Distributed Energy Resource Management System Market Summary

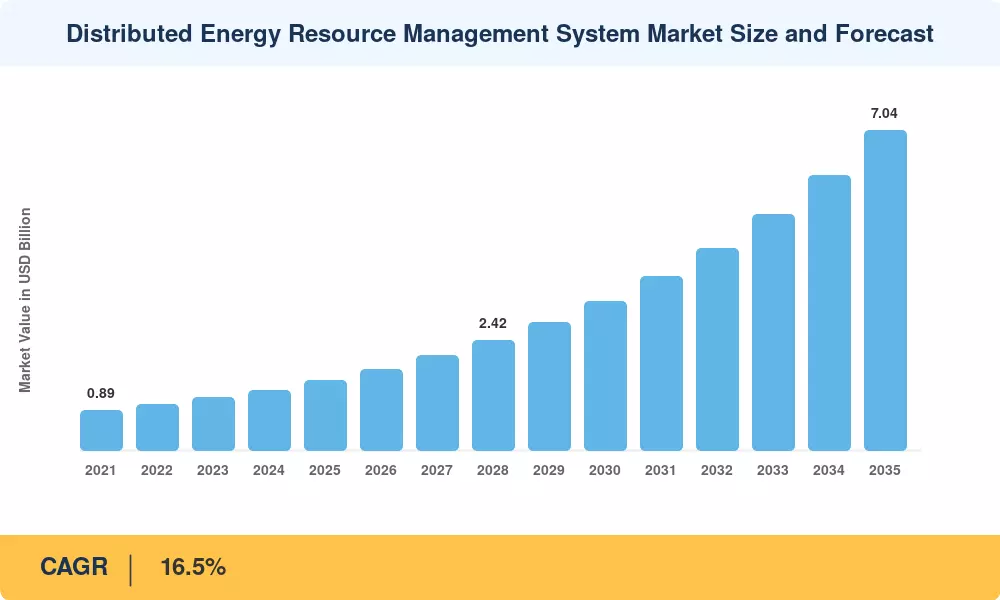

The Distributed Energy Resource Management System Market reached an estimated USD 1.53 billion in 2025 and is projected to climb from USD 1.78 billion in 2026 to USD 7.04 billion by 2035, registering a CAGR of 16.5% across the forecast window [1]. This trajectory reflects aggressive policy momentum — the U.S. Inflation Reduction Act alone has channeled over USD 370 billion toward clean energy and grid modernization programs, while the European Union's revised Renewable Energy Directive mandates 42.5% renewables in the energy mix by 2030 [2][3]. These twin forces are compelling utilities and independent power producers to adopt platforms that can orchestrate thousands of distributed assets in real time.

A fundamental technology shift is reshaping how grid operators manage energy flows. Legacy SCADA-based supervisory systems, designed for centralized generation, cannot handle the bidirectional complexity introduced by rooftop solar arrays, battery storage, and electric vehicle chargers feeding power back into the grid. AI-driven forecasting engines, edge computing nodes, and cloud-native orchestration platforms are replacing these rigid architectures, enabling sub-second dispatch decisions and predictive maintenance cycles [4]. The U.S. Department of Energy committed USD 3.5 billion through the Grid Resilience and Innovation Partnerships program in 2024, signaling that federal investment will continue to accelerate platform deployments [5].

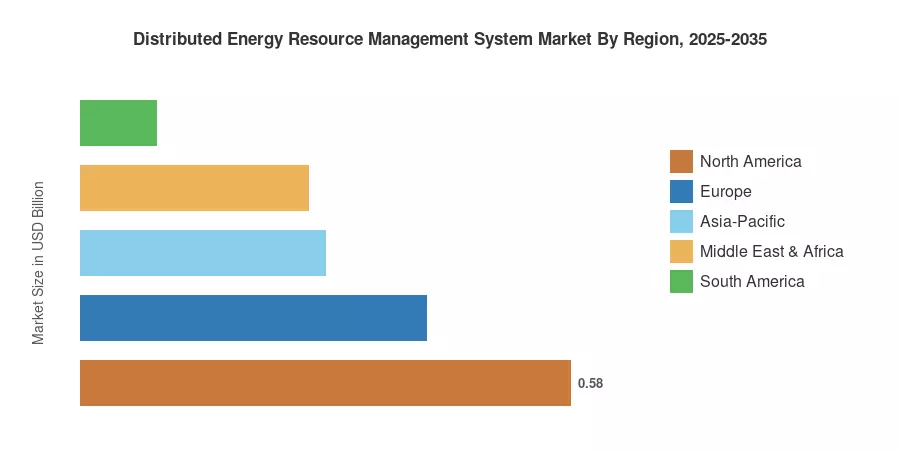

North America commands approximately 38% of the Distributed Energy Resource Management System Market, anchored by regulatory mandates in California, New York, and Texas. Asia-Pacific is the fastest-growing region at a projected CAGR of 19.2%, fueled by India's 500 GW non-fossil capacity target and China's aggressive smart grid rollout. Europe holds the second-largest share at roughly 27%, with Germany, the UK, and the Nordics leading adoption. As electrification accelerates across transportation, buildings, and industry, the Distributed Energy Resource Management System Market is set to become a foundational layer of the modern energy stack.

Key Report Takeaways

• By Technology

- Solar Photovoltaic (PV) represents the dominant technology segment, capturing approximately 42% of the Distributed Energy Resource Management System Market in 2025, driven by declining panel costs and net-metering mandates.

- The Electric Vehicles segment is forecast to grow at a CAGR of 20.1% through 2035 as vehicle-to-grid programs scale across major economies.

- Microgrids contributed an estimated USD 0.32 billion in 2025, supported by federal resilience investments and campus-scale deployments.

• By End User

- Industrial end users account for roughly 38% of total spending on the Distributed Energy Resource Management System Market, reflecting demand from energy-intensive manufacturing and mining operations.

- The Residential segment is expanding at a CAGR of 18.7%, as smart home ecosystems integrate with utility-facing orchestration platforms.

• By Region

- North America held the largest revenue share in 2025 at approximately 38%, supported by FERC Order 2222 and state-level distributed energy mandates.

- Asia-Pacific is projected to register the highest regional CAGR of 19.2% through 2035.

- Europe contributed an estimated USD 0.41 billion to the Distributed Energy Resource Management System Market in 2025.

Distributed Energy Resource Management System Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining top-down revenue analysis of leading platform vendors, bottom-up capacity aggregation across utility deployment data, and cross-referencing with regulatory filings from FERC, AEMO, and European energy regulators [1]. Historical figures reflect audited company disclosures and verified utility contracts; forecast projections apply a compound growth model calibrated against policy roadmaps, renewable capacity additions, and technology cost curves published by IEA and IRENA [7][8].