2026 Solid State Transformers Market Summary

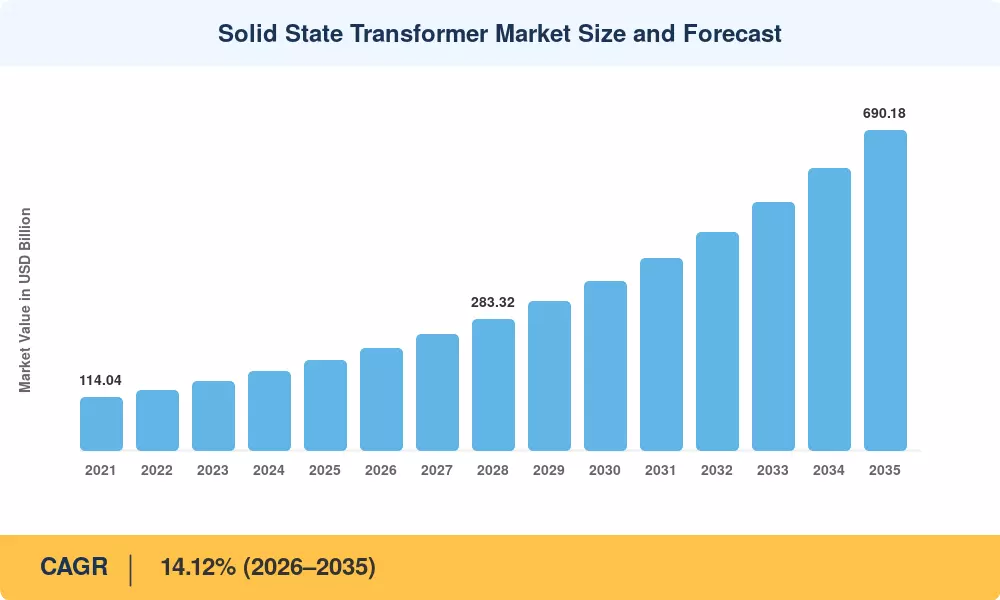

The Solid State Transformer Market was valued at USD 193.44 million in 2025 and is projected to grow from USD 218.85 million in 2026 to USD 690.18 million by 2035, registering a CAGR of 14.12% during the forecast period (2026–2035). Utilities across North America, Europe, and Asia-Pacific are accelerating grid modernization programs that prioritize compact, digitally controllable power conversion over conventional oil-filled transformers. The U.S. Department of Energy's Grid Resilience and Innovation Partnerships (GRIP) program alone has earmarked over USD 10.5 billion for next-generation distribution infrastructure, creating a robust policy tailwind for SiC power electronics adoption [2].

Legacy copper-and-iron transformers — many installed 40+ years ago — lack bidirectional power flow capability and real-time voltage regulation, two features essential for integrating rooftop solar, battery storage, and DC microgrids. SiC and GaN wide-bandgap semiconductors now switch at medium frequency with dramatically lower losses, enabling medium frequency solid state transformer designs that cut magnetic core weight by 50–70% and fit inside space-constrained urban substations [3]. A recent report estimates that replacing just 5% of aging U.S. distribution transformers with smart SST bidirectional power flow units could defer USD 3.8 billion in grid upgrade costs through 2032 [4].

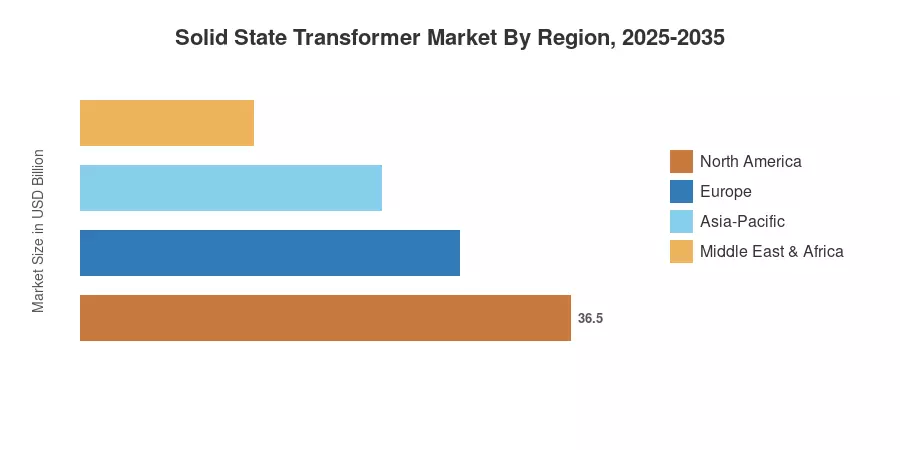

Asia-Pacific commands roughly 43.30% of global revenue, driven by China's State Grid spending on SST grid edge distribution pilots and India's Revamped Distribution Sector Scheme. Europe holds the second-largest share at approximately 26.50%, buoyed by EU directives phasing out SF₆ switchgear. North America is the third-largest region, propelled by defense microgrid mandates and solid-state transformer EV charging deployments along interstate corridors. As semiconductor costs continue their downward trajectory, the Solid State Transformer Market is positioned for sustained double-digit expansion well into the next decade [5].

Key Report Takeaways

• By Product Type

- Distribution SSTs captured 43.70% of the Solid State Transformer Market share in 2025, reflecting heavy utility investment in grid edge distribution upgrades

- Traction SST units for rail and on-board applications are forecast to expand at a 16.10% CAGR through 2035, the fastest among product segments

- Power SSTs contributed USD 48.36 million in 2025 revenue, anchored by industrial DC microgrid deployments

• By Voltage Level

- Medium-voltage equipment (2–36 kV) accounted for 59.55% of the Solid State Transformer Market in 2025

- High-voltage systems above 36 kV are expected to grow at a 15.85% CAGR, driven by offshore wind interconnection and HVDC tapping applications

• By Application

- Smart-grid and utility distribution applications led with USD 72.18 million in 2025 revenue

- Solid state transformer EV charging infrastructure is projected to post the quickest application-level CAGR of 17.25% through 2035

• By Region

- Asia-Pacific commanded 43.30% of 2025 revenue in the Solid State Transformer Market and is set to progress at a 15.05% CAGR

- North America contributed USD 42.17 million in 2025, supported by DOE GRIP grants and defense standards

Market Size and Forecast (2021–2035)

MRFR’s estimating framework triangulates bottom-up manufacturer revenue data, patent filing velocity, and top-down TAM modeling against utility expenditure budgets stated in regulatory filings. Historical numbers (2021-2024) are verified by FERC Form 1 filings, Eurostat energy accounts, and yearly reports of highlighted enterprises. The forecast predictions (2026-2035) use a calibrated CAGR of 14.12%, stress tested against three macro scenarios (base, accelerated policy, delayed adoption).

.