. This growth is being driven by the increasing dependence on digital systems and the rising number of cyber-attacks and natural disasters. Also, the growing need for organizations to ensure business continuity and reduce downtime is driving the demand for DRaaS. Also, the rise in the use of cloud, automation and artificial intelligence is expected to play a key role in shaping the DRaaS market. These innovations help organizations to adopt cost-effective and efficient DR strategies, thereby enhancing their resilience to disruptions. DRaaS market leaders such as IBM, Microsoft and VMware are investing in product innovation and partnership strategies to strengthen their service offerings. For example, cloud service providers have been collaborating with cyber security companies to enhance the security and reliability of DRaaS solutions. These solutions will enable organizations to protect their critical data and applications in an increasingly volatile environment.

Regional Market Size

Regional Deep Dive

The market for DRaaS is growing at a fast rate in many regions, driven by the growing importance of security, compliance and the need for business continuity. Each region has its own characteristics, influenced by the economic situation, the technological environment and the cultural attitude towards risk management. DRaaS is a natural consequence of the growing reliance of organizations on cloud-based solutions. The need for a disaster recovery solution that can reduce the impact of a disaster on the business is expected to grow.

Europe

- The European General Data Protection Regulation has had a considerable influence on the DRaaS market. It requires companies to ensure that their data is protected and can be recovered. Consequently, companies like Acronis and Zerto are developing products that are specifically designed to meet these strict regulatory requirements.

- DRaaS in Europe is a major trend, and is gaining momentum as businesses seek to ensure the continuity of operations in a distributed environment. This will inevitably lead to closer collaboration between service providers and enterprises.

Asia Pacific

- The digital transformation in Asia-Pacific is in full swing. India and China, for example, are investing heavily in cloud computing. This has led to a booming DRaaS market in which local competitors such as NTT Communications and Alibaba Cloud have emerged as key players.

- Business is becoming more and more aware of the importance of disaster recovery planning. In particular, small and medium-sized enterprises (SMEs) are becoming aware of the need for disaster recovery as a service (DRaaS).

Latin America

- Latin America is undergoing a gradual shift to cloud computing, with a corresponding growth in DRaaS, as businesses seek to protect their data and ensure continuity of operations. Local companies like Totvs and UOL Diveo are leading the way in providing DRaaS.

- The economic situation is influenced by the instability of political conditions and the exchange rate. Disaster recovery has become a higher priority for companies that wish to protect their business against unforeseen disruptions.

North America

- North America has been seeing a significant increase in demand for DRaaS, particularly as a result of the increased frequency of natural disasters and cyberattacks. IT companies like IBM and Microsoft are now developing solutions that combine machine learning and artificial intelligence to make DRaaS even more effective.

- Regulations such as the Californian Personal Data and Information Protection Act (CCPA) are pushing organizations to adopt more comprehensive disaster recovery plans, which is in turn driving a greater use of DRaaS. The resulting cloud spending will be largely driven by this trend.

Middle East And Africa

- IT investment and a greater awareness of the threat of cyber attacks are the two main factors influencing the DRaaS market in the Middle East and Africa. Oracle and IBM are increasing their presence in the region and are offering a range of DRaaS services tailored to local needs.

- In the public and private sectors, the implementation of the UAE National Cyber Security Strategy has prompted a surge in the use of disaster recovery as a service. This increased focus on resilience is expected to drive market growth in the years to come.

Did You Know?

“Did you know that nearly 60% of small businesses that experience a data breach go out of business within six months? This statistic underscores the critical importance of disaster recovery planning and the growing demand for DRaaS solutions.” — National Cyber Security Alliance

Segmental Market Size

Disaster Recovery as a Service (DRaaS) is a critical part of the cloud computing market, which is experiencing rapid growth as a result of the increasing reliance on digital infrastructure. The threat of natural disasters and cyber-attacks is driving demand for DRaaS. Regulations such as the General Data Protection Regulation and the Health Insurance Portability and Accountability Act (HIPAA) require companies to have a robust disaster recovery plan in place, which is further driving DRaaS adoption. As the market moves towards full-scale deployment, the likes of IBM, Microsoft and VMware are delivering a wide range of DRaaS solutions to businesses across all industry verticals. Amongst the most active are healthcare and financial services, with a particular focus on the protection of critical patient data and financial transactions. Similarly, the COVID 19 pandemic has accelerated the trend towards remote working, further highlighting the importance of disaster recovery plans. Moreover, advances in cloud technology, such as serverless computing and the use of machine learning to automate recovery processes, are transforming the DRaaS market.

Future Outlook

The Disaster Recovery as a Service (DRaaS) market is expected to grow rapidly from 2023 to 2030, with an estimated market value of $39.2 billion and a CAGR of 20.0%. The main driving force for this growth is the increasing reliance on cloud-based solutions, as organizations seek to enhance their resilience to data loss and business interruptions. The report estimates that by 2030, over 60% of enterprises will have adopted DRaaS, up from about 30% in 2023. This demonstrates a significant shift towards a more pro-active approach to disaster recovery, in the face of the growing threat of cyber-attacks and natural disasters. During this time, a number of technological developments are expected to enhance the performance of DRaaS offerings. These developments include the integration of artificial intelligence and machine learning into DRaaS offerings. In addition, increasing regulatory pressures and the need for compliance with new standards are expected to spur demand for more comprehensive DRaaS offerings. Also, the increasing adoption of hybrid cloud and the growing importance of data sovereignty will shape the competitive landscape, encouraging a greater focus on innovation and differentiation. As business continuity continues to be a priority for organizations, the DRaaS market will continue to evolve as a key component of enterprise risk management strategies.

Leave a Comment