Drainage System Market Summary

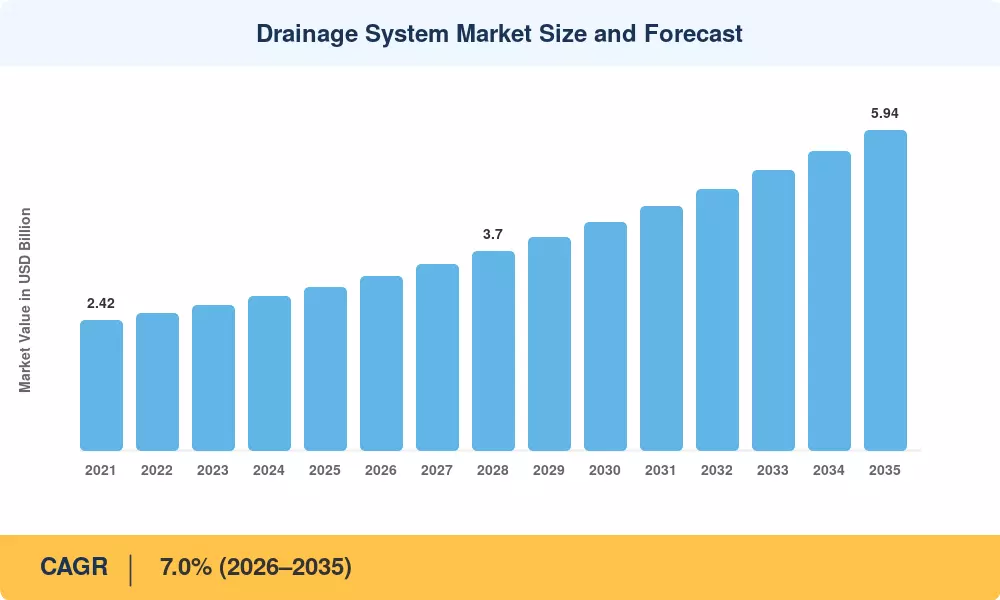

The drainage system market reached an estimated USD 3.02 Billion in 2025, positioning it for a forecast trajectory that begins at USD 3.23 Billion in 2026 and climbs to USD 5.94 Billion by 2035 at a compound annual growth rate of 7.0%. Two catalysts underpin this expansion: first, rising global surgical volumes—driven by aging populations and the growing burden of chronic cardiovascular and orthopedic conditions—are multiplying the procedural occasions that require effective fluid management. Second, infection-prevention mandates from agencies such as the U.S. Centers for Disease Control and Prevention (CDC) and the European Centre for Disease Prevention and Control (ECDC) are compelling hospitals to upgrade legacy open drainage configurations to closed, antimicrobial-coated alternatives [1][2].

The technology shift reshaping the drainage system market centers on the replacement of gravity-dependent passive collection with electronically regulated active suction platforms. Hospitals across North America and Western Europe are now integrating drainage units that feed real-time output data directly into electronic health records, a capability that legacy jar-and-tube setups cannot provide. The U.S. Department of Health and Human Services allocated over USD 1.6 Billion toward hospital infrastructure modernization grants between 2023 and 2025, a portion of which has flowed into surgical consumable upgrades including drainage equipment [3].

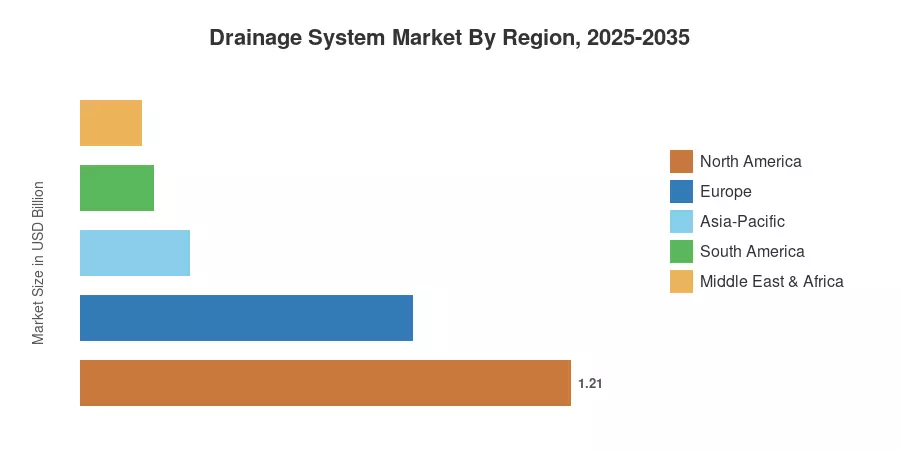

North America commands roughly 40% of global revenue in the drainage system market, anchored by high procedural reimbursement rates and a dense ambulatory surgery center network. Asia-Pacific is the fastest-growing region with a projected CAGR of 8.9% through 2035, fueled by government-backed hospital construction in India and China. Europe holds the second-largest share at approximately 27%, supported by stringent EU MDR compliance standards that favor premium device adoption. As surgical care decentralizes into outpatient settings worldwide, the drainage system market is expected to sustain above-average medtech growth through the forecast decade.

Key Report Takeaways

• By Product

- Drainage systems accounted for 63% of revenue in 2024, reflecting entrenched hospital purchasing patterns for integrated suction-and-collection units.

- Accessories—tubing kits, connectors, and replacement canisters—are forecast to register a 10.1% CAGR through 2035, driven by recurring procurement cycles.

• By Type

- Active drains held a 64% share of the drainage system market in 2024, underscoring clinician preference for controlled negative-pressure evacuation.

- Passive drains remain the cost-efficient option in resource-limited settings, sustaining steady single-digit growth.

• By Application

- Thoracic and cardiovascular procedures captured 32% of application-level revenue in 2024 within the drainage system market.

- Orthopedic applications are projected to grow at an 8.2% CAGR through 2035 as joint-replacement volumes rise globally.

• By End User

- Hospitals represented 77% of end-user spending in the drainage system market during 2024.

- Ambulatory surgical centers and clinics are forecast to register a 7.5% CAGR, the highest among end-user categories.

• By Geography

- North America generated approximately 40% of global drainage system market revenue in 2024.

- Asia-Pacific is projected to expand at an 8.9% CAGR, the fastest of any region, through 2035.

Drainage System Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from triangulated hospital procurement databases, customs trade records, and manufacturer disclosure filings. Forecast projections apply a bottom-up model calibrated against surgical procedure volume growth, reimbursement trends, and capital-equipment replacement cycles across 32 countries.