Power Transformers Market Summary

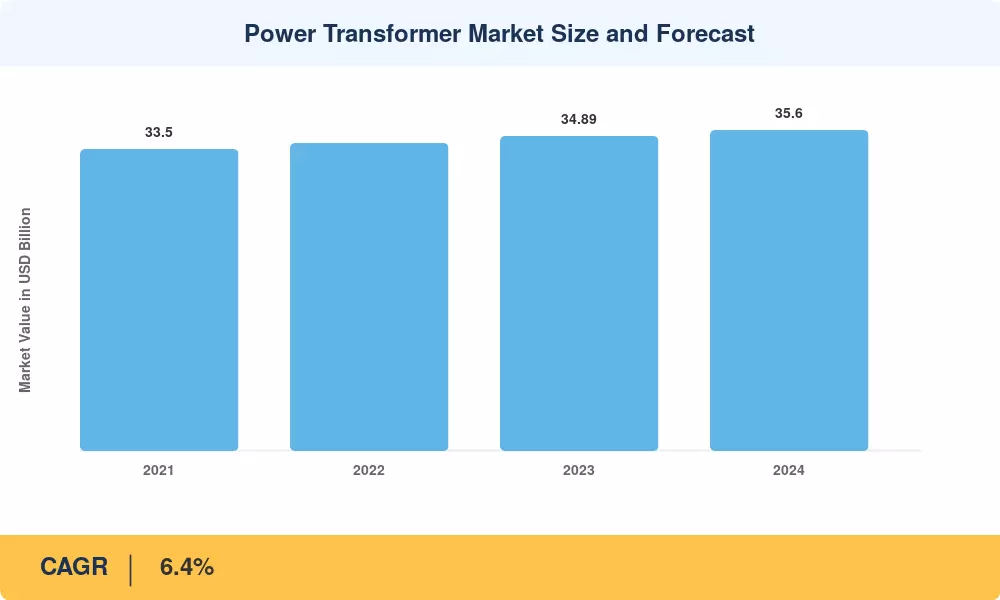

The global Power Transformer Market stood at an estimated USD 33.5 billion in 2025, reflecting a sector entering its most consequential investment cycle in decades. From a 2026 starting value of USD 35.6 billion, the Power Transformer Market is projected to reach USD 62.2 billion by 2035, expanding at a compound annual growth rate of 6.4% during the 2026–2035 forecast period. Two catalysts anchor this trajectory: the IEA's finding that global grids require USD 600 billion in annual investment through 2030 to meet net-zero targets [1], and the accelerating retirement of transformers installed during the 1960s–1980s capacity build-out across North America and Europe [3].

Technological advancements are altering priorities regarding procurement. Advanced insulation systems, sensor-embedded bushings, and digitally integrated monitoring platforms are being used to supplement traditional silicon-steel core transformers. The 2024 National Transmission Planning Study conducted by the U.S. Department of Energy identified a requirement for 47,000 GW-miles of additional high-voltage transmission capacity by 2035. This figure is directly proportional to the demand for large-scale power transformers [3]. Efficiency mandates are being tightened by utilities at the same time; the EU's Ecodesign Tier 2 requirements, which have been in effect since July 2021, have encouraged manufacturers to adopt lower-loss core designs [10].

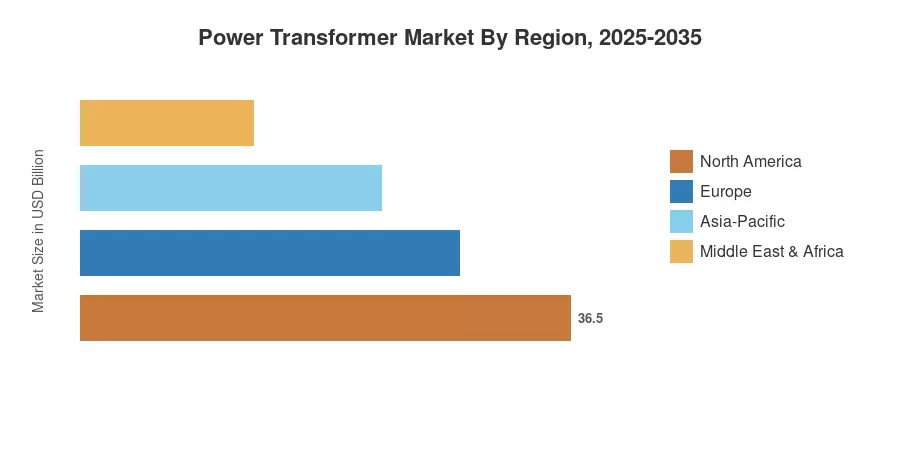

The Power Transformer Market is primarily dominated by the Asia-Pacific region, which accounts for approximately 42% of global revenue. This dominance is primarily due to the utility expansion programs in China and India [15]. The region also experiences the most rapid growth, with an estimated 7.8% compound annual growth rate (CAGR) through 2035. Under ENTSO-E's Ten-Year Network Development Plan [20], Europe maintains an approximate 24% market share through cross-border capacity auctions and offshore wind interconnection. North America, the third-largest region, is expanding at a rate of 5.8% per year as utilities compete to replace their antiquated fleet assets. Manufacturers who can provide reduced lead times, higher efficiency ratings, and integrated digital capabilities will be rewarded in the upcoming decade.

Key Report Takeaways

• By Rating (MVA)

- Small-rating transformers (up to 100 MVA) hold ~38% of the Power Transformer Market share, driven by distribution network densification in emerging economies.

- Medium-rating units (100–500 MVA) are expanding at a 7.1% CAGR, reflecting utility-scale solar and wind farm interconnection demand.

- Large-rating transformers (above 500 MVA) represent a high-value niche worth approximately USD 6.8 billion in 2025.

• By Cooling Type

- Oil-immersed transformers command ~78% market share, remaining the default for outdoor high-voltage installations.

- Dry-type units are the fastest-growing cooling category at an 8.2% CAGR, propelled by indoor data center and commercial building applications.

• By Region

- Asia-Pacific holds ~42% of the Power Transformer Market, anchored by State Grid Corporation of China's annual procurement exceeding USD 5 billion.

- North America is growing at a 5.8% CAGR as the U.S. Bipartisan Infrastructure Law allocates USD 65 billion to grid modernization.

- Europe contributes approximately USD 8.0 billion in annual revenue, shaped by offshore wind corridor build-outs.

Power Transformer Market Size and Forecast (2021–2035)

Market sizing integrates bottom-up transformer shipment volume analysis from 45+ OEMs, verified against top-down utility capital expenditure data sourced from IEA, EIA, World Bank, and national grid operator annual reports. Historical figures reflect actual procurement records; forecast values incorporate announced grid investment pipelines, renewable energy capacity targets, and fleet-age replacement schedules.