2026 Distribution Transformers Market Summary

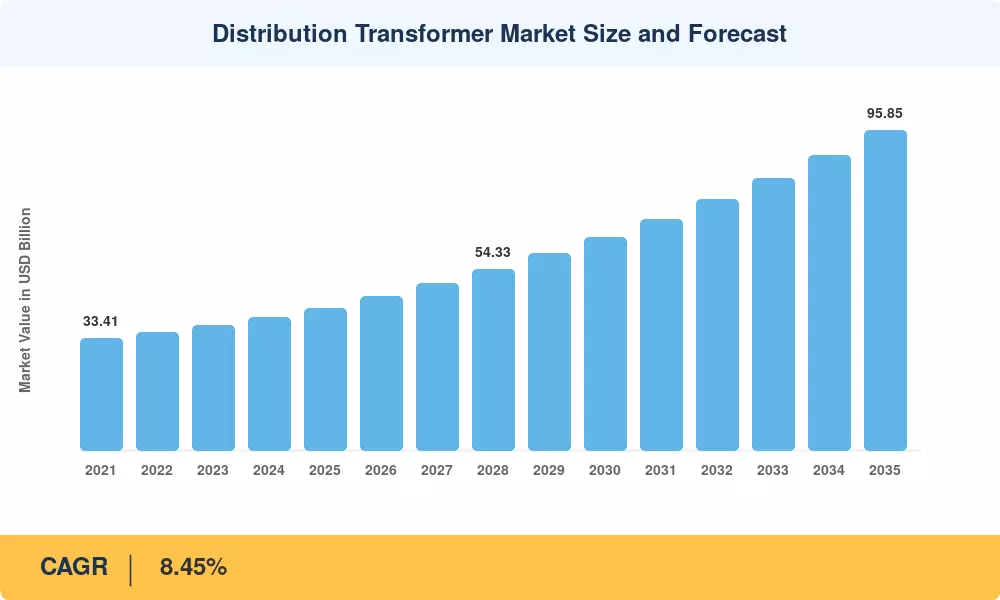

The Distribution Transformer Market reached an estimated USD 42.59 Billion in 2025 and is projected to grow from USD 46.19 Billion in 2026 to USD 95.85 billion by 2035, registering a CAGR of 8.45% during the forecast period. Accelerated grid modernization programs — driven by aging infrastructure installed between the 1970s and 1990s — alongside the rapid expansion of renewable energy interconnections, are creating sustained demand for new transformer capacity across both developed and emerging economies[2].

A generational technology shift is underway. Utilities and industrial operators are progressively retiring legacy mineral-oil units in favor of ester-fluid and dry-type platforms that meet tightening eco-design regulations in the EU and energy-efficiency mandates from the U.S. Department of Energy [3]. The IEA estimates that global electricity networks require over USD 600 billion in annual investment through 2030 to keep pace with electrification targets, and distribution-level equipment absorbs a meaningful share of that capital [4].

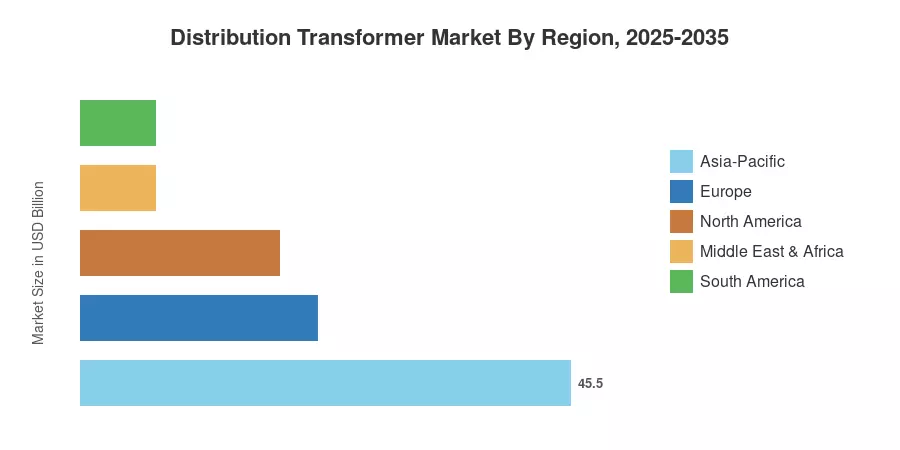

Asia-Pacific commands roughly 45.5% of the Distribution Transformer Market, anchored by large multiyear utility tenders in China and India. Europe holds the second-largest regional share at 22.0%, propelled by grid resilience mandates and offshore wind integration. North America, contributing 18.5%, is the region where data-center load growth and EV-charging corridor buildouts are reshaping neighborhood-level capacity planning most visibly. The Distribution Transformer Market outlook through 2035 remains structurally positive as electrification demand, decarbonization policy, and infrastructure renewal converge globally.

Key Report Takeaways

• By Power Rating

- Small units (≤ 10 MVA) held a 62.1% revenue share in the Distribution Transformer Market in 2025, reflecting widespread residential and commercial deployment.

- Medium units (10–100 MVA) are projected to advance at a 9.2% CAGR through 2035, driven by industrial and renewable-interconnection demand.

• By Cooling Type

- Oil-cooled designs captured 68.5% of 2025 revenue, supported by cost advantages in rural and industrial applications.

- Air-cooled configurations are forecast to grow at a 9.5% CAGR over 2026–2035 as fire-safety and indoor-installation requirements expand.

• By Phase

- Three-phase transformers accounted for 76.2% of unit volume in 2025.

- Single-phase units are expected to register a 9.4% CAGR through 2035, boosted by last-mile rural electrification programs.

• By End-User

- Power utilities represented 52.1% of Distribution Transformer Market demand in 2025.

- Residential applications are projected to advance at a 9.7% CAGR to 2035.

• By Region

- Asia-Pacific captured a 45.5% share of the Distribution Transformer Market in 2025.

- North America is projected to expand at a 7.9% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market sizing combines bottom-up demand analysis — aggregating utility procurement data, industrial capex disclosures, and regulatory filings — with top-down cross-validation against macroeconomic power-consumption growth models. Historical figures (2021–2024) reflect reported financials and trade data; the 2025 base year is estimated from preliminary shipment volumes; and the 2026–2035 forecast applies the calibrated CAGR alongside scenario-adjusted demand multipliers for EV charging, data centers, and renewable integration[5].