Disaster Recovery Service Market Summary

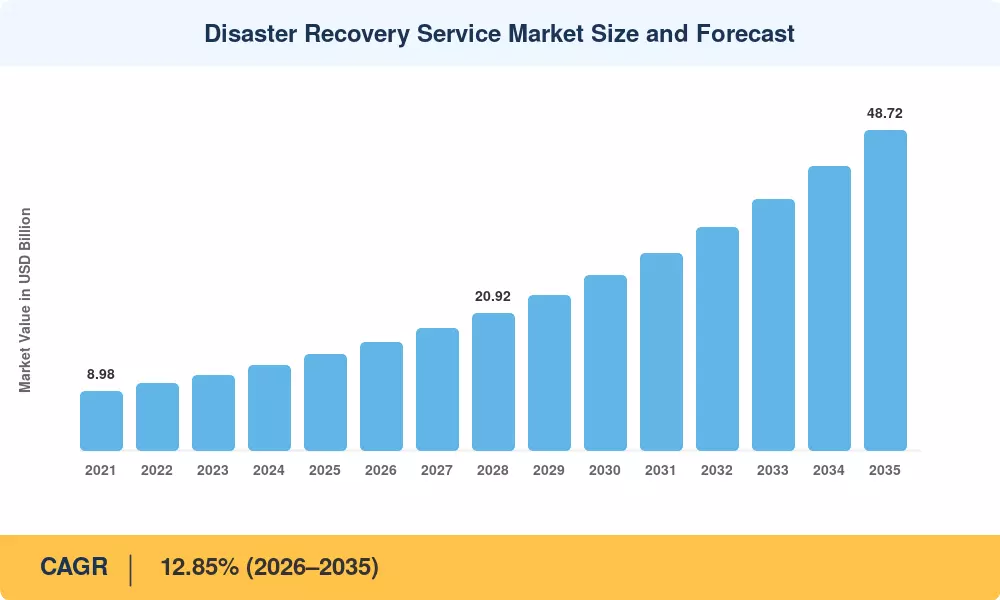

The Disaster Recovery as a Service Market reached a valuation of USD 14.56 billion in 2025 and is projected to grow from USD 16.43 billion in 2026 to USD 48.72 billion by 2035, registering a CAGR of 12.85% during the forecast period (2026–2035). A sharp escalation in ransomware incidents — global damages exceeded USD 30 billion in 2024 alone — has forced enterprises to rethink their business continuity planning strategies [2]. Regulatory bodies across North America and Europe now mandate tested recovery runbooks as a condition for cyber-insurance underwriting, directly linking premium costs to cloud backup solutions maturity [3].

Legacy tape-based and on-premises disk recovery architectures are giving way to cloud-native data recovery services that deliver automated failover in minutes rather than hours. The shift gained momentum after several high-profile supply-chain attacks in 2023–2024 demonstrated that traditional approaches could not meet sub-one-hour recovery time objectives demanded by boards and regulators [4]. Enterprise spending on DRaaS cloud platforms surpassed USD 9 billion globally in 2024, reflecting a 22% year-over-year increase as organizations prioritized resilience over capital expenditure.

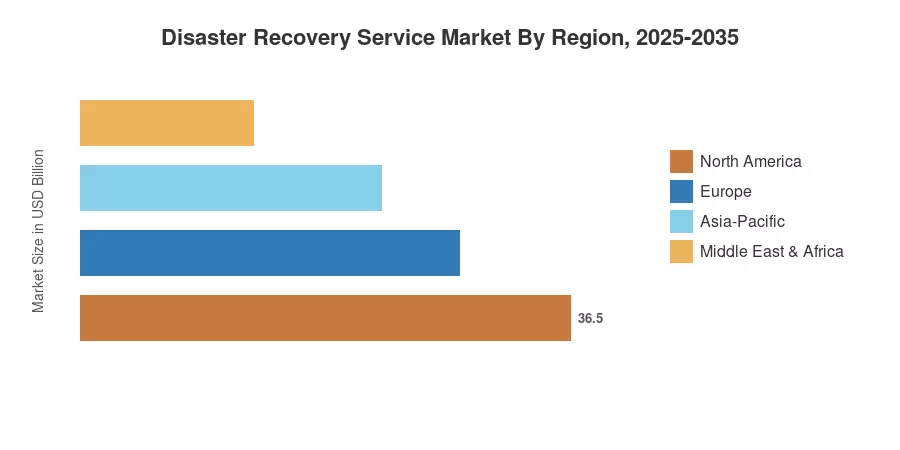

North America commands roughly 42% of the Disaster Recovery as a Service Market, anchored by stringent HIPAA, SOX, and FFIEC compliance mandates that require documented failover cloud infrastructure Asia-Pacific is the fastest-growing region at a 15.40% CAGR, fueled by digital-economy expansion across India, China, and ASEAN nations. Europe holds the second-largest share at approximately 27%, driven by GDPR and the EU's Digital Operational Resilience Act (DORA) [6]. The next decade will see orchestration intelligence and multi-cloud portability redefine how organizations buy and deploy recovery services.

Key Report Takeaways

• By Service Type & Component

- Fully Managed DRaaS solutions captured approximately 50% of the Disaster Recovery as a Service Market share in 2025, reflecting enterprise preference for turnkey business continuity planning offerings

- Orchestration and Automation is the fastest-growing service component, advancing at a 14.20% CAGR as organizations automate failover cloud infrastructure workflows

- Cloud backup solutions for real-time replication are projected to reach USD 7.8 billion by 2035, driven by zero-RPO mandates

• By Deployment & Organization Size

- Public Cloud deployments led the Disaster Recovery as a Service Market with 61% revenue share in 2025, though Hybrid/Multi-Cloud configurations are climbing fastest at 15.35% CAGR

- SMEs represent the fastest-expanding organization segment at a 15.95% CAGR, leveraging subscription-based data recovery services to access enterprise-grade resilience

• By Region

- North America generated USD 6.12 billion in 2025, with US federal agencies accelerating cloud-first mandates

- Asia-Pacific is projected to grow at 15.40% CAGR through 2035, outpacing all other regions as DRaaS cloud platforms scale across emerging digital economies

Market Size and Forecast (2021–2035)

MRFR's sizing methodology combines bottom-up revenue modeling from vendor disclosures, IT spending benchmarks from Gartner and IDC, and top-down validation against macroeconomic cloud-adoption indicators. Historical figures (2021–2024) reflect actual spend; forecast years (2026–2035) apply the calibrated 12.85% CAGR with adjustments for anticipated regulatory catalysts and technology adoption curves.

.webp?v=1786103502)